Service Solutions | 10.26.22 | Show Me the Money – The Current State of Cannabis Lending

NCIA’s Service Solutions series is our sponsored content webinar program which allows business owners the opportunity to learn more about premier products, services and industry solutions directly from our network of established suppliers, providers and thought leaders.

In this edition originally aired on Wednesday, October 26, 2022 we were joined by the experts from cannabis-focused financial institutions FundCanna, Safe Harbor Financial, and AVANA Companies to dive deep into the current state of cannabis lending with leading industry journalist John Schroyer of Green Market Report.

A decade after California and Colorado became the first adult use states, the regulated U.S. cannabis market encompasses over 70,000 cannabis-related businesses. Shockingly, most of those businesses still lack easy access to debt and other forms of growth and operating capital. From federal prohibitions and the impact of IRS regulation 280e, to state and local taxation issues, the costs of operating a regulated cannabis company continue to remain nearly unendurable.

Learn what may change in the coming six to 12 months so you’ll know how to access debt capital most cost-effectively in this ever evolving environment. No matter your place in the industry or the supply chain from cultivators, manufacturers, vendors, suppliers, distributors and retailers this conversation will provide the insights to meet your financial needs.

At the conclusion of the discussion our panel hosted a moderated Q&A session to provide NCIA members an opportunity to interact with leading minds from the financial services space, join today to contribute to future conversations!

Panelists:

Adam Stettner

Founder & CEO

FundCanna

Sundie Seefried

Founder and CEO

Safe Harbor Financial

02:13 – Equity vs. Debt: With equity dried up, should cannabis companies be looking at debt financing to grow now?

07:28 – Equity vs. Debt: What do borrowers need to do before approaching a debt provider (vs. an equity provider)?

13:25 – Equity vs. Debt: What can cannabis companies or entrepreneurs do to improve their overall credit worthiness prior to seeking capital?

17:16 – How has the interest rate increases by the Federal Reserve impacted capital markets (and the industry at large) in 2022?

26:07 – Audience Q&A: “If there’s “no reason not to have banking” for your cannabis business how can I easily (and inexpensively) establish and maintain a compliant bank account?”

28:56 – Lending: What significant lending challenges are your clients currently facing within the industry?

33:56 – Lending: What advice can you provide business owners for evaluating lenders that you should (or shouldn’t) work with and tips for avoiding predatory lending practices?

39:05 – Cannabis Reform: What impact do you expect President Biden’s recent announcement will have on the industry?

49:32 – Audience Q&A: “Are your financial institutions planning to offer lending and banking services in New York, New Jersey and other new markets?”

51:42 – Audience Q&A: “With the mindset of “Investors are betting on the Jockey not the Horse.” What type of CEO or founding team would be a red flag or not a viable investment?”

55:19 – Audience Q&A: “How can I start to shift my retail company from being primarily a cash-only business?”

The state-by-state level of legalization and expansion of cannabis continues to pick up momentum across the United States, however, the adoption at Federal level is a much slower movement. The absence of federal legalization has created a situation where federally insured lending institutions like banks and traditional investment capital markets are prohibited from funding cannabis projects. The direct result of this restriction in capital has historically forced the cannabis industry to rely exclusively on private loans and individual investors as the primary sources of development and operating capital. These sources of capital are limited in capacity and can garner interest rates from 15-25%. While the legalized cannabis industry has made great strides in removing much of the negative stigma surrounding the products and their uses, resulting in the opening of some additional funding sources such as crowdfunding and angel investors, the cost of these capital sources is still significantly above the conventional market rates. At Ebee Management Group, we would argue that the most underutilized yet best financing tool presently available for the cannabis industry is the Commercial Property Assessed Clean Energy (C-PACE).

C-PACE is an innovative financing tool that gives owners of commercial, industrial, and multi-family properties access to long-term fixed-rate financing for energy efficiency, water conservation, and renewable energy projects. The C-PACE legislation authorizes municipalities or counties to partner with private capital providers to deliver financing options to commercial property owners for energy qualified improvements with the collection of the debt repayment through a special assessment on the property’s tax bill. The C-PACE funds provide upfront capital with 100% financing for qualified improvement often with terms up to 20 years. The resulting energy savings and reduced operating and maintenance costs typically exceed the amount of the assessment payment and often contribute to a positive cash flow to the operating budget.

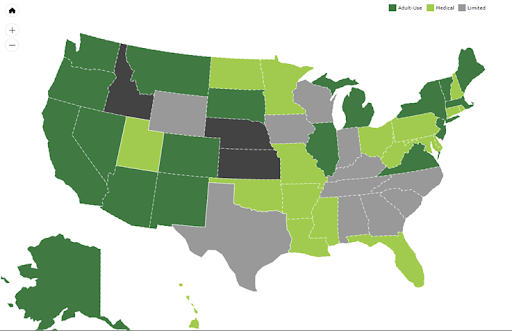

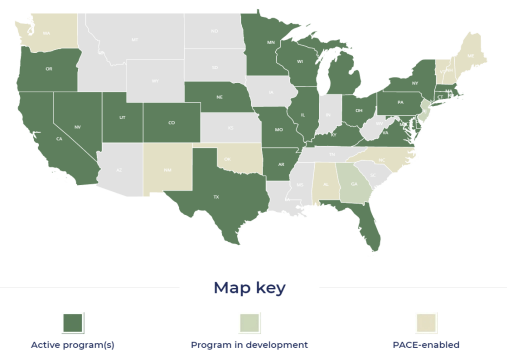

The primary caveat to the use of C-PACE for cannabis is that the property must be in a state that has passed the legislation that empowers local municipalities to provide C-PACE as a funding tool. C-PACE can be funded directly by the municipality through a bond issuance; however, most projects are presently being funded by the private equity markets. Typical terms on a C-PACE-funded cannabis transaction are 100% financing, fixed for a term up to 20 years at interest rates ranging from 7%to 9%. The maps below illustrate the current enactment of state-level policy for both cannabis and PACE.

Map provided and maintained on the PACENation website

C-PACE can be utilized for any improvement that saves energy with maximum lending limits influenced by individual state legislation and program guidelines. Typically, the maximum loan amount is capped at 20-25% of the completed appraised value and restricted to funding only qualifying improvements. Typical qualified improvements include lighting, HVAC systems, and building controls, doors, windows, roofs, and alternative power generation like wind and solar. PACE can be used for retrofitting an existing building, new construction, and in some states, refinance of existing debt. For the established cannabis market, the refinance option is an extremely attractive tool because it can be utilized to pay off higher-cost investor debt and is non-recourse to the owner. The debt is tied to the physical facility as a special assessment, not a mortgage lien, and is thus fully transferable at sale. You heard me right. If you have a short-term hold strategy for a facility, any remaining obligation you have associated with your PACE assessment does not have to be paid off at closing. The balance of the debt follows the tax bill and transfers directly to the new owner like any other existing tax-based assessment.

The table below outlines the benefits and features of C-PACE

Owner Benefits

Financing Features

Qualified Equipment

• Lower cost capital

• Non-recourse to owner

• Preserves owner’s capital

• Debt transfers at sale

• 100% financing of qualified improvements

• Long-term fixed-rate up to 20 years

• Competitive interest rates ranging from 6.5%-9.5%

• Debt securitized by a special assessment on the property

• Lighting

• HVAC

• Controls

• Roofs

• Doors & Windows

• Insulation

• Power factor conversion

• Alternative energy generation

The future of a wider array of funding options for the cannabis industry will clearly be impacted by both the ongoing adoption on a state-level and the possible federal-level legalization. Presently the pressure from states like New York and Chicago that house the two largest capital markets in the United States is leading to the expanded conversations about tapping into some of these sources of capital. That being said, arguably the best real-time solution for structuring a cannabis capital stack is C-PACE. New construction, building retrofit, or refinance, C-PACE can fill a gap or serve as a lower-cost replacement of other investment capital or equity.

Dr. Teresa Smith leads the Strategic Growth & Development for Ebee Management Group where she is recognized as an industry expert in sustainable development, leveraging PACE financing solutions for qualified energy efficiency projects throughout Ohio and Michigan. Prior to joining Ebee in 2019, Teresa was the Business Development Manager for the Toledo-Lucas County Port Authority where she built a robust growth process that delivered a 280% annualized increase in Property Assessed Clean Energy (PACE) loan transactions, driving loan balances from $3 million in 2011 to $47 million in 2019. Teresa obtained a Bachelor Degree in Economics from Eastern Michigan University, a MBA in Executive Management from the University of Toledo and a Doctorate Degree in Business Management with a specialty in Leadership from Capella University.

Ebee Management Group is a full-cycle construction, finance, and energy management firm, offering our clients the most cost-effective and appropriate development strategies — never compromising integrity and quality. We oversee every aspect of the project with a proprietary process and unique energy financing programs, delivering a custom designed, state-of-the-art energy savings solution with a guarantee to save you time, energy, and money. Ebee offers a wide array of financing solutions for the Cannabis Industry that reduce equity requirements and replace much more expensive sources of capital. Our flagship financing tool for new construction, renovation and refinance of commercial facilities is Commercial Property Assessed Clean Energy (C-PACE). This financing tool makes it possible for owners and developers of commercial properties to obtain low-cost, non-recourse, long-term financing which is paid back through an annual assessment on the organization’s property tax bill. For more information, contact Teresa Smith at 419.340.0420, tsmith@ebeeco.com or visit our website athttps://www.ebeeco.com/

Member Blog: Common Cannabis Capital Cadence

by Sumit Mehta, CEO of MAZAKALI

NCIA’s Finance and Insurance Committee

Companies often benefit from capital infusions that can help them grow their businesses. When and how much capital to raise is a common question, once that is best addressed by balancing need for cash with dilution of equity. This article outlines typical stages for corporate growth along with potential sources of capital and required documentation along the way.

Common Cannabis Capital Cadence

Introduction

While a business does not need to raise money to be successful, one of the primary reasons businesses fail is that they run out of money. Businesses that do need money to survive or to accelerate growth can benefit from outside capital balanced by the related loss of ownership. Effective capital management is thus crucial to business growth and success.

Access to necessary capital can be a significant challenge, as money is cheapest to borrow when you least need it. Access to liquidity, while difficult in any industry, is even more challenging in the cannabis industry for a myriad of reasons. Despite these challenges, cannabis capital infusions are at an all-time high. Companies are well-served to be focused on ‘capital readiness’ well in advance of their desired capital needs.

The true entrepreneur does more and dreams less

Fail to prepare and you may be preparing to fail. Maintaining focus on cash needs and related documentation at every stage of your business growth is crucial to its ultimate success.

Idea Stage – Founders

A founder collaboration agreement can help lay out a working agreement along with conflict-resolution steps for future disputes. A common stock purchase agreement is a binding contract which highlights basic terms for the sale of shares to founders. This agreement will define the parties, the shares to be sold, the purchase price, the timing and method of payment, and the closing date. A shareholder agreement typically accompanies the stock purchase agreement and highlights shareholder rights, pricing mechanisms, voting arrangements and shareholder privileges and protections.

Documentation: Founder collaboration agreement, common stock purchase agreement, shareholder agreement.

Early Stage – Friends & Family

Friends and family can be some of the easiest sources of capital. They are typically more forgiving about business ups and downs, and having a resourceful network of trusted early investors is a good step towards securing money from future investors. It is common to use convertible notes at this stage, and relevant here are a convertible note purchase agreement along with a board of director consent. The intention of this note is that it converts to equity when the company conducts an equity financing.

Documentation: Convertible note purchase agreement, board of director consent.

Seed Stage – Angel Investors

An angel or seed investor is an affluent individual who provides capital for a business start-up, usually also in exchange for convertible debt. An advantage of this type of financing is that it is less risky than debt financing. In the event of business failure, invested capital does not have to be paid back. In addition to the documentation above, most angels will want to see a business plan and a pitch deck.

While the term ‘Venture Capital’ broadly applies to any capital provided to a venture, it typically describes a structured institutional scenario. Advantages of venture capital include amounts typically larger than angel funding rounds along with valuable information and resources that can contribute to business success. Challenges here include the length and complexity of the diligence process along with the documentation burden as highlighted below.

Documentation: A robust data room that includes the above documents along with a 5-year pro-forma model, cap table, valuation, subscription agreements, stock purchase agreements, incorporation documents & bylaws; and vendor, contractor & employee agreements.

Growth Stage – Private Equity

Private equity investments typically result in either a majority or a substantial minority ownership stake in a company. These generally come with strings attached, which can be wound tightly at times. While private equity offers the opportunity to raise large amounts of capital, it is also often accompanied by a loss of control. In order to amplify returns, private equity firms typically raise a significant amount of debt to introduce leverage into the transaction. This has helped coin the term ‘Leveraged Buyout’.

Documentation: A robust data room as above with PE specific documents that may include supply chain verification, tax and audit, legal reviews, intellectual property opinions and management team background checks.

Final Stage – Public Equity

A substantial increase in liquidity is one of the main advantages of this final stage of liquidity. Other advantages include increasing brand and prestige, attracting employees with a stock option plan, and making acquisitions with company stock. Going public is no easy task and requires a large absorption of new obligations, including filing SEC reports, getting shareholder approval for corporate actions, additional legal liabilities and other regulations as introduced by the Securities Act of 1933 and its many subsequent amendments.

Documentation: In addition to compliance with Regulation FD and Sarbanes-Oxley, filing and reporting requirements include annual reports, quarterly reports, proxy statements and insider holding filings.

Conclusion: A sustained and successful capital cadence raises investor confidence and subsequent recommendations to others. Determining a timeline for liquidity is the cornerstone of capital raise decision-making, and a plan created with financial rigor is useful for management and investors alike. While the preservation of liquidity is of primary importance, this is best balanced by the desire to retain ownership and control. When and how to raise money are amongst the biggest challenges for any business, and preparation is paramount to the capitalization of the arrival of opportunity.

Chance often favors the prepared.

In addition to his role as Founder and CEO at MAZAKALI, Sumit is a consultant to The Arcview Group and the Managing Partner of Emerald Ventures. A frequent speaker at investment seminars, Sumit acts as a mentor to Arcview and Canopy companies and serves on the Canopy Investment committee as well as the NCIA Finance & Insurance committee. Sumit and MAZAKALI support NCIA, the Marijuana Policy Project and Students for Sensible Drug Policy.

Sumit has earned an MBA from the University of Michigan, a BA in Economics with Honors from the University of Texas and currently holds Series 7, 63, 65 and 79 licenses. He resides in San Francisco where he enjoys riding his motorcycle, yoga, and craft beer.

Dr. Teresa Smith leads the Strategic Growth & Development for

Dr. Teresa Smith leads the Strategic Growth & Development for

Follow NCIA

Newsletter

Facebook

Twitter

LinkedIn

Instagram

News & Resource Topics

–

This Just In

How THCa Vapes Are Changing Consumer

Announcing NCIA’s 2026-2028 Board of Directors