We are pleased to announce the release of the 2021 Cannabis Compensation Survey Report. This second annual survey aggregates compensation data for cannabis businesses and ancillary services, establishing benchmarks to help those businesses better understand the market and stay competitive, all while following federal compliance regulations that guide the collection and dissemination of compensation survey data and results.

FutureSense and NCIA laid the foundation for the project in 2019 and released results for the inaugural survey at the end of that year. At the onset of the pandemic in early 2020, both parties took a step back to adjust their trajectories looking to enhance the scope and depth of the project. Marijuana Business Daily came on as a primary partner to assist with visibility and distribution. Green Leaf Payroll & Business Solutions came on as a supporting partner, providing the project with anonymized payroll data. NCIA has stayed on as an endorsing partner to promote the shared mutual interest of supporting cannabis businesses and the industry at large.

This year, the survey established benchmarks with reportable data for 98 unique positions, a jump up from the inaugural report, which included 78 positions. The benchmarking process also established more accurate job titles representing both specific job responsibilities as well as representing the scope and breadth of organizational structures within the cannabis industry. These benchmarks include close to 200 unique positions total that will be reported on as the project grows and more cannabis organizations participate and submit data in future years.

The final report also includes recent trends and observations connecting the data to anecdotal insights found through our work and involvement in the cannabis community. The final report also provides information about how to utilize the survey data and a “geo-differential” chart to inform making any adjustments by state. The results are presented as percentiles to show both central tendency and spread. They are meant to be used as ‘guideposts’ to help inform salary and wage decisions, rather than exact numbers to base those decisions on. Many factors can and should be taken into consideration when determining what and how to pay employees, but these results provide an accurate representation of what pay amounts can be.

As the survey evolves and more companies participate, the project plans to also produce results with demographic breakouts such as by region/location, industry sector, and company size; as well as data for benefits, incentives, and equity compensation. These are all very valuable insights but require more participation across the country to produce, per compliance regulations.

The results from the survey can be used across every facet of the cannabis business. Understanding not just how to pay your employees, but also how to attract, motivate, engage, and retain your employees through compensation can be make-or-break in this rapidly evolving industry. 60-70% of companies’ expenses are typically payroll; being even 5% on- or off-the-mark could mean thousands or hundreds of thousands of dollars lost or gained.

The survey’s success is contingent on participation. More and more companies are realizing the value of this information and the importance of transparency through 3rd party surveys. All submissions and their respective data are held in strict confidentiality. Abiding by the Department of Justice regulations, this survey produces anonymous and unbiased results.

The survey accepts organization-wide submissions for companies with ten or more employees at this time. Individual submissions are appreciated as anecdotal insights, but are typically not included in data calculation.

For any questions and/or to sign up for next years’ survey, please email matt@futuresense.com or visit: www.BlueFireCannabis.com

Matt Finkelstein is a consultant with BlueFire Cannabis by FutureSense. He has worked in the management consulting world since 2007 while also pursuing a passion for and career in organic farming. His farming experiences span across the many facets of the cannabis industry, lending itself to unique perspectives supporting his current work bringing FutureSense’s services to the cannabis industry and its community.

BlueFire Cannabis is the cannabis-forward division of FutureSense LLC, a management consulting firm providing holistic people strategies that improve business performance. Our specialties include business strategy, motivation and rewards, executive, employee and sales compensation, organizational and individual assessment, leadership development and coaching, human resources, communications, change and sustainable transformation. For more information, please visit www.BlueFireCannabis.com and www.FutureSense.com

Committee Blog: Four Elements of Compensation Strategy in High-Growth (Cannabis) Companies

by Fred Whittlesey, Founder and President, Cannabis Compensation Consultants Member, NCIA Human Resources Committee

with assistance from

Kara Bradford, Co-Founder & CEO, Viridian Staffing Chair Emeritus, NCIA Human Resources Committee

All high growth companies face the same challenge: Hiring high-quality people at a feverish pace, while dealing with all of the issues that come with that including recruiting, onboarding, training, and of course, compensation.

The cannabis sector (more than just an “industry”) has another layer of challenges rarely seen when finding and hiring the employees needed for the explosive growth underway:

Diverse segments (to use a financial reporting term) often under a common entity, or

Multiple entities housing those distinct businesses, and

Diverse occupational categories either within a common entity or spread across multiple entities.

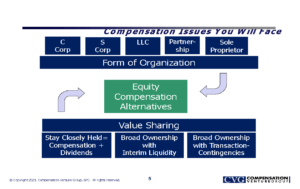

The cannabis product lifecycle, like any consumable product, spans agriculture, processing, packaging, branding, distribution, and direct sales. A fully vertically-integrated company might employ, within a single corporate entity, agricultural workers, lab workers and extraction specialists, manufacturing workers, distribution teams, and dispensary employees. That is a challenging environment for compensation plan design.

For example, agricultural workers, including agricultural managers, virtually never receive equity compensation as an element of their pay package. Biochemists, particularly when coming from a biopharma company, expect significant equity compensation. Retail dispensary managers, no equity. VP of sales, equity.

Now, imagine those jobs and people are spread across multiple entities. Maybe the overall corporate structure is a C Corp over some LLCs. Or, like in Arizona, a nonprofit corporation with a Management Services Agreement with a C Corp which directs money through an LLC.

Or in British Columbia which, like the U.S., prohibits alcohol and cannabis sales in the same stores or from the same company, but has owners that operate in both businesses. And the stores are next door to each other. Budtender vs. sommelier? Employees talk.

But perhaps the most compelling reason to consider a broad spectrum of compensation alternatives is unique to cannabis: The non-deductibility of compensation expenses that cannot be characterized as cost of goods sold — Tax Code Section 280E. More than in any other industry, using forms of compensation that avoid incurring a nondeductible compensation expense can have a direct and immediate impact on business financial performance.

Compensation Strategy

Complex cannabis companies have to mold their pay programs to fit this broad array of entities, lines of business, and types of jobs, under an unfavorable tax environment.

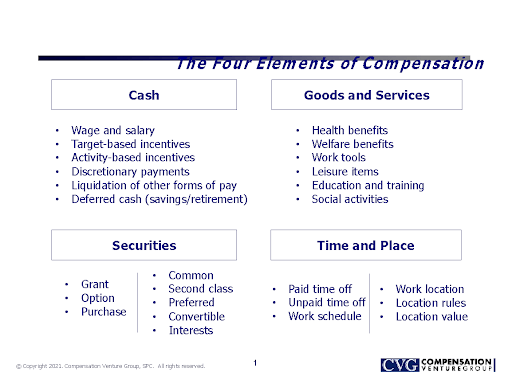

There are four, and really only four, types of compensation for employees (and independent contractors, and members of the Board of Directors, and consultants). Each of the four has many forms, but there are four types of things a company can do to pay — and hopefully continue to pay — an employee. This is a useful framework for thinking about compensation.

Cash

Wage, salary, performance incentives or bonuses, commission, 401(k) contribution (yes, a cannabis company can have a 401(k)), profit sharing, retention bonuses. Every employee will receive one or more of these forms cash payments. All require cash changing hands from the company to or on behalf of the employee.

The most common cash compensation arrangement is a base salary plus bonus as a percentage of salary that is typically dependent upon the performance of the individual, team, and/or company. Many companies have a 10% of base salary target. In the cases of budtenders and delivery drivers, tips (essentially a customer-paid commission) are common as compensation as well. Companies in some locations, such as California, continue to pay trimmers at piece rates (pay by unit production).

Goods and Services

I casually call this category “stuff” — a company gives people stuff as part of their compensation. Healthcare coverage, life insurance, job training, a laptop and a phone in the traditional model. But this category includes much more than traditional “employee benefits” — from free food to use of the company vacation home to sabbaticals, these meet employees’ needs while keeping them focused on, and sometimes physically at, work. Sometimes this free stuff is not taxable income to the employee (healthcare coverage, free food at work) and sometimes it is taxable (free gym membership). Be informed in your creativity here. Local regulations in many jurisdictions are dictating benefits coverage above the federally-mandated level.

Securities

This is by far the most complex form of compensation, and more so for cannabis companies. Whether it’s stock options, restricted stock, restricted stock units, or member interests (in an LLC) — the question is which entity is granting the compensation, and whether they are allowed to grant it to an employee in a different entity. We are beginning to see companies that compensate employees with cryptocurrency which is viewed as a “security” by both the IRS and SEC. Given the increasing social justice emphasis in the cannabis sector, equity compensation is the form of pay that truly levels the playing field across all income levels.

The choice of equity compensation will be driven by the form of organization and ownership philosophy.

Time and Place

Before COVID-19, companies in all industries were increasingly emphasizing this form of compensation. In the 1980’s, there was no “casual dress” and “working from home” was unheard of. An employee reported to the workplace at the assigned time, and there was no “flextime.” Over the past few years, companies were already experimenting with paid parental leave, unlimited vacation time, and employee-choice work location. Now, for many companies and many jobs, WFH is the model. Not for growers and not for budtenders (yet). But time and place can be highly valuable cash-free (sort of) equity-free forms of compensation.

And then…

Hiring is only half the battle. Retention of employees in the cannabis sector is as challenging as hiring. Companies need to be creative with the same four tools to retain employees. But you can’t wait until they give notice of resignation, because then it’s too late.

Your employee retention compensation program starts at the employee’s date of hire, because it is the same program.

Video: NCIA Today – The MORE Act, 2020 Election, Board of Directors, and More!

Tune in to this month’s episode of NCIA Today with Deputy Director of Communications, Bethany Moore.

This month, we’re sharing even more important news about The MORE Act, an analysis of the results of the 2020 election, plus our own Board of Directors election results, and a new policy report from NCIA’s Policy Council. We review some clips from the educational panels from our very first CYBER edition of our Cannabis Business Summit & Expo.

We’re doing a great job staying home, wearing masks, and socially-distancing through these difficult times. We can’t wait to get back to hosting our national and regional events in person later in 2021. In the meantime, make sure you’re subscribed to our email list, and listening to NCIA’s weekly podcasts hosted by myself and Tahir Johnson. And now is a great time to invest in the future of our industry by getting more involved in NCIA, registering for our educational webinars, and learning more about the Diversity, Equity, and Inclusion Program SPONSORSHIP opportunities! Join NCIA members who have stepped up their support by becoming DEI Program Sponsors like 4Front Ventures and Greenbridge Corporate Counsel.

We Must Hold Ourselves Accountable To Create A Fair Cannabis Industry

by Aaron Smith, NCIA’s CEO and Co-founder

As the nation began grappling with issues of systemic racism and inequality on a massive scale following the death of George Floyd and ensuing civil rights protests across the country, we saw an outpouring of support from members of the cannabis community. It was inspiring to see so many people standing up for justice and recognizing the disproportionate impact that prohibition has had on marginalized communities and Black people in particular.

Words, however, are not enough. Implicit in supporting positive change is the need to reflect on where we can do better – and be better – ourselves, and then taking action.

Since our initial public statement on this national reckoning early this summer, NCIA has started taking the first in what will be an ongoing series of steps to facilitate more diverse representation, participation, and access to opportunities in our industry. We instituted aSocial Equity Scholarship Program to provide complimentary first-year membership and other benefits to licensees and applicants in state and local social equity programs and recently launched the#CatalystConversations webinar series to provide them with valuable information and amplify their voices. We have created a staff position to directly engage staff, membership, and allies to critically analyze and expand upon our progress. And, we are currently establishing an Opportunity Fund to help support and expand our scholarship program, and assist disenfranchised members and the organizations fighting for them. But we still have a long way to go.

As part of our efforts, we are also encouraging cannabis and ancillary businesses to commit to improving diversity, equity, and inclusion in the industry and to hold themselves to those commitments by participating in The Accountability List byCannaclusive.

The Accountability Listgives businesses and organizations the opportunity to show consumers, the industry, and policymakers what they are actively doing to promote fairness and inclusivity in cannabis and beyond. We encourage everyone in the cannabis space to stand up for justice, be honest about where they can improve, and commit to doing so in the most forthright, measurable, and transparent ways possible.

Photo By CannabisCamera.com

Ending cannabis prohibition and improving diversity in the industry is not going to eliminate systemic racism or fully repair all the death and destruction committed in the name of the war on drugs, but together we can make a real difference and help create a better future.

NCIA, our Board of Directors, and I stand firmly in support of people fighting to end racial injustice and ensure a fair cannabis industry with equitable opportunities for all. We hope you’ll stand with us.

Video: NCIA Today – August Recap, Diversity, Equity, & Inclusion Update, Election Predictions, and more!

Host Bethany Moore, NCIA’s Communications Manager and host of NCIA’s weekly Podcast ‘NCIA’s Cannabis Industry Voice‘ brings you an in-depth look at what is happening across the country in federal cannabis policy reform and with NCIA.

From the top, Bethany discusses the new NCIA #IndustryEssentials webinar series. Webinars that arenʻt just about getting some big-name talking heads on a Zoom call, but about getting the correct people with the most up-to-date information to help our members stay ahead of the curve. This new series provides insights you canʻt find anywhere else, from experts who will surprise and delight you with their in-depth knowledge on relevant industry topics.

We check in with NCIA Diversity, Equity, Inclusion Manager Tahir Johnson to hear some of the recent highlights from his new show “The Cannabis Diversity Report.” Launched alongside the NCIA Social Equity Scholarship program, this weekly conversation takes an in-depth look at navigating, regulating, and growing the cannabis industry as a minority operator.

Director of Public Policy Andrew Kline joins Bethany on NCIA Today to discuss the nomination of Kamala Harris as the Democrats’ vice-presidential choice. A former Biden staffer and advisor, Kline discusses the minute differences he sees in the nominees’ cannabis policy and his expectation that Senator Harris can help Vice President Biden’s views evolve.

2020 isn’t completely canceled, as we begin registration for this November’s #CannaBizSummit CYBER, register today!

Member Blog: A Summary Of Colorado’s Publicly Licensed Marijuana Companies Bill (HB19-1090)

On May 29, 2019, Governor Jared Polis signed HB 1090 into law, removing burdensome restrictions on who can own cannabis businesses in Colorado and permitting greater outside investment. The law, which goes into effect on November 1, 2019, drastically changes the regulations in Colorado by permitting public companies, currently prohibited from owning cannabis licenses, to own such a license in the state. Additionally, shareholders with equity interests below ten percent will largely be able to avoid the current extensive disclosure requirements.

Before industry participants rush to secure outside investments, there are important issues to be considered.

First, the rules and regulations promulgated pursuant to HB 1090 have yet to be drafted. While the new ownership framework is outlined in HB 1090, the actual rules that will govern Colorado businesses must still be written. Second, the law does not take effect until November 1, 2019. Regulators have previously penalized companies for hastily signing, or announcing transactions before a law takes effect or without first speaking with the regulators. This type of hasty action can put companies at risk of sanctions and hinder the application process. Lastly, this article is only a summary of HB 1090 and does not discuss the nuances of the law. Please consult a licensed attorney regarding specifics of any proposed transactions.

The signing of HB 1090 opens a new era for the Colorado cannabis industry. Where the old law prohibited public corporations from owning even indirect equity stakes, the new law allows certain publicly traded companies to own licensed cannabis businesses within Colorado. And where the old law required at least one owner to meet the one-year residency requirement, the new law only requires all individuals with day-to-day operational control to be Colorado residents. The new law also allows non-U.S. citizens to own equity in a licensed business.

What’s New

Many of the old categories of ownership have been scrapped. No longer are there Direct and Indirect Beneficial Interest Owners or Qualified Passive Investors. Where HB 1040 (the previous law that currently governs ownership) focused on any amount of control or ownership, HB 1090 generally requires more direct control or ownership to trigger disclosures and Marijuana Enforcement Division (MED) approval. HB 1090 creates three new types of ownership classifications and defines “Acquire” and “Control” more effectively. Control is the direct or indirect possession of the power to direct the management or policies of the cannabis business, whether through ownership of voting securities, by contract, or otherwise. This is important because the control requirement now specifically addresses management agreements within the industry. A person “Acquires” a cannabis business not only through the acquisition of ownership interest, but also through the acquisition of direct or indirect control, voting power, or through the sole power to dispose of the owner’s interest through transactions, subsidiaries, purchases, assignments, transfers, exchanges, successions, or other means.

There are three new types of ownership classifications within HB 1090.

First, a Controlling Beneficial Owner, which refers to (i) a natural person, entity, or affiliate (a person that directly, or indirectly through one or more intermediaries, controls or is controlled by or is under common control with, the person specified) or a Qualified Private Fund, defined as a typical venture capital or private equity fund that, owns ten percent or more of a cannabis business, or a person who is otherwise in control of the cannabis business (including managers or others); or (ii) a Qualified Institutional Investor, which is defined as one of a list of entity types that largely reflect passive institutional investors, owning or acquiring at least thirty percent of the owners interest in the cannabis business.

Second, a Passive Beneficial Owner, which is any person holding any interest in a marijuana business who is not otherwise a Controlling Beneficial Owner or in control.

And, third, an Indirect Financial Interest Holder, which is a person that is not an affiliate, a Controlling Beneficial Owner or Passive Beneficial Owner, does not receive a percentage of the revenue or profits of the cannabis business as compensation and satisfies one of the following requirements: (a) holds a reasonable royalty in exchange for the cannabis business using its IP; (b) holds a permitted economic interest prior to January 1, 2020 in a cannabis business that has not been converted into an ownership interest; or (c) is a party to a contract with a cannabis business involving a direct nexus to cultivating, manufacturing, or the sale of cannabis. An Indirect Financial Interest Holder includes a person leasing equipment or real property for use in cannabis operations or cultivation; secured and unsecured financing agreements; security contracts; and management agreements.

Disclosure Requirements and Change of Ownership Process

Controlling Beneficial Owners and Passive Beneficial Owners each have their own separate disclosure requirements under the law. But with reasonable cause, the MED can require any person to report most of the same information as Controlling Beneficial Owners. All Controlling Beneficial Owners and, at the MED’s request and based on reasonable cause, any other person disclosed under the “business owner and financial interest disclosure requirements” provision must submit for a Suitability Judgment from the MED or apply for an exemption from such requirement prior to submitting a cannabis business application. “Reasonable cause” is defined as just or legitimate grounds (based in law and in fact) to believe that the requested action furthers the purpose of the law or protects public safety.

All Controlling Beneficial Owners must submit disclosure and fingerprint-based criminal history checks as required by the regulations. The MED will review the Controlling Beneficial Owner to see if it shows a history of good moral character. Currently, there is no test for what will justify denial based on the background check.

All applicants for the issuance of a state license must disclose a complete organizational chart reflecting the identity and ownership percentages of its Controlling Beneficial Owners. If the Controlling Beneficial Owner is a publicly traded company, the application must disclose the public companies’ managers and any beneficial owner that, directly or indirectly, owns at least ten percent of the Controlling Beneficial Owner. If the Controlling Beneficial Owner is a Qualified Private Fund, then an organizational chart must be disclosed that identifies the ownership percentages of the Qualified Private Fund’s managers, investment advisors, and anyone else that would control the manager or operations of the marijuana business (this means that, barring extenuating circumstances, funds will not need to disclose their Limited Partners). All applicants (including individuals) must take reasonable care to confirm that its Controlling Beneficial Owners, Passive Beneficial Owners, Indirect Financial Interest Holders, and Qualified Institutional Investors are not prohibited under the law, and failure to do such due diligence can lead to penalties.

For individual applicants, the natural person’s identification must be disclosed for persons that are both Passive Beneficial Owners and Indirect Financial Interest Holders in the cannabis business, any Indirect Financial Interest Holder that holds two or more indirect financial interests in the business or for persons that contribute over fifty percent of the operating capital of the business.

Despite specific disclosure requirements listed in HB 1090, the MED has discretion to mandate additional reporting. The MED may require an applicant or business to disclose each owner and affiliate and, with reasonable cause, may require a list of each non-objecting beneficial interest owner; business or Controlling Beneficial Owner that is publicly traded; Passive Beneficial Owners of the business; for any Passive Beneficial Owner that is not a natural person, the board members, directors, general partners, executive officers, and ten percent or more owners of the Passive Beneficial Owner; and all Indirect Financial Interest Holders of the cannabis business (including non-natural persons that own at least ten percent of the Indirect Financial Interest Holder).

The disclosure requirements primarily focus on individuals with ten percent or more interest in a cannabis business and those persons in control, but HB 1090 does include a strict prohibition on structuring any transaction with the intent to evade disclosure, reporting, record-keeping or suitability requirements, and any such action can lead to denial or revocation of an application.

Conclusion

Regulations for changes of ownership are still not known and will be clarified during the rule-making process. For most transactions, it appears that a new Controlling Beneficial Owner will need to be approved prior to submitting an application change of ownership for approval. HB 1090 will generate exciting opportunities for Colorado, but it is important to know the law, be patient while the MED promulgates regulations, wait until November 1, 2019 before initiating any outside investment transactions, and consult a licensed attorney regarding specifics of any proposed transactions.

Charlie Alovisetti, Vicente Sederberg LLC

Charles Alovisetti is a partner and chair of the corporate practice group at Vicente Sederberg LLP based in Denver. He assists licensed and ancillary cannabis businesses with corporate legal matters, and he has experience working with clients on a broad range of transactions.

Committee Blog: Transacting in Equity – The Basics

by Charlie Christopher, VP, Finance, Cirrata NCIA’s Finance and Insurance Committee

“A prudent man must seek to satisfy himself about the means to an end. This demands that he must revisit, again and again, the very elemental principles of his craft independent of how others think and act.” – Tony Deden

In businesses of all sizes it is common to transact in a number of currencies other than cash. The focus of this piece is on transactions involving common equity, the most fundamental unit of business ownership. The first section establishes a framework for how to view equity as currency, and what differentiates equity from other mediums of exchange such as cash. The second section introduces the process for creating reasonable projections based on sound logic. The third section demonstrates a somewhat novel application of concepts, and provides an example of the flexibility that can be introduced into the process. The conclusion is a reminder that these concepts can easily be misused, and that nothing should replace common sense when dealing with extreme uncertainty.

The Problem

Valuing any business is hard. Valuing a start-up is even harder still, not because of process, but because of the ambiguity associated with the output. When a valuation is based on multiple layers of high variance variables then the resulting distribution of value is rightfully broad. This poses a major challenge for operators and investors trying to agree on fair terms, and it can lead to irreparable damage to a young company.

Imagine for a second that you, and everyone else, have a crystal ball that can see the future with just enough variance to keep things interesting. How would that change the way you think about your equity? Would you be offering the same equity deals to your entire team? Would you be flexible with investors interested in your business? Of course not, you would look into the future every morning, update your projections and you would transact in equity in a similar manner to how you would with cash. Even though we do not have a crystal ball in the real world, it stands that to transact in equity with absolutely no opinion of value is the equivalent to being indifferent between paying $.10 or $100,000 for the same product or service.

Equity is a form of currency. It has value. However, its value has a built-in variance that rewards beating expectations, and punishes missing expectations. This is why equity awards are typically used to incentivize contributions that can increase the odds of achieving the former. The act of issuing the reward, in theory, immediately increases the value of the firm through the alignment of incentives. The common exaltation of the aforementioned qualitative attributes of the incentive over the quantitative attributes is also why the standard practice of ignoring a non-cash expense like share-based compensation is so indefensible. The value creation may be real, but to deny that a currency has transacted to create that value is to double count the benefit to shareholders.

The Process

Valuing a business begins from the top down and ends from the bottom up. Top down refers to projections based on the broader market while bottom up refers to firm specific capabilities extrapolated into the broader market. A common mistake operators make is to build up based on capabilities with no regard for how the aggregate ecosystem will react to the sum of all fundamental behaviors in the ecosystem. Starting from the top-down with a defensible position regarding both the size of the addressable market and the number of competitors participating in the market provides parameters for the business’s potential revenue.

Arguing for market share using a top-down analysis is fundamentally flawed if it does not reflect the true capacity of the business. A bottom-up analysis reflecting firm-specific capabilities should be compared to the top-down analysis for reasonableness. Ultimately, bottom-up analysis drives operating assumptions, and operating assumptions are the inputs to nearly every valuation technique.

I subscribe to the theory that posits that the variance in all of the assumptions can be quantified using an appropriate discount rate. In other words, if I’m uncertain and find my forecasted outcome to be highly unreliable I may choose to use a much higher discount rate to calculate the present value of the business than for a business with lower variance assumptions. When valuing a start-up company, I consider the corresponding ultra-high discount rate to cloud too much insight. For start-ups I first calculate a probability of firm failure in each of the forecast years and multiply my operating assumptions by the cumulative probability of success, I then use a more reasonable discount rate as if the firm was not highly speculative. This allows start-ups in the seed stage to more easily defend increases in value before launch. For example, the filling of a major executive leadership position justifies a small reduction in the probability of failure. Thus, your first executive hire has a reason to have received a higher percentage equity award than your last hire, even though the dollar value of the award might be equal. The process facilitates fair negotiations among all shareholders who may commit under vastly different circumstances and with different information. All too often this doesn’t take place, and the animosity that can develop as a result is as real as it is avoidable.

Valuation is admittedly more art than science. Many astute readers will point out that markets don’t operate in the orderly, fundamental matter I’ve proposed. Those critics are absolutely correct. It is a fair caution that not only are the trappings of certainty intoxicating, but sometimes simply observing how others are transacting is sufficient to make decisions. The market is often wrong, but it’s also often right. Remember to update your assumptions as new information becomes available.

Charlie is a Co-Founder of Cirrata where he lends his extensive knowledge from being both an entrepreneur as well as a securities analyst. As VP of Finance, Charlie combines his skills to assist clients through the application process, ongoing operations, and exit strategies.

Prior to joining Cirrata, Charlie co-founded a luxury women’s ready-to-wear label where he oversaw two separate rounds of funding as CFO. He has consulted numerous clients in the cannabis, construction, music, financial services and software industries in which his primary focus was on information systems, optimization, cash forecasting, securities offerings, licensing and capital allocation.

Raising Money 101: Accredited Investors and Fundraising in the Cannabis Industry

*Updated to reflect new Rule 147A and Amendments to Rule 147

When raising capital from outside investors, companies are faced with several choices regarding terms, structure, filings to make or not make, and type of investor, among other decisions. One choice – whether or not to include unaccredited investors – should be easy to make. For the reasons outlined below, it is strongly advised that only accredited investors be allowed to participate in a fundraising process.

What is an accredited investor? An accredited investor can be an individual or an entity. An individual can be considered accredited if he or she meets one of the following criteria:

net worth of at least $1,000,000 dollars (excluding the value of his or her primary residence); or

income at least $200,000 each year for the last two years (or $300,000 combined income if married) and have the expectation to make the same amount this year.

For entities, different criteria can apply depending on the form of the entity, but generally speaking, an entity will be considered accredited if all of its equity holders are accredited or it has greater than $5,000,000 in assets. Persons or entities that do not meet the above standards are referred to as unaccredited or non-accredited investors. While this is not an insignificant amount of money, the threshold is not very high. Especially if the person in question is considering investing a substantial amount of money in an uncertain venture that, even in the best of circumstances, may not make any money for years to come.

To understand why this definition is important, you must understand how sales of securities are regulated in the United States. At a high level, federal securities law requires that any sale of securities must either be registered with the Securities Enforcement Commission (SEC) or issued pursuant to an exemption. A full description of each exemption available to companies is beyond the scope of this article. But most private offerings of securities make use of the safe harbor exemption from registration known as Regulation D (in the parlance of our times, Reg D). There are three exemptions under Reg D (note the descriptions below only address the accreditation and disclosure issues discussed in this article and ignore issues related to general solicitation and restricted securities):

Rule 504: Allows for an exemption for the offer and sale of up to $5,000,000 of securities in a single twelve-month period.* Unlike some other exemptions, this exemption allows for a private sale without any specific disclosure requirements (note that the anti-fraud provisions of the federal securities laws still apply). Sales can generally be made to an unlimited number of accredited or unaccredited investors.

*Prior to adoption of new rules on October 26, 2016, the aggregate amount of securities that could be sold pursuant to Rule 504 was $1,000,000. The new rules also eliminated Rule 505.

Rule 506(b) and (c): Has the same criteria and guidelines as Rule 505, with one additional requirement – in the case of a 506(b) offering, all non-accredited investors must be sophisticated (i.e., “must have sufficient knowledge and experience in financial and business matters to make them capable of evaluating the merits and risks of the prospective investment”). This is an amorphous standard and creates yet another potential issue for the company offering securities. While beyond the scope of this article, it is worth mentioning that a Rule 506(c) offering, which permits general solicitation and advertising (normally not allowed under a 506(b) offering), cannot include any non-accredited investors.

The most important takeaway from the descriptions of the exemptions above: if you wish to undergo an offering without limitations on the number of investors, size of amount raised, or without specific disclosure requirements, you must sell only to accredited investors. Any offering which includes unaccredited investors, whether done under 504 or 506, will impose at least one of these restrictions on the offering.

Beyond the above-mentioned restrictions, there are other reasons not to include unaccredited investors in an offering. For one, it is not unusual to give investors the right to invest in future financing rounds – often referred to as a preemptive right. This is fine, provided no investors are unaccredited, but would be an issue for a company that has existing unaccredited investors with the right to invest in future rounds. Suddenly, a future financing round may inadvertently involve unaccredited investors and this may require a company to spend time and money developing fulsome disclosure documents or risk violating securities law. Another concern, while not immediate, is that if the company wants to go public, the SEC may evaluate all prior issuances of stock by the company and require that it take remedial actions to cure any past violations of securities laws, which might delay or imperil the IPO.

While any emerging company would be wise to restrict its offering to accredited investors, cannabis companies should be especially vigilant. Securities regulators, both on a federal and on a state level, made it clear that they consider the cannabis industry to be an area of special concern. Not because of the ongoing federal illegality of cannabis, but because of the increased risk of fraud in such a new and dynamic industry. The last thing any cannabis company should want to do is take any action that could expose them to the ire of regulators.

What if your investors are Canadian? After all, almost $500,000,000 Canadian dollars were raised last year in the Canadian public markets, and many Canadian investors are eagerly eyeing U.S.-based assets. Setting aside any Canadian securities laws issues, which are beyond the scope of this article, a Canadian or Canadian entity can certainly qualify as an accredited investor and allow an issuer to rely on Reg D. But be sure to have any Canadian investors carefully review their accredited investor questionnaire (a document issuers should require investors to fill out certifying what criteria marks them as accredited) they provide in connection with the offering – while Canadians are familiar with their version of accreditation, the qualifications differ just enough from US qualifications to be a potential issue. Note that there can be additional complications involved with accepting foreign investment, both for the investors and the company raising capital beyond those related to securities law.

It is also worth mentioning that the underlying policy arguments for restricting offerings (in the absence of fulsome disclosures) to accredited investors become even stronger in the cannabis industry. The risk of failure, and the total loss of investment, is undoubtedly present in an industry and remains federally illegal and operates based on federal guidance that could be changed at any moment. And investing in a cannabis company requires an even higher level of sophistication than a typical deal because of the challenges involved. A company should not accept money from investors who cannot handle the risk of losing their entire investment – not only is this unfair to the prospective investor, but any burned investors who end up in a financially precarious situation increase the risk of damaging litigation. While it may be tempting to accept funds from non-accredited investors, all the above issues can be readily avoided if non-accredited investors are not permitted to participate in a company’s offering.

This information is educational only and shall not be construed as legal advice. Please consult your attorney prior to relying on any information in this article.

Charles Alovisetti is a senior associate and co-chair of the corporate department at Vicente Sederberg LLC. Prior to joining Vicente Sederberg, Mr. Alovisetti worked as an associate in the New York offices of Latham & Watkins and Goodwin where his practice focused on representing private equity sponsors and their portfolio companies, as well as public companies, in a range of corporate transactions, including mergers, stock and asset acquisitions and divestitures, growth equity investments, venture capital investments, and debt financings. In addition, Mr. Alovisetti has experience counseling portfolio and emerging growth companies with respect to general corporate and commercial matters and all aspects of compensation arrangements, including executive employment and consulting agreements, stock option plans, restricted stock plans, bonus plans, and other management incentive arrangements. Mr. Alovisetti has experience in both U.S. and cross-border transactions, and advised clients across a range of industries prior to focusing on the cannabis space. He holds a Bachelor of Arts, with honors, from McGill University and a law degree from Columbia Law School, where he was a Harlan Fiske Stone Scholar. Mr. Alovisetti is admitted to practice in both Colorado and New York and is a Level One Interpener. He can be reached at charlie@vicentesederberg.com. Follow him on Twitter @CAlovisetti.

Michael Heyward is a law student at the University of Denver Sturm College of Law and a law clerk at Vicente Sederberg LLC. He holds a Bachelor of Arts in History and Political Science, and a Master’s Degree in History from Florida Agricultural and Mechanical University.

Matt Finkelstein is a consultant with BlueFire Cannabis by FutureSense. He has worked in the management consulting world since 2007 while also pursuing a passion for and career in organic farming. His farming experiences span across the many facets of the cannabis industry, lending itself to unique perspectives supporting his current work bringing FutureSense’s services to the cannabis industry and its community.

Matt Finkelstein is a consultant with BlueFire Cannabis by FutureSense. He has worked in the management consulting world since 2007 while also pursuing a passion for and career in organic farming. His farming experiences span across the many facets of the cannabis industry, lending itself to unique perspectives supporting his current work bringing FutureSense’s services to the cannabis industry and its community.

by Fred Whittlesey, Founder and President, Cannabis Compensation Consultants

by Fred Whittlesey, Founder and President, Cannabis Compensation Consultants

On May 29, 2019, Governor Jared Polis signed

On May 29, 2019, Governor Jared Polis signed

Follow NCIA

Newsletter

Facebook

Twitter

LinkedIn

Instagram

News & Resource Topics

–

This Just In

Member Blog: What Consumers Really Want in a Pre-Roll

Member Blog: The Evolving Cannabis Legal & Regulatory Landscape in 2026