Policy Matters: Navigating the New Normal – A Regulator’s Outlook on Federal Momentum

Join us for the October edition of our new illuminating “Policy Matters” webinar series! In this dynamic session, we’ll dive into the intricacies of cannabis policy from two critical angles. For this month’s episode, we’re shifting the spotlight to the thriving adult-use cannabis marketplace in Maine, featuring our special guest, John Hudak, the Director of the Office of Cannabis Policy at the Maine Department of Administrative and Financial Services.

Discover the unique dynamics of Maine’s cannabis industry, from its regulatory framework to market trends and the challenges faced by industry stakeholders. Gain valuable insights into managing a successful adult-use market while adhering to rigorous regulatory standards. Then, we’ll explore the policy implications of descheduling or rescheduling cannabis, a topic that gained momentum following President Biden’s directive to review its federal classification.

Join our hosts, NCIA Policy Co-Chairs Khurshid Khoja and Michael Cooper and guest speakers, NCIA’s Director of Government Relations Michelle Rutter Friberg and John Hudak, Ph.D, the Director of the Maine Office of Cannabis Policy, as they discuss the potential shifts in cannabis policy, what the process may look like, and what to expect in the coming months.

Needless to say, with multiple federal agencies involved, an election year nearing, and Congress in disarray, this is a complex topic – but policy matters. Stay informed, stay ahead, and be part of the conversation that’s shaping the future of cannabis policy.

Tune in and empower yourself with the knowledge to thrive in this dynamic industry! Reserve your spot today and join us as we continue to unravel the complexities of cannabis policy and regulation.

Panelists:

John Hudak

Director | Maine Office of Cannabis Policy

HHS Recommends Rescheduling: Now What? | 9.14.23 | Fireside Chats with NCIA’s Government Relations Team

NCIA’s #IndustryEssentials webinar series is our premier digital educational platform featuring a variety of interactive programs allowing us to provide you timely, engaging and essential education when you need it most. The Fireside Chat series of NCIA’s #IndustryEssentials webinars are an opportunity for industry professionals to hear from our government relations team and guests about the latest developments in federal policy LIVE.

For more than fifty years, the federal government has maintained that cannabis is a Schedule I drug, meaning that it has a high potential for abuse and no accepted medical value.

That recently changed when the Department of Health and Human Services (HHS) recommended to the Drug Enforcement Administration (DEA) that cannabis be placed in Schedule III, meaning that it has moderate to low abuse potential, a currently accepted medical use, and a low potential for psychological dependence.

There’s no doubt this move was an historic one– but what does it mean? What’s next? How will it impact your business? Join NCIA’s Aaron Smith and Michelle Rutter Friberg as they unpack all these questions surrounding cannabis rescheduling impact and more!

Fireside Chats with NCIA’s Government Relations Team: HHS Recommends Rescheduling; Now What?

NCIA’s #IndustryEssentials webinar series is our premier digital educational platform featuring a variety of interactive programs allowing us to provide you timely, engaging and essential education when you need it most. The Fireside Chat series of NCIA’s #IndustryEssentials webinars are an opportunity for industry professionals to hear from our government relations team and guests about the latest developments in federal policy LIVE.

For more than fifty years, the federal government has maintained that cannabis is a Schedule I drug, meaning that it has a high potential for abuse and no accepted medical value.

That recently changed when the Department of Health and Human Services (HHS) recommended to the Drug Enforcement Administration (DEA) that cannabis be placed in Schedule III, meaning that it has moderate to low abuse potential, a currently accepted medical use, and a low potential for psychological dependence.

There’s no doubt this move was an historic one– but what does it mean? What’s next? How will it impact your business?

Join NCIA’s Aaron Smith and Michelle Rutter Friberg as they unpack all these questions and more! Register today and don’t miss your chance to hear from two of the foremost government relations experts in the cannabis industry.

Panelists:

Aaron Smith

Chief Executive Officer

National Cannabis Industry Association

Michelle Rutter Friberg

Director of Government Relations

National Cannabis Industry Association

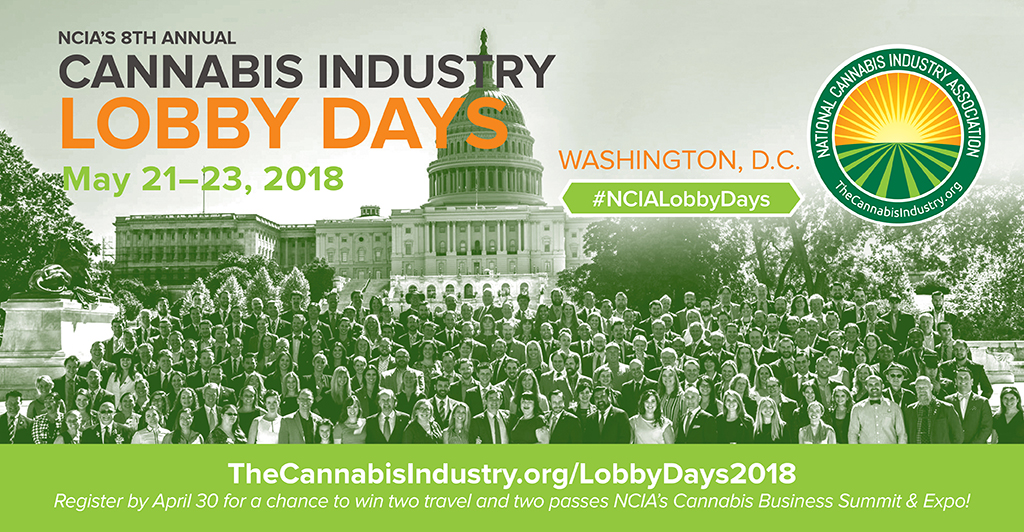

NCIA Members United in D.C. at Lobby Days! Join Us Next Year!

Photo By CannabisCamera.com

by Michelle Rutter Friberg, NCIA’s Deputy Director of Government Relations

Essentially every industry and association with a presence in Washington, D.C. hosts their own lobby days, advocacy days, or fly-ins – whatever you want to call them – where their members come to the Capitol to lobby Congress on their respective industry and legislative issues.

Thanks to NCIA, the cannabis industry is no different. In fact, just a few weeks ago, more than 100 members of the National Cannabis Industry Association (NCIA) descended upon Capitol Hill for NCIA’s 11th Annual Cannabis Industry Association Lobby Days. Lobby Days are an opportunity to advocate for our industry and tell Capitol Hill staff about the real, lived, on-the-ground experiences that cannabis professionals experience daily.

Planning 150+ meetings over the course of two days with 100+ attendees and 21 teams is about as easy as it sounds. That’s not to mention the multiple events, a congressional briefing, and training sessions! But that’s exactly what the NCIA team does for our members every spring. At lobby days, NCIA members gather to amplify our message and make their voices heard in the halls of Congress, while simultaneously forging strong relationships with the most influential leaders in the cannabis industry.

With more than 80 freshman members in Congress this session and multiple bills that have yet to be reintroduced, we wanted to focus our efforts on educating new members about the issues the cannabis industry – and the people that comprise it – face regularly. Many of these members and their staff have never heard of 280E, haven’t had to vote on SAFE Banking (yet!), and are on the fence about legalization, while others have never even talked with a cannabis professional. As a result, it was incredibly important to us that we reach out to those offices and provide them with the resources they need to best inform their position on the various policy areas that cannabis touches.

After arriving in D.C., attendees were greeted with a tropical vibe at our welcome reception at Tiki TnT & Potomac Distilling Company. This gave teams an opportunity to meet up ahead of meetings and mingle with other professionals who made the trip. The next day, we all gathered bright and (very) early for our mandatory breakfast training ahead of shuttling to the Capitol grounds for our group photo. At the training, attendees were able to grab a quick bite to eat, drink some coffee, get together with their teams, and get the final “do’s and don’ts” for their meetings. After our training and group photo, our teams split off for their meetings and reconvened at the end of the day for our stunning closing reception. There, attendees debriefed after an incredibly productive day and unwound with beautiful views, some drinks, and a dreamy jazz band. On the final day, attendees began their morning with a Senate briefing focused on SAFE Banking, where they rubbed elbows with congressional staff. Post-briefing, teams broke off for their final meetings, and just like that, lobby days 2023 was a wrap!

It’s no secret that the cannabis industry is undergoing significant struggles and we’re feeling that squeeze in Washington, D.C. Many companies have downsized and laid off government relations professionals, while others continue to just hope that Congress will pass reform magically. The truth is that lobbying, advocating, and being active in the legislative process are critical to moving our industry forward. Stay tuned for other citizen lobbying opportunities, and take it to the next level by sponsoring NCIA’s 12th Annual Cannabis Industry Lobby Days in 2024!

The legal cannabis industry is growing at an unprecedented rate, with more and more states legalizing its use for medical and recreational purposes. However, despite this progress, cannabis businesses face a major obstacle: Section 280E of the Internal Revenue Code. This provision is a significant burden on cannabis businesses, limiting their ability to take deductions for basic expenses like rent, utilities, and employee salaries. The result is a higher tax burden and reduced profitability, putting cannabis businesses at a disadvantage compared to other industries.

Section 280E was introduced in the 1980s as a way to prevent drug dealers from taking business deductions on their tax returns. At the time, the provision was aimed primarily at illegal drug dealers. However, when it comes to cannabis businesses, Section 280E has become a significant hurdle. The problem is that while cannabis is legal for medical or recreational use in many states, it remains a Schedule I drug at the federal level. This means that cannabis businesses are still subject to the same limitations as illegal drug dealers when it comes to tax deductions.

The impact of Section 280E on cannabis businesses is significant. Without the ability to deduct basic expenses, cannabis businesses face higher tax burdens and reduced profitability. This makes it difficult for them to reinvest in their operations and grow their businesses. In addition, the provision makes it challenging for cannabis businesses to obtain financing, as many traditional lenders are hesitant to work with them due to the regulatory environment and the industry’s status as a Schedule I drug.

The insurance industry plays a vital role in supporting the cannabis industry. With the help of insurance professionals, cannabis businesses can protect their assets, mitigate risks, and navigate the complex regulatory environment. However, insurance providers also face challenges in the cannabis industry due to the regulatory environment and the industry’s status as a Schedule I drug. For example, some insurance companies are hesitant to provide coverage to cannabis businesses due to concerns about federal prosecution.

Despite these challenges, there are insurance providers that specialize in the cannabis industry and offer tailored solutions to cannabis businesses. By working with these providers, cannabis businesses can protect their assets and minimize risks, while also demonstrating to potential investors and lenders that they are taking the necessary steps to manage their risks.

In addition to the insurance industry, there are other steps that policymakers can take to support the cannabis industry. Revising Section 280E is one of the most critical steps that can be taken. By allowing cannabis businesses to take more deductions on their tax returns, policymakers can help level the playing field and create a more equitable regulatory environment for the industry. This would enable cannabis businesses to reinvest in their operations, grow their businesses, and create jobs.

One could say that 280E could be equally or more importantly about de-scheduling cannabis than about changing a tax code. This a vital step that policymakers can take to remove cannabis from the list of Schedule I drugs. The current classification of cannabis as a Schedule I drug is outdated and based on outdated stereotypes. This is also contributing to a massive roadblock with the potential to destroy many businesses in the legal market, which only helps the illicit market thrive. Removing it from the list of Schedule I drugs would enable researchers to study cannabis more effectively and provide a clearer understanding of its medical benefits and potential risks. It would also allow cannabis businesses to operate more freely and obtain financing from traditional lenders.

Creating a more supportive regulatory environment for the cannabis industry is critical to its success.

With the help of insurance professionals, tailored solutions, and supportive policymakers, the cannabis industry can continue to grow and contribute to the economy. Revising Section 280E and removing cannabis from the list of Schedule I drugs are essential steps that can be taken to support this critical industry.

Valerie has over 16 years of experience in the insurance industry with specialized niches in cannabis, real estate, and community associations. With experience working for companies such as McDermott Costa Insurance Brokers, AmWINS Group, Inc., Commercial Coverage Ins. Agency, and Colemont Insurance Brokers, Valerie has developed a love of helping clients navigate the world of insurance by creating an understanding of the value behind insuring their business. In addition to her professional work, Valerie serves as the CREW East Bay Chair on the Programs Committee, is a National Cannabis Bar Association member, NCIA member, and volunteers in East Bay communities with Richmond Grows Seed Lending Library to show people how to save vegetable seeds and grow their own food. In 2021, Valerie received the 2021 and 2022 CREW East Bay Connections Award and was a nominee for the Elevate 2021 Industry Impact award.

With a drive and passion for helping people, Valerie has gone back to her long-standing roots in the plant medicine industry and uses her unique lens of growing up surrounded by cultivators and sellers to validate her client’s business needs. Valerie strives to break the mold of how insurance and cannabis has partnered together to give back to the community she grew up in. With a strong insurance background and an in-depth knowledge of the cannabis industry, Valerie has been a trusted advisor for over 70 cannabis clients.

For more information on Liberty’s National Cannabis Practice Group, please reach out toValerie Taylor, Vice President (National Cannabis Practice Leader), The Liberty Company Insurance Brokers.

Service Solutions | 10.26.22 | Show Me the Money – The Current State of Cannabis Lending

NCIA’s Service Solutions series is our sponsored content webinar program which allows business owners the opportunity to learn more about premier products, services and industry solutions directly from our network of established suppliers, providers and thought leaders.

In this edition originally aired on Wednesday, October 26, 2022 we were joined by the experts from cannabis-focused financial institutions FundCanna, Safe Harbor Financial, and AVANA Companies to dive deep into the current state of cannabis lending with leading industry journalist John Schroyer of Green Market Report.

A decade after California and Colorado became the first adult use states, the regulated U.S. cannabis market encompasses over 70,000 cannabis-related businesses. Shockingly, most of those businesses still lack easy access to debt and other forms of growth and operating capital. From federal prohibitions and the impact of IRS regulation 280e, to state and local taxation issues, the costs of operating a regulated cannabis company continue to remain nearly unendurable.

Learn what may change in the coming six to 12 months so you’ll know how to access debt capital most cost-effectively in this ever evolving environment. No matter your place in the industry or the supply chain from cultivators, manufacturers, vendors, suppliers, distributors and retailers this conversation will provide the insights to meet your financial needs.

At the conclusion of the discussion our panel hosted a moderated Q&A session to provide NCIA members an opportunity to interact with leading minds from the financial services space, join today to contribute to future conversations!

Panelists:

Adam Stettner

Founder & CEO

FundCanna

Sundie Seefried

Founder and CEO

Safe Harbor Financial

02:13 – Equity vs. Debt: With equity dried up, should cannabis companies be looking at debt financing to grow now?

07:28 – Equity vs. Debt: What do borrowers need to do before approaching a debt provider (vs. an equity provider)?

13:25 – Equity vs. Debt: What can cannabis companies or entrepreneurs do to improve their overall credit worthiness prior to seeking capital?

17:16 – How has the interest rate increases by the Federal Reserve impacted capital markets (and the industry at large) in 2022?

26:07 – Audience Q&A: “If there’s “no reason not to have banking” for your cannabis business how can I easily (and inexpensively) establish and maintain a compliant bank account?”

28:56 – Lending: What significant lending challenges are your clients currently facing within the industry?

33:56 – Lending: What advice can you provide business owners for evaluating lenders that you should (or shouldn’t) work with and tips for avoiding predatory lending practices?

39:05 – Cannabis Reform: What impact do you expect President Biden’s recent announcement will have on the industry?

49:32 – Audience Q&A: “Are your financial institutions planning to offer lending and banking services in New York, New Jersey and other new markets?”

51:42 – Audience Q&A: “With the mindset of “Investors are betting on the Jockey not the Horse.” What type of CEO or founding team would be a red flag or not a viable investment?”

55:19 – Audience Q&A: “How can I start to shift my retail company from being primarily a cash-only business?”

1:05:03 – NCIA Member Appreciation Credit Sequence

Sponsored By:

Service Solutions | 9.27.22 | The Devil is in the Details: Claiming Your Employee Retention Credit as a Cannabis Business

NCIA’s Service Solutions series is our sponsored content webinar program which allows business owners the opportunity to learn more about premier products, services and industry solutions directly from our network of established suppliers, providers and thought leaders.

In this edition originally aired on Tuesday, September 27, 2022 we were joined by the experts from ERT Credit for an exclusive webinar outlining how cannabis businesses can take advantage of The Employee Tax Credit (or ERC) which has currently only been claimed by a small fraction of cannabis businesses, and most importantly, as a payroll tax credit is not subject to Section 280E.

Think your cannabis-related business does not qualify for COVID-19 relief funds worth up to $26,000 per employee.? You’ll leave the session with a roadmap for next steps to determine eligibility and maximize your claim so you don’t miss out on a potentially guaranteed refund worth hundreds of thousands of dollars and in some cases millions.

At the conclusion of the discussion our panel hosted a moderated Q&A session to provide NCIA members an opportunity to interact with leading minds from the cannabis accounting and technology space, join today to contribute to future conversations!

40:46 – Audience Q&A (If your business is still operating – what are the taxes due on the tax credit?)

42:04 – Audience Q&A (I was told that ERC money is not available for the cannabis industry due to 280e. How are you navigating that compared to others trying to provide the same services?)

44:31 – Audience Q&A (Does this apply to cultivation facilities also?)

46:42 – Audience Q&A (What if we apply and don’t receive our money or we are denied the credit?)

48:09 – Audience Q&A (What if my accountant/lawyer says I don’t qualify?)

49:41 – Audience Q&A (How can I find more details on how to navigate the 280e concerns?)

50:58 – Audience Q&A (So if you went out of business before or soon after getting the tax credit you would not have any (or minimal) tax impact from taking the tax credit?)

53:24 – Audience Q&A (Do I have to spend the money on my payroll? Or can I use it towards my other business expenses? Any other restrictions?) 54:26 – Audience Q&A (So is this a credit for my company towards next year or do I get an actual check like a refund?)

01:05:28 – NCIA Lobby Days 2023 Member Appreciation

Sponsored By:

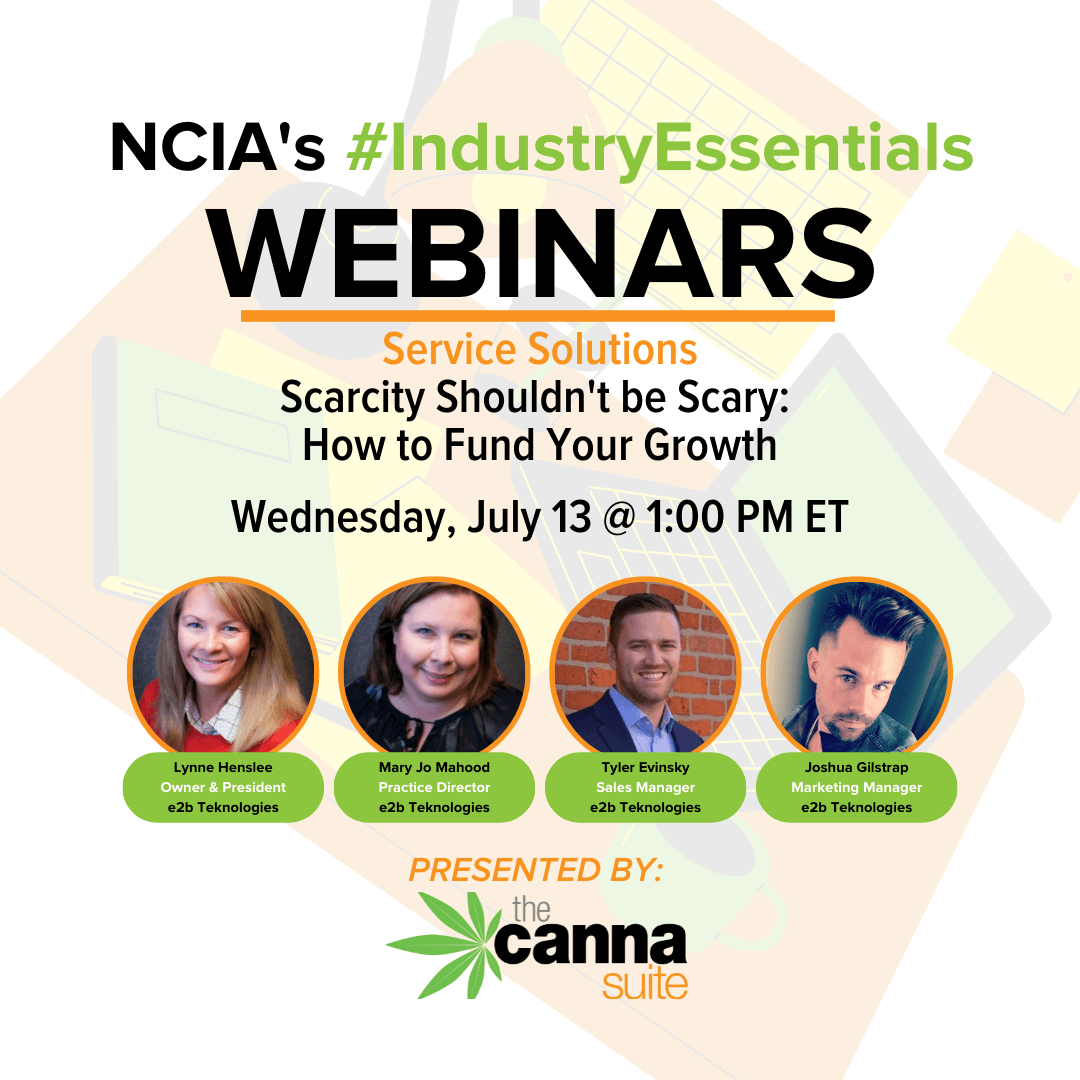

Service Solutions | 7.13.22 | Scarcity Shouldn’t be Scary – How to Fund Your Growth

NCIA’s Service Solutions series is our sponsored content webinar program which allows business owners the opportunity to learn more about premier products, services and industry solutions directly from our network of established suppliers, providers and thought leaders.

In this edition originally aired on Wednesday, July 13, 2022 we were joined by e2b Teknologies whose team of leading integration & technology experts discussed some easy steps to prepare your business for funding and accelerated growth. As you all know, competition was stiff for funding prior to 2022 but with the current economy and rising interest rates, capital is much harder to acquire today. You should be taking steps get noticed and get the MONEY you need to grow your business now.

After viewing you’ll walk away with a better understanding of:

• How to leverage a team properly

• What’s most important – It may not be what you think.

• What’s necessary in terms of reporting, compliance, and record-keeping

• Evaluating potential technology partners

Sit back and settle in for an informative and timely program outlining the challenges facing operators and how you can position yourself for success with the right tools to help succeed at scale.

Equity Member Spotlight: Banyan Tree Dispensary – Adolfo “Ace” Castillo

NCIA’s editorial department continues the Member Spotlight series by highlighting our Social Equity Scholarship Recipients as part of our Diversity, Equity, and Inclusion Program. Participants are gaining first-hand access to regulators in key markets to get insight on the industry, tips for raising capital, and advice on how to access and utilize data to ensure success in their businesses, along with all the other benefits available to NCIA members.

Tell us a bit about you, your background, and why you launched your company.

My name is Adolfo Castillo. People who know me call me Ace. Before I started my first cannabis business, I had a 10-year career in the banking industry. I started in a call center as a customer service associate. I then moved into a traditional banking center where I learned sales and eventually became the assistant manager. It was at the end of my tenure in 2008 that my Tia Eloise was diagnosed with terminal cancer. At the request of my mother, she asked me to get some cannabis in hopes that it would help her sister eat. Although it did not cure cancer, it really helped her appetite and gave her a bit of relief. Unfortunately, my Tia Eloise lost that battle, but it was the relief that I was able to provide that helped bring me peace when she passed away. This all happened around the same time that bill SB 420 was signed into California law, establishing statewide guidelines for Prop. 215. This law paved the way for cooperatives and collectives to begin operating legally in my city. It was at that moment that my love for cannabis became a passion. I felt a need to help more people gain access to cannabis, so I partnered with a friend of mine who sold weed and I took what I had learned about business and applied it to opening my first medical cannabis dispensary.

What unique value does your company offer to the cannabis industry?

I named the dispensary Banyan Tree after an experience I had in Maui about 13 years ago. It was my first visit to Maui so I decided not to bring any cannabis products to avoid any problems at the airport. When I arrived, I asked a few locals where I could find some good smoke and they all pointed me to the Banyan Tree. It was true. As soon as I found the Banyan Tree, I could tell this was the place to be. The smell was in the air and I met some really nice Hawaiians who were happy to hook me up. I want our guests to have the same experience when they visit our dispensary. Banyan Tree is a destination. A place where friends can meet to find quality cannabis.

As a local native, I understand the cannabis culture in my town. The legacy market has thrived for so long in Fresno. One of our biggest challenges will be convincing medicinal users and cannabis connoisseurs to buy their cannabis from a licensed facility and not from the streets. In order to create the best experience possible, it starts with a well-trained, knowledgeable staff. I am lucky to have two educators on my team who have helped me put together a robust employee development program that will ensure that the Banyan Tree staff will be primed for success.

My goal for Banyan Tree is to be the #1 dispensary to work for. I truly believe that the success of your business relies heavily on its employees. I want our employees to have purpose and feel proud of the work they do. Banyan Tree was built upon the idea of helping our surrounding community achieve wellness and enjoyment through cannabis. When you come to Banyan Tree, you will not be rushed, you will feel safe, your questions will be answered, and the price you pay will not shock you.

What is your goal for the greater good of cannabis?

I am hopeful that I will see full legalization in my lifetime. As a cannabis business operator, I would like cannabis to be recognized as a normal commodity and not this taboo substance that has so much negativity around it and red tape. As a business owner, I would like cannabis commerce to transact and be accepted without any special rules in regards to banking and filing federal income tax. As outdated stereotypes are finally fading away, more and more consumers view cannabis as an integral part of their health and wellness routine. I’m confident that in 20 years we will look back at the history of cannabis and just laugh at all the nonsensical rules surrounding cannabis in the early 2000s.

What kind of challenges do you face in the industry and what solutions would you like to see?

Most cannabis operations are running all-cash businesses because mainstream, national banking institutions are not willing to support a federally illegal industry. A small number of state-chartered banks and credit unions have offered financial services to compliant operations, but establishing these relationships continues to be a significant challenge for operators.

An equally frustrating financial challenge is IRS Tax Code 280E, which states that “no deduction or credit shall be allowed in running a business that consists of trafficking a controlled substance.” This archaic code impacts cannabis businesses across the nation, causing unnecessary fiscal and operational stress.

Why did you join NCIA? What’s the best or most important part about being a member through the Social Equity Scholarship Program?

I joined NCIA through the Social Equity Scholarship program to extend my network of cannapreneurs and to help develop best practices and guidelines that will shape the future of our industry. I would say for me, the best part of being a member of NCIA is the synergy. One of my favorite parts of the program is the “Power Hour.” Each week, Mike Lomuto hosts a zoom meeting dedicated to Social Equity members. It is where we have an opportunity to share ideas and find solutions to the issues we all face in our industry. I am very capable, but I recognize that by fostering relationships and collaborating with others in my industry, I can achieve far more than I could ever achieve on my own.

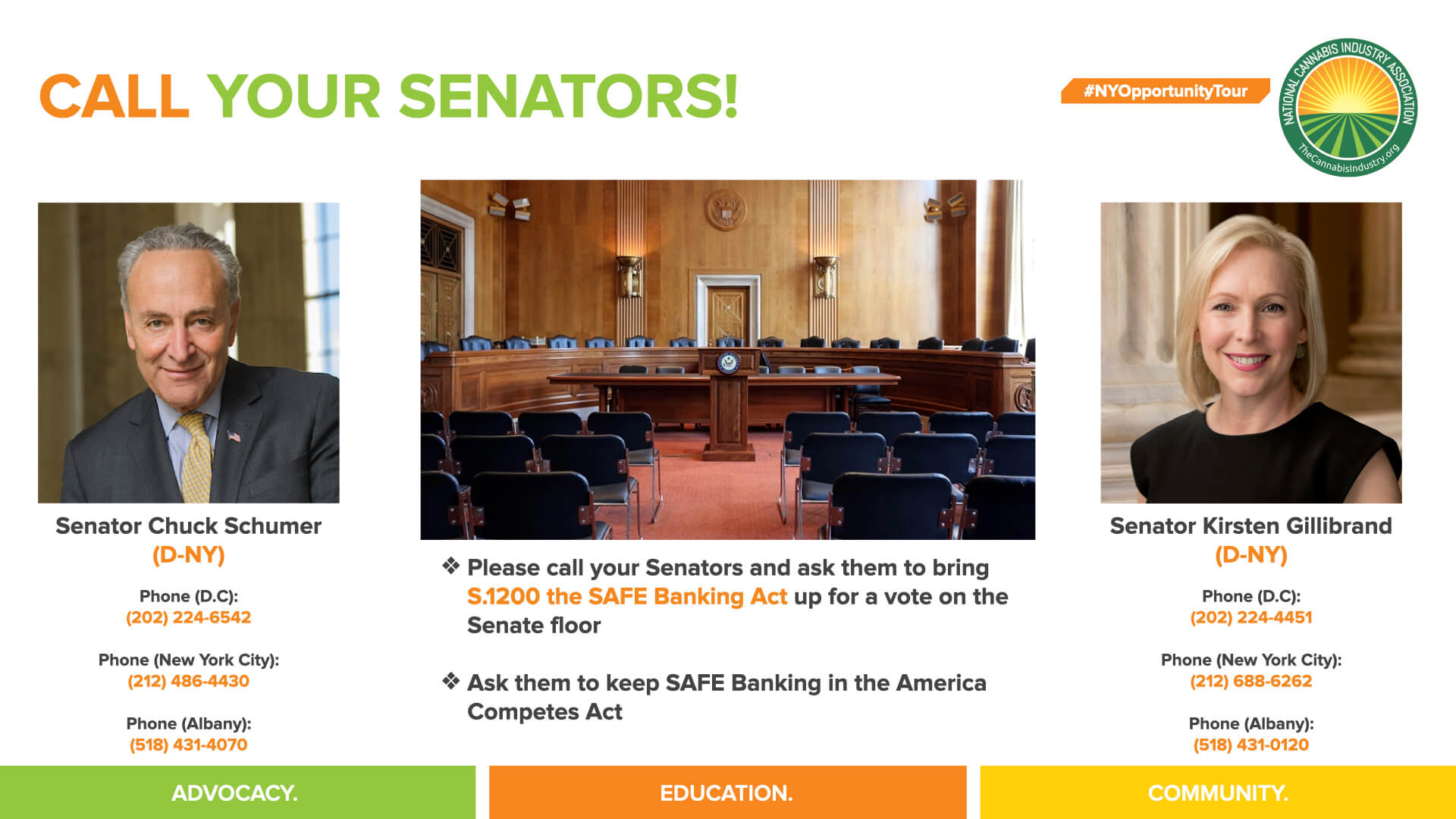

Positioned for Success – Highlights from the Insights & Influencers: NY Opportunity Tour

Any cannabis insider knows that New York is poised to become the next cannabis epicenter since legalizing last year. As such there is naturally incredible interest in learning about the business opportunities, how to best position yourself for success, as well as networking with potential future partners and clients. To meet these needs for our members and supporters, NCIA hosted the “Insights & Influencers: NY Opportunity Tour”, a weeklong series of events across New York featuring stops in Rochester, Albany and Brooklyn in partnership with founding members Canna Advisors, a trusted advisor to cannabis entrepreneurs who are starting or expanding a cannabis business.

(C) Sam C. Long / Honeysuckle Media, Inc.

Returning with our first in person events of the year, we couldn’t have been more thrilled to meet face-to-face with nearly 150 attendees who were either current or prospective business owners operating in New York and interested in expanding their operations or trying to break into the industry. With stops in Rochester, Albany, and New York City, the events brought together attendees from across the Empire State to not only learn about the developing regulatory landscape and opportunities to get involved with the burgeoning cannabis industry, but also the latest developments with NCIA’s work on federal cannabis policy.

(C) Sam C. Long / Honeysuckle Media, Inc.

Speakers were NCIA CEO and co-founder Aaron Smith and representatives from Canna Advisors including Bob Wagener, Vice President of Real Estate Development; Sumer Thomas, Director of Regulatory Operations; and Vincent DiMichele, Regulatory Content Manager. During the hour long presentation, numerous topics were covered that were relevant to business owners in the cannabis industry such as:

• The possibility of federal legalization and the work NCIA is doing to ensure small — or “main street” — cannabis businesses have a seat at the table as legislation is written

(C) Sam C. Long / Honeysuckle Media, Inc.

• Benefits of starting the license application process early and the importance of community engagement efforts

(C) Sam C. Long / Honeysuckle Media, Inc.

• Understanding zoning requirements and ensuring your business can operate in the best location possible

(C) Sam C. Long / Honeysuckle Media, Inc.

• Developing staffing needs and protocols so the team behind your operations is positioned for success and growth

• Engaging in public comment periods including the New York Office of Cannabis Management’s (OCM) current 60 day comment period open now through August 15 surrounding regulations for packaging, labeling, marketing, advertising, and laboratory testing of adult-use cannabis

Throughout the tour, representatives from the OCM were on-site to chat with participants, answer questions that attendees had, and generally get to know those interested in owning or operating a cannabis related business in the state. We are proud to facilitate those connections at our events time and time again, so that regulators and business owners alike can meet in person to build relationships which in turn helps break down the barriers to communication down the line.

Nevillene White, Manager of Community Relations and External Affairs for OCM, joined our Albany gathering right next door to The Egg performing arts venue located inside of Empire State Plaza. Throughout she was able to supplement the presentation by providing comments directly to crowd feedback during updates on the licensing process in the Capitol.

(C) Sam C. Long / Honeysuckle Media, Inc.

Trivette Knowles, Press Officer and Manager of Community Outreach for the OCM, was present in Brooklyn and commented ”We need more events like this to show people that cannabis touches all walks of life,” he said. “It’s part of the culture.”

(C) Sam C. Long / Honeysuckle Media, Inc.

NCIA’s Aaron Smith closed out each of the events with a final call to action for everyone in the room: Contact New York’s U.S. Senators Chuck Schumer and Kirsten Gillibrand to urge them to support the SAFE Banking Act and bring it to the floor for a vote. As the Majority Leader in the Senate, Sen. Schumer has the power to allow the legislation to be voted on but has not done so, stating a preference for more comprehensive legislation. Smith also discussed the Cannabis Administration and Opportunity Act (CAOA), which addresses federal legalization on a broader scale. A final version of that bill is still yet to be introduced however, and passage of the SAFE Banking Act would provide protections to financial institutions working with cannabis business and would have a positive impact on the cannabis industry while support for CAOA and comprehensive reform builds in Congress.

Of course we encourage anyone reading to take this call to action even further, and plan to join NCIA at our upcoming 10th Annual Cannabis Industry Lobby Days from September 13-14 in Washington, D.C. Find out more details and register online here.

We can’t thank all our members and supporters who attended the events on our “Insights & Influencers: NY Opportunity Tour” enough, as well as our co-hosts, Canna Advisors, for making these events possible!

(C) Sam C. Long / Honeysuckle Media, Inc.(C) Sam C. Long / Honeysuckle Media, Inc.(C) Sam C. Long / Honeysuckle Media, Inc.(C) Sam C. Long / Honeysuckle Media, Inc.(C) Sam C. Long / Honeysuckle Media, Inc.(C) Sam C. Long / Honeysuckle Media, Inc.

Interested in attending our next in-person event this Summer? Register now for the Colorado Industry Social taking place on Thursday, July 28 in Denver, CO.

Want to know how you can sponsor events like these? Please contact our Events Team at events@thecannabisindustry.org to explore possibilities.

The cannabis industry has grown exponentially as an increasing number of states have relaxed state law prohibitions on the use of cannabis for medical and recreational purposes. However, under federal law, cannabis remains classified as a Schedule I controlled substance under the Controlled Substances Act (CSA). This means that the production, distribution, and possession of cannabis remains illegal on the federal level.

Schedule 1 Status of Marijuana: State-Legal Cannabis Businesses and Application of Internal Revenue Code Section 280E

Cannabis businesses are treated differently from many other businesses for tax purposes. Under Internal Revenue Code (IRC) §280E (“280E”), which applies to a federal income tax filing, denies deductions and credits for amounts paid or incurred in carrying on the trade or business of cannabis. Cost of goods sold is allowable because it is not considered a deduction, rather it is a reduction of gross receipts (revenue) to arrive at gross profit.

A report published in March 2020 by the U.S. Treasury Inspector General for Tax Administration examined California and found that over 50% of marijuana companies had likely underpaid the IRS under IRC§ 280E. The report confirms the IRS is preparing to increase marijuana industry audits nationwide in response.

Currently, the method by which cost of goods sold may be deducted for producers is to use IRC §471(a). This provision discusses how to clearly reflect income by using an inventory method. Therefore, cannabis producers have less of a 280E problem than retailers and distributors.

After the passage of the Tax Cuts and Jobs Act (TCJA), effective for tax years beginning January 1, 2018, a provision was passed in the IRC §471(c). There are various opinions with advisors in the industry on whether this code section and method can be used for retailers and distributors. The idea behind IRC 471(c) is that “certain small businesses” can meet the gross receipts test of this subsection for any taxable year in which the corporation’s or partnership’s average annual gross receipts do not exceed $25,000,000 for the 3-taxable-year period ending with the taxable year that precedes such taxable year. Pursuant to IRC §448(c)(1), this type of small business may be able to use a “books and records” method for deducting all costs – rather than being limited to cost of goods sold only. In other words, if one uses 471(c)(1)(B) as an accounting method, in theory, they may also be able to deduct selling expenses and all other costs that were previously not allowed as deductions.

Assembly Bill 37, codified in §17209 of the California Revenue and Taxation Code

Each state in the U.S. is autonomous in that it has the authority to decide whether its income tax laws conform to §280E or not. On October 12, 2019, Governor Newsom signed into law AB 37, which overrides §280E through the following provision:

For each taxable year beginning on or after January 1, 2020, and before January 1, 2025, Section 280E of the Internal Revenue Code, relating to expenditures in connection with the illegal sale of drugs, shall not apply to the carrying on of any trade or business that is commercial cannabis activity by a licensee. – (CAL. REV. & TAX CODE § 17209 (2020). CAL. REV. & TAX CODE § 17209 (2020).

However, AB 37 only applies to state filings with the Franchise Tax Board and is currently only available until January 1, 2025. AB 37 has no impact on federal tax filings, which is where a majority of cannabis entities pay their income taxes with effective tax rates as high as 25% for corporate taxes and up to 37% for individuals.

The IRS Lacks Guidance for Cannabis Tax Payers

The IRS has not published nationwide guidance to taxpayers and tax professionals in the cannabis industry. In addition, cash-intensive business issues unique to the cannabis industry such as IRS §280E and banking limitations will remain unresolved unless and until there is uniformity through federal legalization. As a result, compliance-related issues continue to grow and negatively affect cannabis business owners who operate legally under individual state law.

Kaveh Newmen is an associate at Edlin Gallagher Huie + Blum who handles cannabis law general litigation, and trucking and transportation matters. Kaveh was admitted to practice law by the State Bar of California in 2021. Kaveh earned his J.D. from the University of San Diego School of Law in 2020, where he was a board member of the Criminal Law Society, the Immigration Law Society, the Middle Eastern Law Student Association, and served as an intern at the school’s Immigration Clinic. He is a first-generation Iranian-American and speaks Farsi.

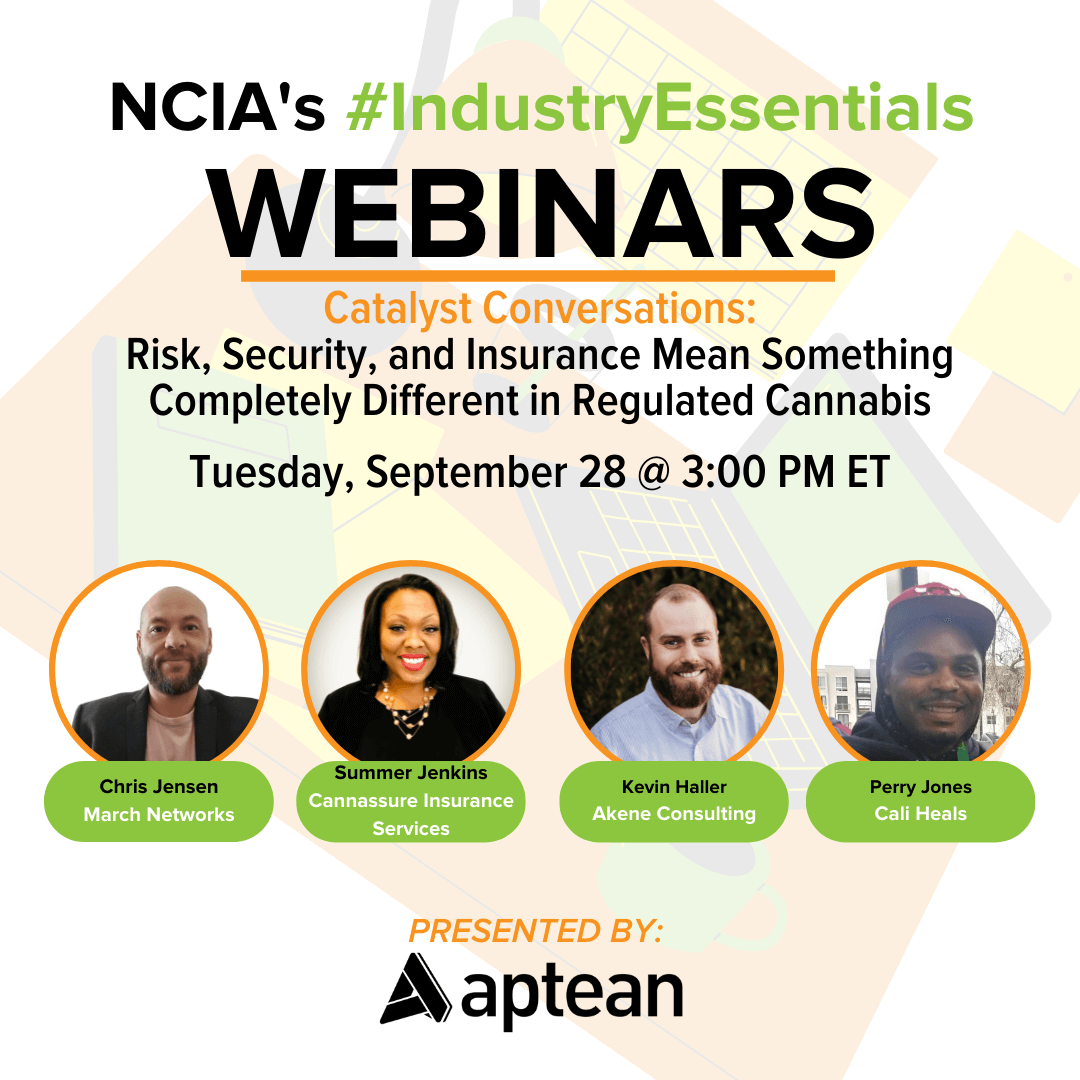

Catalyst Conversations | 9.28.21 | Risk, Security, and Insurance Mean Something Completely Different in Regulated Cannabis

NCIA’s Catalyst Conversations series is an advanced webinar series curated to give enrollees in our Social Equity Scholarship program the opportunity to network and gain access to valuable knowledge that will help them excel in the cannabis industry.

In this edition of our Catalyst Conversations series originally aired on Tuesday, September 28, NCIA’s Risk Management and Insurance Committee teamed up with the Diversity, Equity, and Inclusion Committee to create a powerful discussion every Social Equity operator should join in on.

Legacy and Social Equity operators face many hurdles. One of the biggest hurdles is creating a risk management strategy and gameplan in the regulated industry, which can prove to be very different from the risk management strategies that may have gotten them here in the first place. In the regulated industry, the greatest risks to survival aren’t always so obvious, and the ways to mitigate those risks can often seem too expensive, or even worse, the service providers may be difficult to trust. The still-existent impact of the War on Drugs cannot be underestimated in the role it plays in this dynamic.

During this webinar, we host a lively discussion about the very real threats to the survival of small cannabusinesses, and the ways to mitigate those risks.

Attendees will walk away with these key insights:

• Understand the current state of Security and Insurance in the regulated industry

• Get pragmatic information on what to look for when vetting Security and Insurance firms and coverage

• Learn how to incorporate simple tactics into your current business strategy.

• Understand how the impact of the War on Drugs and making the transition from Legacy markets may affect your outlook on Security and Insurance in a unique way, and what you can do about it

• Recognize the importance of assessing and mitigating financial risk in the regulated industry

A special thank you to the benefactors of NCIA’s Diversity, Equity and Inclusion Program which are listed below!

All businesses must adhere to tax rules and regulatory compliance, but for cannabis companies, the laws are significantly more challenging to navigate. The cannabis industry has specific tax rules that differ from other sectors, and failing to follow them can result in severe financial and legal implications.

At Green Space Accounting, we know that managing your finances as a cannabis company can be much more complicated than the average start-up. Keeping a compliant financial system in place is not always easy with constantly changing state laws and regulations.

Here are a few tips on how to avoid compliance issues with your budding cannabis business.

Have Your Business Documentation in Order

One of the first steps to staying compliant is to have all the appropriate financial information and licensing for your business on hand.

Always be prepared with copies of your cannabis license, information from your seed-to-sale tracking system, and your point of sale software records. Having this paperwork, along with legal documents like operating agreements, Articles of Incorporation or Organization, and EINs will ensure that you have a fully compliant relationship with your bank, as well as local and state government.

It’s also a good idea to have detailed records on all sales transactions within your business, especially ones dealing with cash. Cash is used more frequently in cannabis dispensaries than in other retail industries. Having proper cash-handling procedures in place can save you from theft and keep you ready for any unexpected auditing.

Stay up to Date with State and Local Regulations

It’s important to remember that regulations surrounding cannabis change over time, so monitoring your state legislature and all applicable state and local agencies is crucial to keeping your business compliant. By making yourself aware of the rules for the cultivation, manufacturing, and distribution of cannabis, you can avoid the risk of fines or legal action and build a better relationship with your local government, law enforcement, and, most importantly, customers.

One way to stay up to date with regulatory compliance laws is to consume state and industry news surrounding cannabis daily. Not only do these publications keep you informed on business and consumer trends, but they also avoid complicated legal jargon, speaking directly to business owners in a way that’s easy for them to understand.

Another great way to stay on top of state and local cannabis laws is to network and build relationships with your local regulators. While maintaining compliance internally is the biggest goal, creating an ongoing relationship with the regulators in your area can help you better understand the changes within the industry and the steps you can make to conduct business more transparently.

Develop SOPs, Training, and Reporting Systems

Think of these SOPs as a set of rules that all employees need to abide by to keep your company’s production, sales, and accounting processes consistent and safe. Having a set of standard operating procedures can help you recognize potential compliance issues and fix them before they occur. These procedures can include an employee handbook on proper handling and storage of cannabis consumables to installing a seed-to-sale tracking system for inventory management purposes.

The best way to stay on top of your SOPs is to create reports, checkbooks, and logs in all aspects of your operations to show regulators that you are a transparent business that has a complete understanding of your state’s compliance laws. Frequent compliance training sessions are also an effective way to educate your entire team on the legal and tax regulations associated with your business.

Cannabis Payroll

To avoid issues concerning payroll, installing time tracking software for employees is also a great way to keep your staff organized and stay on top of the 280E tax code. The 280E law denies cannabis businesses federal income tax deduction for operating business expenses, which means that the wages for some employees may be deductible, and some may not be. By introducing software where employees can specify the tasks they’re doing and track the salaries they’re receiving, you’ll stay compliant with the tax code and better understand the productivity your team is generating.

Frequently Audit your Business

Hiring an outsourced accounting team to audit your cannabis business is a great way to avoid any potential risks regarding compliance. Auditors serve as an additional, unbiased set of eyes that will examine all areas of your organization and identity aspects that might need improvement.

If you are looking to stay on top of the legal and tax regulations for your cannabis business on a tight budget, self-auditing your company is a great way to check whether or not your training, bookkeeping, and SOPs are being appropriately implemented.

Entrepreneurs who belong to the National Cannabis Industry Association can receive discounted access to an acclaimed compliance management platform created by Simplifiya, which gives licensed operators a self-audit checklist that helps them identify, track, and mitigate potential issues before it’s too late. The platform also provides templates for creating SOPs customized for each license type and tied directly to your state regulations.

The Bottom Line

Whether you are a start-up, a growing business, or a multi-state operator, complying with federal and state compliance laws is essential. By following the above tips and staying transparent with your employees, partners, and investors, you’ll be ready for any audit that comes your way.

Whether you’re looking for cash flow management, business planning, or internal controls, our team is dedicated to helping you achieve peace of mind when it comes to your company’s finances and compliance. We understand that the financial side of your business can be daunting, complicated, time-consuming, and most of all: stressful. You don’t need to go through it alone. Our team is prepared to help you achieve your financial goals. Whether you’re looking to earn more revenue, scale your business or achieve a little peace of mind, you can trust Green Space Accounting to guide you.

Video: NCIA Today – July 9, 2021

NCIA Deputy Director of Communications Bethany Moore checks in with what’s going on across the country with the National Cannabis Industry Association’s membership, board, allies, and staff. Join us every Friday on Facebook for NCIA Today Live.

Registration to our Midwest Cannabis Business Conference in Detroit is now open with special limited-time super early bird pricing on tickets available, head to www.MidwestCannabisBusinessConference.com today!

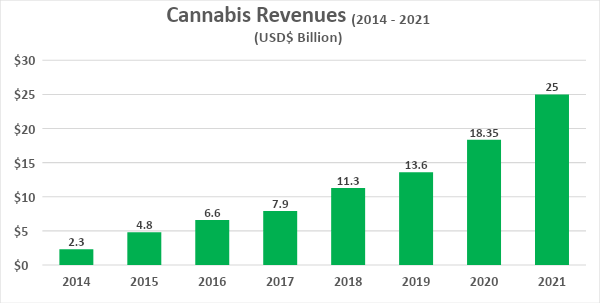

Mid-Year Update on 280E and its Impact on the Cannabis Retail Sector

by Beau R Whitney, NCIA’s Chief Economist

The first half of the year was a strong one for cannabis revenues. After a strong first quarter, with $5.9 billion in revenue, cannabis retailers are experiencing continued growth in Q2 with preliminary results coming in at $6.2 billion to $6.5 billion.

If this trend remains in the second half of the year, the cannabis retail sales are projected to be $24.5 to $25 billion for the year. This would reflect another cycle of 35% year-over-year growth.

Source: Whitney Economics, Leafly

Strong growth in the first half of the year, does not necessarily mean huge profits for the cannabis industry.

While the industry has seen strong growth over the past year, this does not necessarily mean that the industry as a whole is in good shape. Retailers are struggling to make profits due in a large part to federal taxation. IRC 280E does not allow entities conducting business in federally illicit trade, such as cannabis, to write off common and ordinary deductions from their federal taxes. As a result, cannabis operators pay significantly more taxes than other businesses. This has long been an issue with the cannabis industry and organizations such as NCIA has been working tirelessly to address this, but as long as it remains a federal policy it will be negatively impacting the industry.

Cannabis retailers are taking the brunt of federal tax policy.

With over $12 billion in first-half revenues, cannabis retailers will be on the hook for $1.2 billion in federal taxes for the first half of the year alone. This is $756 million more than what “normal” businesses would pay. Cannabis retailers are forecasted to pay over $1.5 billion more in taxes in 2021 and, when combined with the rest of the supply chain, will pay over $2.2 billion in additional taxes in 2021.

280e Example of Impact on Retail

Normal Business

280E Business

Comment

Retail mid-Year Revenue

$12,000,000,000

$12,000,000,000

Based on data from Whitney Economics

Cost of Goods Sold (COGS = 50%)

$6,000,000,000

$6,000,000,000

Ordinary and Necessary Expenses (30%)

$3,600,000,000

$3,600,000,000

Not allowed under 280e

Real Pre-Tax Profit w/o 280e

$2,400,000,000

$2,400,000,000

Taxable Profit

$2,400,000,000

$6,000,000,000

Big difference in taxable rates

Fed Tax @21% *

$504,000,000

$1,260,000,000

Retailers pay 150% more

Effective tax rate

21.0%

52.5%

Some effective tax rates approach 60%-70%

Net Annual Profit (Before State Tax and Debt Service)

$1,896,000,000

$1,140,000,000

A difference of $201,000 per year per retailer

Source: Whitney Economics *Assumes taxed at C-corporation rates

The effective tax rate is forecasted to increase with corporate tax increases.

The effective tax rate increases significantly for retailers and in many cases exceeds 60% to 70%. The level of additional taxes that cannabis operators pay, over the course of the next five years, will increase by an average of $630 million per year for the industry if the business tax rates increase from 21% to 28%. Depending on how corporate tax policy negotiations are settled, things may go from bad to worse for cannabis retailers.

Cannabis retailers are struggling to make ends meet.

Based on sales data from 2020, there were over 7,550 licensed cannabis retailers in the U.S. with each retailer generating an average of $2.4 million per year. This is right around the amount of revenue required to be a sustainable retail business. In 2021, there have been roughly 1,000 more retailers licensed and even with an increase in sales, retailers are only forecasted to average $2.7 million per year.in sales. In fact, in 13 states, retailers are not projected to average the $2.4 million per year to remain viable. While retailers in some states may be OK, other retailers are not able to make ends meet.

What do these numbers tell us?

IRC 280E will reduce cannabis retailers cash flow by $200,000 in 2021 and that $200,000 would go a long way in shoring up the finances and provide retailers with the breathing room they need to remain viable. 280E reform would allow retailers to pay for health care for more employees, hire more workers and expand their business. However, in the current environment, many cannabis operators will continue to struggle.

The key message here is that retailers are under duress due to 280E and policy reform in the area of federal taxes may make the difference between success and failure. The time for reform is now, before it is too late.

Learn more in a recent NCIA Fireside Chat webinar with an all-star panel of accounting experts and operators to dive deep into all things 280E.

Supreme Court of Cannabis?

Photo By CannabisCamera.com

By Michelle Rutter Friberg, NCIA’s Deputy Director of Government Relations

While it’s become commonplace to hear cannabis come up in the halls of Congress, and increasingly so in the White House, there’s one branch of government that has been quieter on the topic: the Supreme Court (SCOTUS). However, this week, conservative Justice Clarence Thomas changed that when the court actually declined to weigh in on a 280E case.

Towards the end of 2020, a Colorado medical cannabis dispensary decided to ask the U.S. Supreme Court to review a lower-court decision that allowed the IRS to obtain business records in order to apply the 280E provision of the tax code. (Fun fact: NCIA member Jim Thorburn, of the Thorburn Law Group, was actually the counsel on record for this appeal!) According to the filings, the IRS overstepped its authority and also violated the company’s Fourth Amendment privacy rights. Some of the questions the company took to the highest court in the land:

Does the Fourth Amendment protect taxpayers from having confidential information released to the IRS and federal law enforcement authorities?

Does the application of Section 280E to state-legal marijuana businesses violate the federal constitution?

Again, while SCOTUS declined to consider this appeal, Justice Thomas took issue with the underlying state/federal discrepancy in the country’s cannabis laws and issued a searing statement. He specifically discussed a 2005 ruling by SCOTUS in a case called Gonzales v. Raich. In this ruling, the court narrowly determined that the federal government could enforce prohibition against cannabis cultivation that took place wholly within California based on its authority to regulate interstate commerce. Check out a few excerpts from Justice Thomas’ statement below:

“Whatever the merits of Raich when it was decided, federal policies of the past 16 years have greatly undermined its reasoning. Once comprehensive, the Federal Government’s current approach is a half-in, half-out regime that simultaneously tolerates and forbids local use of marijuana. This contradictory and unstable state of affairs strains basic principles of federalism and conceals traps for the unwary.”

“Given all these developments, one can certainly understand why an ordinary person might think that the Federal Government has retreated from its once-absolute ban on marijuana. See, e.g., Halper, Congress Quietly Ends Federal Government’s Ban on Medical Marijuana, L. A. Times, Dec. 16, 2014. One can also perhaps understand why business owners in Colorado, like petitioners, may think that their intrastate marijuana operations will be treated like any other enterprise that is legal under state law.”

“As things currently stand, the Internal Revenue Service is investigating whether petitioners deducted business expenses in violation of §280E, and petitioners are trying to prevent disclosure of relevant records held by the State. In other words, petitioners have found that the Government’s willingness to often look the other way on marijuana is more episodic than coherent.”

“This disjuncture between the Government’s recent laissez-faire policies on marijuana and the actual operation of specific laws is not limited to the tax context. Many marijuana-related businesses operate entirely in cash because federal law prohibits certain financial institutions from knowingly accepting deposits from or providing other bank services to businesses that violate federal law. Black & Galeazzi, Cannabis Banking: Proceed With Caution, American Bar Assn., Feb. 6, 2020. Cash-based operations are understandably enticing to burglars and robbers. But, if marijuana-related businesses, in recognition of this, hire armed guards for protection, the owners and the guards might run afoul of a federal law that imposes harsh penalties for using a firearm in furtherance of a ‘drug trafficking crime.’”

“Suffice it to say, the Federal Government’s current approach to marijuana bears little resemblance to the watertight nationwide prohibition that a closely divided Court found necessary to justify the Government’s blanket prohibition in Raich. If the Government is now content to allow States to act “as laboratories” “‘and try novel social and economic experiments,’” Raich, 545 U.S., at 42 (O’Connor, J., dissenting), then it might no longer have authority to intrude on “[t]he States’ core police powers . . . to define criminal law and to protect the health, safety, and welfare of their citizens.””

Just to be clear, these statements don’t change the law of the land, nor do they indicate formal policy developments. They do, however, show that the constantly shifting public perception of cannabis is affecting the way we as a society think about marijuana, which will, at some point, translate into policy. It’s no small feat that one of the most conservative justices on the Supreme Court has weighed in so substantially on this topic. Continue the momentum and join the movement with NCIA!

Labor Supply Shortage Represents a Significant Risk to the Cannabis Industry in 2021

by Beau Whitney, NCIA’s Chief Economist

Supply tightness in the labor market represents a significant risk to cannabis operators heading into the summer months. With the potential of wage inflation adding to the costs of businesses, many operators that are struggling to make ends meet due to the economic stresses associated with 280E now face higher labor costs. This labor tightness and higher costs could not have come at the worst time.

The recent U.S. Bureau and Labor Statistics jobs report for May, published on Friday, June 4, 2021, indicated that there were 559,000 jobs added in the U.S. economy. This amount was lower than what analysts had predicted, but still strong nonetheless.

The report also showed that the labor force participation rates held steady which is a good sign that people are not getting too frustrated with their job search. The BLS data also indicated that there are still 9.3 million workers unemployed. Even with these higher numbers of displaced workers, this level is roughly 3.6 million workers higher than it was pre-pandemic when unemployment was at record lows. Considering that 1.1 million workers are on temporary layoff status, a remaining 2.5 million delta is a significant improvement relative to the 18.0 million workers displaced in April of 2020.

While there are differing opinions on policy on how to support the unemployed, the key point here is that the labor force is significantly tighter than what most believe and this could become a major issue for the cannabis industry.

Why should cannabis operators care about a BLS update on employment?

Ever since the great recession, there have basically been more workers than jobs. As a result, employers could pick and choose who to hire and offer them lower wages. This recent job report indicates that now there are more jobs than workers, so workers now have the upper hand when it comes to supplying their labor. This is resulting in wage inflation and labor shortages.

This should be a concern for cannabis operators. Labor is one of the highest costs for operators and if wages continue to rise, this will put a squeeze on already slim margins. Reduced labor availability is already being felt across the country and could become very acute as more labor is required to handle increased retail sales and as the outdoor cultivation industry heads into harvest season. Product manufacturers and retailers are already seeing spot shortages even in states where cannabis operators receive living wages such as in Oregon and Colorado.

Those with more resources can afford to pay higher wages.

In reaction to these labor shortages, some MSOs are offering incentives and sign-on bonuses in order to attract workers, even for positions not requiring highly skilled workers. Unfortunately, smaller businesses may not be able to afford these types of incentives. As a result, this will continue to create competitive advantages for MSOs and to generate opportunities that favor larger firms over smaller ones.

What impact is there beyond higher costs?

Higher costs are not the only concern for cannabis operators. The heavy burden associated with paying higher federal business taxes due to 280E is already driving smaller operators out of the market or forcing them into consolidation with larger, well-financed firms. Smaller entities already have higher costs. The additional risks associated with labor shortages and higher wages could force more operators who are on the edge, into consolidation as well.

What should smaller operators do in response to higher wages?

Operators who cannot absorb the higher costs for labor, may need to find additional areas in which to cut costs. Unfortunately, this may involve doing more with less (fewer workers), bringing in automation, or reducing product offerings (lower inventory overhead). A common area of cost-cutting is also healthcare, but in an environment of high competition for a limited labor pool, reducing benefits may not be an option.

Federal tax reform would help considerably

While many other programs at the federal level have helped struggling businesses outside of the cannabis space, federal tax reform could be a simple, yet elegant solution that would provide widespread relief to struggling cannabis operators and free up cash flow to help offset wage increases.

In the meantime, the anticipated growth in the overall market may decelerate slightly as the industry encounters headwinds as we head into the summer and fall.

NCIA is working with members of Congress to highlight how critically important sound policy is to cannabis operators across the country and how tax reform makes good economic sense. Bringing the voices of cannabis business owners to congress is a very powerful tool in the effort to reform cannabis laws. Now it is up to Congress to act.

Member Blog: IRC Section 471(c) of the TCJA May Mitigate the Curse of 280E for the Cannabis Industry

On March 30, 2020, the Treasury Inspector General for Tax Administration issued a report titled “The Growth of the Marijuana Industry Warrants Increased Tax Compliance Efforts and Additional Guidance.” The 53-page report discussed several different topics, including that the IRS should conduct more audits under Section 280E, and this discussion focuses on Section 471(c).

The report states that certain qualifying cannabis taxpayers, who would otherwise be subject to business expenses being disallowed under Section 280E, could potentially account for their inventory under Section 471(c) using a method that would classify most or all of their expenditures as inventoriable costs and avoid Section 280E’s disallowance of such expenditures. Accordingly, as all the costs would be capitalized into inventory, they would then reduce taxable income as the inventory was sold. In other words, expenditures previously disallowed under Section 280E would be part of the cost of goods sold and allowed as a reduction of gross receipts. There was no public comment from the IRS in the report on the potential that 471(c) may eliminate 280E.

Before continuing to provide our additional comments, it is important to mention the impact of Section 471(c) on Section 280E has not been reviewed by the Courts and the Inspector General also stated that necessary guidance addressing 471(c) is lacking from the IRS. As such, the impact cannot be stated in certain terms.

The curse of Section 280E on the cannabis industry cannot be overstated – some businesses actually end up paying more in tax than they make and Section 280E can turn an economic loss into a taxable gain. This seemingly unconstitutional result has been justified by the courts and IRS under a very old principle of taxation that “deductions are a matter of legislative grace.” New Colonial Ice Co. v. Helvering, 292 U.S. 435, 440 (1934) Legislative grace, according to these authorities, means the legislature has the power to deny all deductions, if they so choose, and it should be said that the limitation of such grace, under the 16th Amendment to the US Constitution, is that 280E cannot disallow costs of goods sold. With Section 471(c), however, legislative grace appears to be on the side of the cannabis industry because, as discussed below, Congress created Section 471(c) and it appears to allow inclusion of deductions into the cost of goods sold where they can’t be disallowed under Section 280E.

The Code states that Section 471(c) allows a small taxpayer, one with less than $25 million in revenues, who is not a tax shelter or public company to account for inventory according to their applicable financial statements, or absent applicable financial statements, according to the actual books and records of the taxpayer. For a qualifying business that doesn’t have applicable financial statements, if their books and records include deductions in COGS, then these deductions may not be subject to 280E.

Question #1 – What are applicable financial statements, what does it mean to have them, and if a taxpayer does not have applicable financials statements what are the books and records of the taxpayer prepared in accordance with the taxpayer’s accounting procedures?

It is our opinion that under IRC § 451(b)(3) if a taxpayer is required to issue audited financial statements in accordance with generally accepted accounting principles (GAAP) for credit purposes, to owners, or for any other nontax purpose, they have applicable financial statements. It would seem that “any other nontax purpose” would include audited GAAP statements required to be issued to state regulatory agencies. As such, because GAAP requires accounting for inventory in a manner similar to Section 471(a), taxpayers who have Applicable Financial Statements appear to be precluded from adding costs disallowed under Section 280E into COGS pursuant to Section 471(c). Of concern are states that require license holders to provide their licensing agency with audited financial statements. However, if the state doesn’t require GAAP financials, then the “Applicable Financial Statements” provision shouldn’t be a problem.

If the taxpayer does not have applicable financial statements, then they are allowed to account for inventory for tax purposes in the same way as they account for inventory on their internal books and records. Thus, their books and records would have to mirror their method of accounting for tax purposes.

Question #2 – Could a small cannabis company, who is not issuing applicable financial statements in accordance with GAAP and is subject to 280E, establish a method of accounting for inventory in which they consider all or most expenditures of the company to be inventoriable costs? If so, does characterizing these otherwise nondeductible costs as inventoriable costs change the nature of the expenditures from non-deductible business deductions to deductible costs of goods sold when the inventory is sold?

As noted above, there is currently no guidance from the IRS regarding this question and, we should assume, that the IRS will not acquiesce to the position that 471(c) eliminates 280E. So, let’s consider the arguments the IRS might make. First to consider is the Service’s conclusion in Chief Counsel Memorandum Number 201504011 regarding Sec 263A. Early on, cannabis taxpayers attempted to use Sec 263A to capitalize general and administrative costs, otherwise subject to 280E, into inventory and then deduct them as part of COGS. This does sound somewhat similar to the approach we are looking at under 471(c).

The IRS concluded in CCA 201504011 that Sec. 263A would not allow an expense disallowed under Section 280E to be added to COGS because of “flush language” added to Sec. 263A(a)(2) in a subsequent congressional amendment. The flush language states:

Any cost which (but for this subsection) could not be taken into account in computing taxable income for any taxable year shall not be treated as a cost described in this paragraph.

The U.S. Tax Court agreed with the Chief Counsel memo in several opinions including Patients Mutual Assistance Collective Corporation d.b.a. Harborside Health Center v. Commissioner.

However, where this language was fatal to the cannabis industry’s attempt to use Section 263A to its benefit – it may help in the case of Section 471(c). It appears to have been necessary for the U.S. Congress to add the Flush Language to Section 263A to prevent the inclusion of otherwise disallowed expenses into COGS. There is no equivalent language added to Section 471(c) and so the argument is that in the absence of an equivalent provision, Section 471(c) can be used to include expenses disallowed under 280E into COGS where they can be used to reduce taxable income.

Another argument the IRS may make is that Treas. Reg. § 1.61-3(a) prevents the inclusion of deductions into cost of goods sold because the regulation states that Gross Income is determined without subtraction of “…selling expenses…” However, Section 1.61-3(a) is part of the Treasury Regs defining gross income and its reference to the non-inclusion of “selling expenses” is from the regulations under Section 471(a). Section 471(c) specifically states that Section 471(a) does not apply (which include the regulations) and a taxpayer’s method of accounting for inventory under Section 471(c) does not fail to accurately reflect income. And, Section 471(c) is a higher authority than the regulations. Thus, it appears that Section 471(c) trumps Treas. Reg. § 1.61-3(a).

Question #3 – Should a taxpayer, eligible to use 471(c) to account for inventory file their tax return taking positions regarding 471(c) as described in this article?

Every taxpayer is different, and accounting for inventory under Section 471(c) is not right for everyone in the cannabis industry. It is also important to understand that it may not work and for taxpayers who use the method to do so with caution and understanding. However, below is a list of issues to discuss with your tax professional:

What is your tolerance for risk and a legal dispute with the IRS? Such a dispute could be time-consuming and costly.

If 471(c) is proven not to eliminate 280E – how will you manage additional tax, interest, and possibly penalties?

Should the position be disclosed as part of your tax filing?

Does the entity have applicable financial statements?

Is the cannabis business a tax shelter?

How aggressive does management and ownership want to be regarding the position?

How will management accomplish the necessary accounting and records to support such a position?

In summary, 471 (c) has left the cannabis industry with several questions and definitive answers are probably not immediately available. License holders should work closely with their advisors as they navigate these questions. But, there is a possibility that Section 471(c) eliminates Section 280E for qualifying taxpayers. Cannabis businesses should take the necessary steps to understand it and protect their ability to benefit from Section 471(c) if it does work.

The Bridge West and GreenspoonMarder teams work tirelessly to understand the tax and accounting issues facing businesses in the cannabis industry and provide the best possible solutions to their clients.

To discuss any of the questions within this article please feel free to contact Calvin Shannon, Nick Richards or any of their team members.

Calvin Shannon is a Pricipal of Bridge West and has over 17 years of experience providing tax, audit, estate planning and trust services. Calvin is skilled at understanding client’s challenges and working with them to develop and implement innovative and unique solutions. Assists organizations to address the industry’s unique and ever-evolving issues. He enjoys having the opportunity to work with cannabis clients to understand their business needs, and to provide timely solutions

Nick Richards is a Partner in the Tax practice group at Greenspoon Marder LLP. He represents individuals and businesses in tax audits & trials, M&A, in managing tax debt, and he advises cannabis companies, owners and investors regarding tax and regulatory compliance matters. Mr. Richards has been a tax attorney for more than twenty years beginning his career with the IRS where he was a leading trial attorney, a Chief Counsel advisor, and a Special Assistant United States Attorney.

With his broad experience and understanding at all phases of the tax system, from reporting and assessment through appeals, court, and tax debt resolution, Mr. Richards achieves successful legal solutions tailored to his individual client’s needs. Mr. Richards also teaches tax attorneys and CPAs throughout the US and he is an Adjunct Professor of Law at the University of Denver, Graduate Tax Program, where he teaches State and Local Tax and Civil and Criminal Tax.

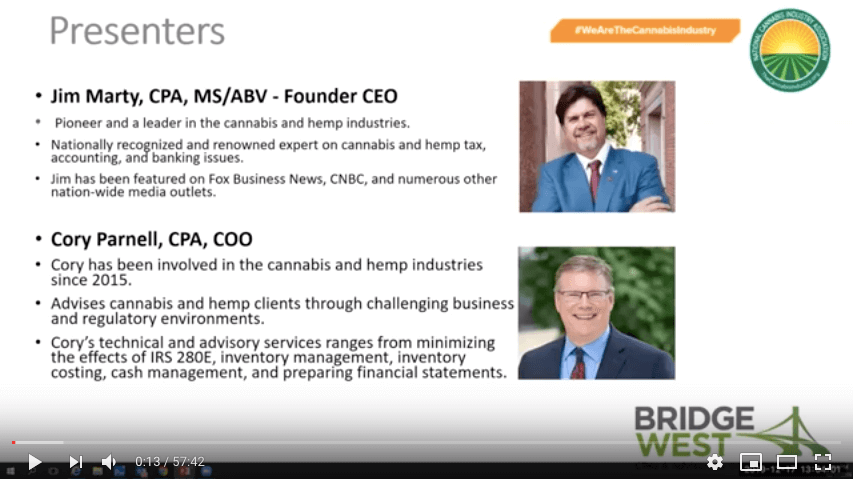

Webinar Recording: 280E Mitigation – What You Need To Know

Watch this webinar recording in case you missed the live presentation from December 17.

Legal cannabis has been spreading across the United States for over 10 years now. How has the industry been viewed in the eyes of the IRS? The cannabis industry has consistently lost in tax court against the IRS. Can these businesses be profitable on an after-tax basis? Do management companies help with profitability? Jim Marty and Cory Parnell of Bridge West LLC, CPAs and Consultants to the cannabis industry will explore these questions in light of recent tax cases.

Learning Objectives:

1. The session will help attendees understand the implications of recent Tax Court decisions that involve IRS Code Section 280E.

2. Learn how to avoid double taxation with related party management companies.

3. Explore the Eighth Amendment to the U.S. Constitution regarding excessive fines and penalties. Hear the arguments that conflict with 280E.

4. In light of the above, learn how C-Corporations can help protect again personal liability for dispensary income taxes.

Top Ten Reasons NCIA Supports De-Scheduling Cannabis

Today, the House Judiciary Committee (Subcommittee on Crime, Terrorism and Homeland Security) is holding a hearing on marijuana policy reform proposals and related social equity provisions. While NCIA supports the STATES Act and other incremental approaches to reform, we strongly prefer a longer-term approach that includes de-scheduling cannabis and the inclusion of robust social equity provisions. Let’s get this right the first time around.

Below are the top ten reasons to support de-scheduling:

1. De-scheduling is good public policy because cannabis should not be classified alongside dangerous drugs like heroin and methamphetamines, and cannabis has proven medicinal properties and is safer for adults than alcohol and many over-the-counter medicines.

2. De-scheduling automatically solves the banking problems plaguing the cannabis industry and automatically cures issues related to the unfair tax provisions imposed by 280E.

3. De-scheduling removes many of the roadblocks in the way of creating an industry that prioritizes and promotes social equity and inclusion.

4. De-Scheduling would allow for cannabis to be transported across state lines in accordance with interstate trade compacts, opening opportunities for licensed growers to get their product into more markets and to stabilize supply and demand issues currently facing some state markets.

5. De-scheduling takes regulatory authority away from the DEA and creates opportunities for the federal government to regulate marijuana through FDA and Treasury with regimes that are more appropriate, given the relative harm of cannabis compared to other adult products.

6. De-scheduling immediately makes federal research and grants possible.

7. De-scheduling immediately changes current immigration policy that prohibits people with “bad moral character” from applying for citizenship because of their work in the cannabis industry.

8. De-scheduling allows for the provision of bankruptcy protection for cannabis-related businesses.

9. De-scheduling would allow veterans access to plant-based medicine and retention of VA benefits if they choose to use medicinal marijuana.

10. De-scheduling still allows for state autonomy while simultaneously providing for federal continuity.

Member Blog: Tax Court Decision for Harborside Health Center

The Tax Court’s recent decision in Harborside Health Center v. Commissioner is more bad news for the cannabis business community. The taxpayer, a prominent California dispensary, was assessed approximately an additional $30 million in tax by the IRS for the years 2007 to 2012, years in which Harborside had total revenue of approximately $102 million. Harborside lost, so it will have to pay that amount plus also pay another 20% of the tax owed in accuracy-related penalties – the Tax Court did not decide the penalty issue and left it for a later opinion. At this point, Harborside can either pay the tax (plus possibly penalties) or appeal to the Ninth Circuit Court of Appeals.

GROUNDS OF THE DECISION

The court decided against Harborside on every single argument made by its counsel. Three of the issues are straightforward:

The doctrine of res judicata didn’t apply, so the fact that a civil forfeiture case against Harborside had been dismissed with prejudice did not prevent the IRS from assessing a tax liability.

The language in Section 280E of the Tax Code that deductions are disallowed to a trade or business that “consists of trafficking in controlled substances” applies to businesses that have more than the one activity of trafficking. Harborside argued that “consists of” means the business must ONLY be trafficking for the disallowance to apply, and the Tax Court rejected that interpretation.

Harborside had only one trade or business so it could not deduct any expenses related to a separate trade or business. The taxpayer had argued it had multiple lines of business, but the opinion held that Harborside didn’t make significant profits from any of the other claimed lines of business so there was only one business.

MOST IMPORTANT CONSEQUENCE OF DECISION