Committee Blog: Banking Guide for Cannabis Industry Veterans

Published by NCIA’s Banking & Financial Services Committee (BFSC)

As a veteran of the cannabis industry, you’re already familiar with the regulatory complexities and operational risks that come with running a legal cannabis business. But even as the industry matures and expands—projected to reach $52 billion by 2026—banking remains one of the most persistent and misunderstood challenges.

Despite being legal in many states, cannabis remains a federally prohibited substance. That means financial institutions must follow federal laws, including the Bank Secrecy Act (BSA), Anti-Money Laundering (AML) protocols, and FinCEN guidance, if they choose to work with cannabis-related businesses. This legal conflict results in higher compliance costs, greater documentation requirements, and fewer financial services available to cannabis operators.

Still, legitimate banking options are becoming more accessible. Businesses that operate transparently and work with proper compliance systems can secure reliable financial partnerships—without resorting to risky workarounds that often lead to frozen funds or account closures.

Understanding the Rules of the Game

Cannabis business owners must understand that banks operate under an entirely different set of rules. Even if your business is licensed and fully compliant at the state level, banks must verify that you also meet federal standards. This includes full documentation of your business structure, licensing, tax status, and ownership—especially for individuals holding 25% or more equity in the company.

Financial institutions also require evidence that you follow local rules, such as zoning approvals and municipal permits. The banking industry takes particular interest in ownership transparency, as previous cannabis operators have attempted to hide beneficial ownership behind shell companies or layered corporate structures. While these tactics may have delayed scrutiny in the past, they are now seen as high-risk and typically result in terminated accounts.

Laying the Groundwork: Due Diligence and Documentation

Before engaging with a financial institution, be prepared to undergo a deep due diligence process. Banks will expect to review your business formation documents, operating agreements, state and local cannabis licenses, tax filings, SOPs for compliance and security, and detailed financial statements. They may also request proof of your inventory tracking system, insurance coverage, and even video footage or plans related to your cash-handling procedures.

The more organized and transparent your records are, the more confident a bank will feel in your business. This includes having an accurate and up-to-date organizational chart, verifying all ownership interests, and providing supporting evidence for your business’s revenue, investments, and cash flow.

Proving Your Controls: AML and Seed-to-Sale Integration

Because cannabis remains a cash-intensive industry, banks are especially concerned about your ability to prevent money laundering. You’ll need to demonstrate that you have systems in place to document and trace every major transaction, identify suspicious activities internally, and track the movement of cash throughout your business. Written policies, transaction logs, and surveillance data are all important tools in meeting these requirements.

An essential part of building banking credibility is aligning your financial statements with your seed-to-sale inventory tracking system. If a bank asks how your product movement matches your reported income, you should be able to demonstrate a direct connection. Inconsistencies raise red flags, while tight integration builds trust.

Financial Discipline and Tax Transparency

Using cannabis-specific accounting software and experienced CPAs is no longer optional—it’s expected. Your records should be clear, professional, and separated from any non-cannabis revenue streams you might have. Maintaining excellent tax compliance is also crucial, particularly around IRS Section 280E, which restricts the deductions cannabis businesses can claim. Banks want to see not only that you’re filing taxes properly, but that you understand and proactively manage your tax obligations.

Relationship Management: Treat Your Bank Like a Partner

Just as you would with a supplier or regulator, maintaining a proactive relationship with your financial institution is key. Assign specific team members to handle banking communications. Keep your bank informed about changes in your business—whether that’s a new owner, a license renewal, or a change in address. Fast, accurate responses to information requests demonstrate your professionalism and commitment to compliance.

By contrast, businesses that open multiple accounts under vague business names, change banks frequently, or misrepresent their activities inevitably find themselves blacklisted. Several operators have lost access to funds or even shut down entirely due to deceptive practices.

Modern Solutions for a Modern Industry

Fortunately, the cannabis banking landscape has evolved. Today, more credit unions and state-chartered banks are stepping forward with programs designed specifically for cannabis operators. These institutions typically charge higher fees to cover the added compliance workload, but they offer transparency and predictability in return.

Additionally, cannabis banking platforms now exist to connect businesses with financial institutions that understand the industry. Some of these platforms also include tools for compliance documentation and reporting. New payment technologies are also emerging that reduce the need for cash handling while still staying within banking regulations.

All of these options represent a shift away from outdated and dangerous practices— such as disguising cannabis income, running funds through unrelated businesses, or relying on holding companies to open accounts.

Yes, It’s More Expensive—But It’s Worth It

Cannabis businesses must accept that they will pay more for banking services. Monthly fees often range from a few hundred to several thousand dollars. These charges cover the cost of suspicious activity report (SAR) filings, KYC verification, and ongoing account monitoring required by federal law.

While expensive, these fees are far less costly than dealing with frozen assets, last minute bank changes, or operating entirely in cash. The predictability and legitimacy that come with compliant banking relationships more than justify the investment.

Understanding SARs and Staying Ahead

Every cannabis-related account triggers SAR filings. Banks file one of three types: a Marijuana Limited SAR for compliant businesses, a Marijuana Priority SAR if the institution suspects a violation of state law, and a Marijuana Termination SAR if the account is shut down for compliance reasons. Trying to avoid SAR filings by obscuring your business type is a red flag and virtually guarantees eventual termination. It’s better to work with institutions that understand these requirements and have built programs to manage them.

Partnering with the Right Providers

You don’t have to navigate all of this alone. Specialized platforms can help manage your documentation and connect you with cannabis-friendly banks. When choosing a provider, confirm they understand both banking and cannabis regulations, check their track record, and make sure they offer strong data protection protocols.

The Payoff: Long-Term Stability and Growth

The benefits of strong compliance go beyond simply keeping your account open. Banks often lower fees over time for trusted partners, and access to services like lending and merchant processing expands as your relationship matures. Businesses with stable banking relationships are better positioned to grow, raise capital, and scale without constant operational disruptions.

Final Thoughts

As a cannabis industry veteran, you already understand regulation. But banking requires a deeper level of documentation, consistency, and strategic communication. Avoid shortcuts. Invest in compliance. Be transparent with your financial partners. While the process may be more rigorous than what other industries face, it’s navigable—and increasingly essential for sustainable growth.

In today’s environment, legitimate banking relationships aren’t just possible—they’re a competitive advantage.

Committee Blog: Banking in the Cannabis World

By: Shawn Kruger, Avivatech

Contributing Authors: Paul Dunford, Green Check Verified | Todd Glider, MobiusPay Inc. | Kameron Richards, Kameron Richards Esq.

Produced by: NCIA’s Banking & Financial Services Committee

The Landscape

With recreational marijuana legalized in 23 states, Washington D.C. and Guam, the public continues to broadly favor legalization for medical and recreational purposes. Why then, is it still a challenge for the cannabis industry to access financial services? The short answer: cannabis banking is risky for financial institutions (FIs), and bankers are committed to avoiding unnecessary risk. Historically, FIs have worked to keep funds associated with illegal activity out of their banks and credit unions, so FIs are sensitive to conflicting state and federal cannabis laws. For example, many FIs are regulated by federal agencies, but marijuana is a Schedule I controlled substance.

Navigating the Challenges

However, there are many banks and credit unions that have taken this risk for a variety of reasons, including creating new sources of income, a desire to serve the unbanked in their communities, and supporting the social equity initiatives in the cannabis industry. These FIs are usually discreet about their cannabis banking programs, and it’s often hard to identify them through your typical approach: prowling websites, Google searches or even trade shows (although this has improved over the past 12 to 18 months).

Fortunately, the best approach is also a well-trusted option: word of mouth. Contact lawyers, accountants and bookkeepers in your area. If they represent or work with other local marijuana related businesses (MRBs), they may know who they are banking with or know someone who does. You should also consider contacting the FIs directly, even if you don’t know if they are working with MRBs. You might be surprised to find that they do, and if they don’t, they might redirect you to another FI in the area. Finally, organizations like the PBC Conference team, provide resources to aid your search, including a Cannabis Banking Directory published annually.

Focus your search on credit unions, community banks, and regional banks. We are entering a new phase of cannabis banking with some FIs offering more than just a place to park your cash. A growing number now offer loans, payroll services, business insurance, etc., so take time to see what’s available, compare multiple FIs’ programs, and find the best match for your cannabis-related business’ (CRB) needs.

Be Prepared

Every action taken by an FI, regardless of their location or asset size, is closely scrutinized by state and federal banking regulators, and law enforcement agencies. They want to make sure that banks and credit unions are only working with legitimate and legal state CRBs. Therefore, you can expect an FI to require a combination of the following:

- Driver’s license or other acceptable state-issued identification for all account holders

- Information on all beneficial owners of the company, not just those who own a percentage of the company above a certain percentage threshold (such as 20%)

- Tax returns for the previous year for both the company and the beneficial owners

- Financial information such as profit and loss accounts and capitalization tables

- A copy of any required state licenses

- Operational data such as projected annual sales and number of patients/customers

- Corporate formation documents such as articles of incorporation and business plans

- Sales transaction data (store reports or invoices) for the past thirty days

Behind the scenes of cannabis banking, FIs must do a lot to ensure that they are onboarding only legitimate CRBs; from collecting and analyzing market transactions to conducting reporting. This means that FIs often have additional staff to fulfill their compliance duties and they invest in software to automate some of their monitoring. FIs invest heavily in banking cannabis and account fees help offset those expenses. This means you can expect to pay account setup fees and monthly account maintenance fees to help cover these costs. Prices have come down in recent years. The days of paying $5,000 per month for an easy deposit account are long gone, but the fees will remain high as long as a lot of oversight and reporting falls on FIs.

Embrace the Journey

FIs are far savvier about detecting MRB activity among their existing customer/member accounts. At this point, it’s not a question of “if” your FI will find out you’re an MRB, but when. Few things are more disruptive to a business than getting a letter from your FI informing you that your account will be closed in thirty days. Don’t put yourself in that position. Additionally, you may be missing out on vital financial and business services by staying “under the radar” and not having a transparent relationship with a bank or credit union. Start looking for a cannabis-friendly bank or credit union today!

Committee Blog: Defining Legal Hemp – It Isn’t Always Simple Math

By: Todd Glider, Chief Business Development Officer, MobiusPay Inc.

Contributing Authors: Paul Dunford, Green Check Verified | Shawn Kruger, Avivatech | Kameron Richards, Kameron Richards Esq.

Produced by: NCIA’s Banking & Financial Services Committee

If you are a cannabis-related business, and are looking to accept credit cards, it is only possible to do so if you are selling a product that is defined as legal hemp by the 2018 Farm Bill.

The 2018 Farm Bill provides that:

“The term ‘hemp’ means the plant Cannabis sativa L. and any part of that plant, including the seeds thereof and all derivatives, extracts, cannabinoids, isomers, acids, salts, and salts of isomers, whether growing or not, with a delta-9 tetrahydrocannabinol concentration of not more than 0.3 percent on a dry weight basis.”

For the most part, it’s pretty cut-and-dry. Marijuana is a schedule 1 drug. Hemp is not. If your product has less than .3% Delta-9 on a dry weight basis, it’s not marijuana, it’s hemp. And since it’s hemp, it’s federally legal. And since it’s federally legal, it can be purchased with checks, credit cards, or debit cards. Hemp products are, reductively, as incendiary as a stick of butter.

Of course, there is the law and there is how acquiring banks—banks that offer merchant accounts—interpret the law. Across the U.S., there are hundreds of acquiring banks. Of those, only six or seven offer merchant accounts to hemp businesses.

That’s it, plus payment service provider Square.

The immediate problem for the few acquiring banks that have, laudably, said, “Yes,” to hemp is, “how do we distinguish products that are .3% Delta-9 or less (and therefore, yawningly legal) from those that are over .3% Delta-9 (and therefore, illegal as angel dust)?”

Enter the Certificate of Analysis, or COA, or lab report. While there is nothing in the law stating that COAs are required to prove that a product is within the federally legal limit, their role is sacrosanct during the boarding process. For every hemp-derived product, there must be a corresponding COA proving that the product being sold is hemp, and not marijuana.

Fortunately, there are labs across the nation. The U.S. Department of Agriculture website lists 85, as of May 2023. Manufacturers and businesses ship their samples to these labs. The labs run their tests and the COAs are issued.

Simple, right?

Not really.

There are no standards in place for these reports. No templates. Every laboratory’s COAs—while substantively providing the same information—look a little different. Furthermore, most bankers haven’t seen a lab report since high school chemistry, and you’ve got a recipe for confusion or misunderstanding (frequently both).

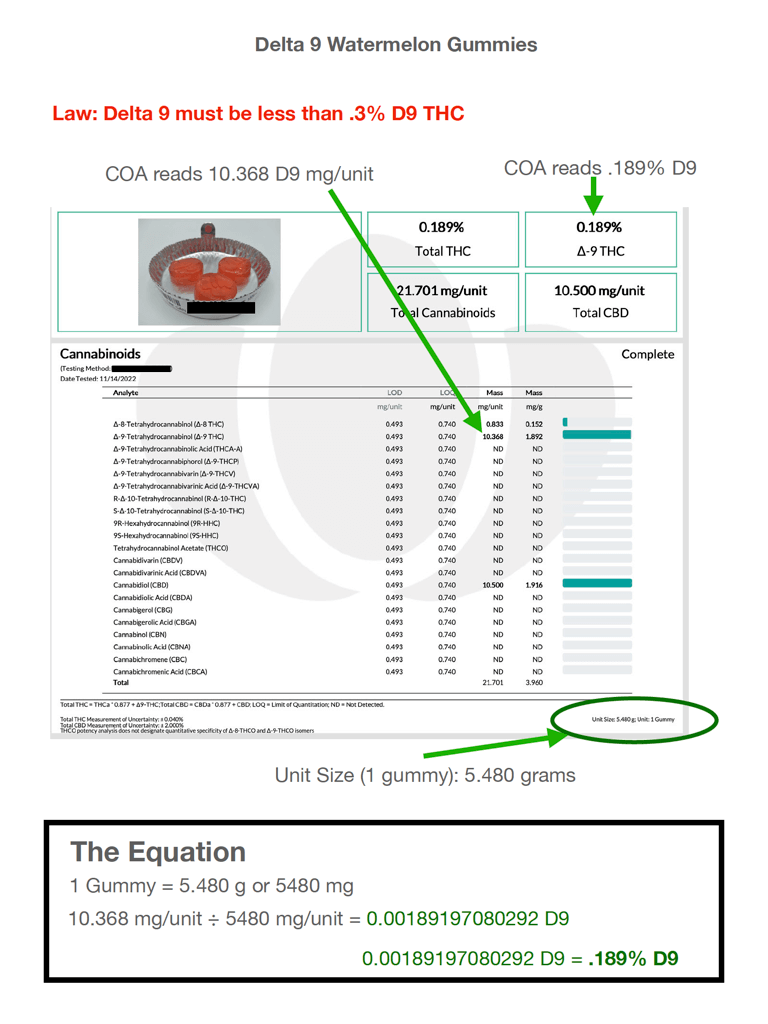

This COA, when it was initially presented to the bank, was rejected. To the underwriter, it was an open and shut case.

When the bank opened its door to offering acquiring to hemp businesses, its policy was to reject anything with greater than .3% Delta-9 by weight.

The top of this COA showed an instance of Delta 9 that read .189%. That passed muster, certainly. However, when he delved further into the analyte detail, he noted additional Delta-9 figures in excess of the .3% limit:

- 10.368 in the mg/unit cell

- 1.892 in the mg/g cell

It was not clear to the bank’s underwriter which of the two—per-unit or per-gram—corresponded with the by-weight percentage he was to be mindful of, but both were certainly over the .3% limit.

So, open and shut case: DECLINED

The salesperson that brought the merchant to this bank was surprised by the rejection. He hadn’t looked at the COAs very closely, but it seemed unlikely that this merchant had been selling products on her website that were in excess of .3% Delta-9.

Why? Because if the merchant had been selling products on its website in excess of .3% Delta-9, it would have been engaging in egregious felony drug trafficking. The salesperson doubted that was the case.

The salesperson did something he didn’t normally do: he took out his calculator.

He wanted to know why it read .189% Delta 9 at the top, but 10.368 in the analyte table. He noted the unit size at the bottom of the page was a gummy weighing 5.480g.

For the sake of simplicity, he multiplied that by 1000 to convert it to milligrams. That made it 5480 mg

Then he entered the onerous 10.368mg from the mg/unit figure in the analyte table and divided it by 5480mg. The resulting calculation netted the following total: .0018919.

Next, he converted it to a percent, and found that the result was .189%, which matched the figure at the top of the COA, exactly.

The next day, the salesperson presented the COA to the bank, with the markings and The Equation just as shown here.

It was an open and shut case: ACCEPTED

This situation is an example of why banks and credit unions unknowingly reject compliant hemp businesses from merchant processing solutions. As stated, a simple mathematical calculation was the difference between being accepted or rejected for necessary merchant processing services. Without proper merchant servicing not only are cannabis businesses’ profitability affected because they can only take cash; cash is also not as traceable or auditable as electronic transactions.

In general, businesses providing services to the cannabis industry are often challenged with disentangling legal risks with the benefits of their necessary services providing more transparency. With enhanced knowledge of the cannabis industry and its parameters, the cannabis industry will recognize a greater participation by all businesses necessary for the life of the industry thereby enhancing cannabis businesses’ likelihood to succeed but also enhancing the legitimacy and regulation of the industry.

Committee Blog: Four Tips for Cannabis Businesses to Maintain Cannabis Friendly Financial Services

by Kameron Richards and Steven Schain

by Kameron Richards and Steven Schain

Members of NCIA’s Banking & Financial Services Committee

Obtaining legitimate, cannabis-friendly financial services is among the cannabis industry’s biggest hurdles. Obtaining financial services is challenging for dispensaries, marijuana grows, and testing labs but it could also be an obstacle for non-plant touching businesses or individuals engaged in the cannabis industry. Without cannabis-friendly financial services, individuals and businesses related to the cannabis industry are deprived of simple financial solutions, like checking accounts, resulting in large amounts of cash being held at company facilities or the operator’s residence, posing significant risks.

Because only a small amount of insured banks and credit unions offer cannabis businesses financial services, finding cannabis-friendly financial services offered by FDIC or NCUA/CUNA institutions is challenging, and following a certain approach may fortify the longevity of a relationship with a financial institution.

Know Your Company Information and Banking Needs

Thorough onboarding initiates the account opening process for cannabis companies seeking financial services. Cannabis-friendly financial institutions exercise enhanced due diligence at account opening for compliance purposes, which will be further discussed in this article.

Financial institutions may require information on state licensing, corporate structure, and governance documents. Institutions generally collect information regarding the company’s underlying products and whether those products or services violate The Controlled Substances Act (“CSA”). Information collected during the onboarding process often determines the institution’s fee, risk-based categorization, and willingness to provide financial services to a particular cannabis company.

During the onboarding process, cannabis companies should determine if the financial institution provides all services necessary for its specific operation. The services offered by cannabis-friendly financial institutions may vary based on its risk tolerance.

Know Compliance Requirements and Cannabis-Specific Programs

Financial institutions serving the cannabis industry must comply with The Bank Secrecy Act’s (“BSA”) requirements set forth in the Treasury Department’s Financial Crimes Enforcement Network’s (“FinCEN”) BSA Expectations Regarding Marijuana Banking (FIN-2014-G001) (“FinCEN Guidance”). To mitigate the possibility of money laundering, institutions assemble extensive risk-based BSA programs centered around assessing the risk of each cannabis account and detecting and reporting “Red Flags” set forth by FinCEN Guidance.

To understand the constraints under which financial institutions are forced to operate, cannabis companies should familiarize themselves with relevant cannabis industry regulatory guidance and, if possible, structure its operations to ease its financial institution’s compliance efforts. Further, cannabis companies should understand any contractual terms and operation of any specific cannabis programs required by its financial institution (e.g., participation in cannabis-specific programs to support loan approvals, liquidity management or the coordination of cash courier services).

Know the Risk-Based Approach

FinCEN Guidance requires institutions to perform enhanced due diligence on cannabis companies, because the risk category of each cannabis account is determined during the onboarding process, institutions are required to obtain corporate and state licensing documentation and detect any negative news on the potential account signers and the business.

Because there is no mandated risk-based structure for institutions to follow, it is critical that cannabis companies know its institution’s specific risk-based structure. Further, if a cannabis company is utilizing more than one institution, it should understand that each institution’s risk-based categorization may have specific factors or considerations. Some institutions use a tiering structure (which can vary by institution) or make this determination based on the direct or indirect relationship that the account’s source of funds has with cannabis prohibited by the CSA. An institution’s risk-based categorization could determine an account holder’s compliance obligations or eligibility for financial services such as lending, treasury services, payment processing, and 401(k)/retirement solutions.

Know What Could Cause Account Termination

After completing the onboarding process and placing cannabis accounts in the requisite risk profile (which may vary among institutions), institutions are obligated to conduct ongoing enhanced due diligence on cannabis accounts in accordance with the risk each account poses.

This enhanced due diligence encompasses staying abreast of corporate changes, confirming that all licenses are up to date and conducting periodic negative news checks that indicate FinCEN Guidance “Red Flags.” It can also include a litany of happenings that cannabis account holders may not be aware of. While cannabis account signers may be compliant, without any negative news on them or their business, their institution could also close an account due to adverse information from tax and state licensing authorities or wrongdoing by employees or vendors. Cannabis account holders should also be aware of transactions prohibited by its institution’s policies and procedures like commingling funds between non-plant touching and plant touching accounts or transferring funds to and from vague accounts at unaware institutions unwilling to serve the cannabis industry.

Cannabis account holders with multiple relationships should be aware that each institution’s closure protocol may vary in response to adverse information or conducting transactions prohibited by internal policies and procedures (account termination terms are often contained in the depository agreement between the institution and cannabis account holder).

Conclusion

Beyond assisting a business’ core functioning, maintaining relationships with legitimate financial institutions leads to strategic advantages for a cannabis company and its owners and operators, like financing or payment processing.

Further, because FinCEN requires institutions to monitor and report cannabis account transactions and file a Suspicious Activity Report (SAR) when a cannabis account is opened or closed or if “Red Flags” are detected; cannabis companies can protect their accounts and businesses by knowing applicable laws and regulations and their institution’s cannabis-specific programs’ policies and procedures.