Navigating the Confusing, Crowded World of Cannabis Payments

When you’re a cannabis retail operator looking for electronic cannabis payment solutions you’re faced with a baffling array of options and it’s hard to pick out the ones you can trust and the ones that you should avoid at all costs. Every potential vendor is going to tell you that their solution is the best (trust me!) so you need to understand the basic landscape of cannabis payment solutions in order to know what questions to ask. There’s a lot of solid vendors out there that only want to help the industry but there are, sadly, those out there that prey upon a lack of familiarity with the crowded, confusing payments landscape to push solutions that are at best unsustainable and at worst fraudulent.

ACH transactions are a way for a person or a business to do direct bank money transfers.

These transactions are conducted on a computer network run by NACHA, the National Clearinghouse Association. Since these don’t run over the networks run by the credit card companies like Visa or Mastercard – known as “payment rails” – these transactions don’t violate their rules. While NACHA hasn’t officially made a statement either way about cannabis, their actions suggest they don’t have an issue processing these transactions over their network.

The downside with many ACH solutions is that they aren’t necessarily convenient for the buyer. Because a customer or patient can’t just pull out a bank card they are often required to download an app and provide banking details like account and routing numbers. This isn’t necessarily an issue from the second purchase forward, but this can be a bit of a pain for a customer or patient trying to use an app for the first time if they’re not expecting to have to go through an account onboarding process that might take several minutes. The upside to this is that there are platforms that allow the buyer to upload funds via ACH to an eWallet, which, after the initial transaction, will enable them to make instant purchases. Platforms also allow the buyer to automatically replenish their eWallet via ACH, allowing them to always have funds to make purchases. These purchases can also be combined with a store’s loyalty points program.

Questions to ask about ACH solutions:

What does a customer or patient need to do to use the solution?

How long does it normally take for the funds to transfer, allowing a user to make purchases?

Are there any contactless platforms that allow a buyer to purchase the product for delivery or curbside pickup?

Do you need additional hardware to display a single-use QR code specific to the transaction?

Cashless ATMs and PIN Debit solutions are among the most common electronic payment methods that allow customers to directly use cards.

To discuss the issues that go along with any card-based solution we need to take a step back and talk about how payments are processed. As previously mentioned, every credit card company has a set of rails used by merchants to process a sale over their network. Each transaction is sent as a packet of information that broadly contains the following information: name of business, location of business, any additional merchant information, and merchant category code (MCC).

Every transaction has to be associated with a four digit MCC used by the merchants to indicate the nature of the business and the transaction. The code that’s traditionally been used by cashless ATMs and PIN Debit solutions is 5912, reserved for pharmacies and “cannabis (where legal to do so)”. This is what’s used in Canada where credit cards are an option but it’s not an acceptable option in the US because the major credit card networks have clarified that their rails cannot be used for the purchase of marijuana. They do so by prohibiting activities associated with “controlled substances, or recreational/street drugs” (VISA) or even more broadly “any Transaction that is illegal” (Mastercard) in their operating agreements.

It’s important to note that you can’t just randomly choose an alternative MCC because miscoding constitutes fraud. You may remember a few years ago that California-based delivery company Eaze was prosecuted in 2019 for using MCC codes associated with things like “carbonated drinks, green tea, face creams and other products” in an attempt to obscure the fact that the network was being used for the direct purchase of marijuana.

It should be noted however that there are a few ATM networks out there that aren’t directly owned by the big credit card companies like NYCE, Allpoint, Star, and Moneypass. These companies have been relatively quiet regarding the use of their networks for the purchase of marijuana products, so there is an argument to be made that if card transactions are sent over those rails they’re not violating any operating rules, but anecdotally we’ve heard that some of these networks aren’t necessarily cannabis friendly and, as private companies, they’re able to change their mind (for or against) whenever they wish.

Questions to ask about Cashless ATMs and PIN Debit solutions:

What MCC code is the payment processor using?

What network is being used to process the transaction?

Credit cards are notoriously off-limits to cannabis because of the very public positions taken by the major card networks but that doesn’t stop companies from popping up offering credit card processing for cannabis purchases. Let’s clarify here at the outset – there is no way to directly purchase marijuana with a credit card in the United States with a credit card from American Express, Visa, Mastercard, or Discover.

So, with necessity being the mother of invention, some companies are trying out a new strategy to get credit card processing into dispensaries legally. Among them are solutions that take advantage of another MCC code: 6051. This code is associated with the purchase of “liquid and cryptocurrency assets” and some enterprising payment providers are using it to set up a structure where a customer isn’t “technically” buying marijuana. Instead they are “buying” what’s called a “stablecoin”, a form of cryptocurrency whose value is pegged 1:1 to the US dollar.

Questions to ask about cryptocurrency or stablecoin solutions:

What MCC code is the payment processor using?

What stablecoin is being leveraged?

How is the stablecoin preserving its value?

What will the offramping of funds from a crypto wallet to my DDA account look like to my bank?

Cannabis retail operators are faced with serious business and legal considerations when determining the payment processing solution provided to patients and customers. What solution will be the easiest for the customer? Is the solution compliant?

The cannabis industry’s evolving legal and regulatory landscape is challenging, especially with bad actors seeking to implement non compliant make-shift payment solutions intended to capitalize off of cannabis businesses seeking efficient and effective cannabis payment solutions. It is essential that you do your due diligence on cannabis payment solutions presented to your business to confirm that it will not cause an issue for you, the business and its patterns and customers. We hope that this article outlines considerations that will allow you to protect your business and its patients and customers.

Committee Blog: Defining Legal Hemp – It Isn’t Always Simple Math

If you are a cannabis-related business, and are looking to accept credit cards, it is only possible to do so if you are selling a product that is defined as legal hemp by the 2018 Farm Bill.

The 2018 Farm Bill provides that:

“The term ‘hemp’ means the plant Cannabis sativa L. and any part of that plant, including the seeds thereof and all derivatives, extracts, cannabinoids, isomers, acids, salts, and salts of isomers, whether growing or not, with a delta-9 tetrahydrocannabinol concentration of not more than 0.3 percent on a dry weight basis.”

For the most part, it’s pretty cut-and-dry. Marijuana is a schedule 1 drug. Hemp is not. If your product has less than .3% Delta-9 on a dry weight basis, it’s not marijuana, it’s hemp. And since it’s hemp, it’s federally legal. And since it’s federally legal, it can be purchased with checks, credit cards, or debit cards. Hemp products are, reductively, as incendiary as a stick of butter.

Of course, there is the law and there is how acquiring banks—banks that offer merchant accounts—interpret the law. Across the U.S., there are hundreds of acquiring banks. Of those, only six or seven offer merchant accounts to hemp businesses.

That’s it, plus payment service provider Square.

The immediate problem for the few acquiring banks that have, laudably, said, “Yes,” to hemp is, “how do we distinguish products that are .3% Delta-9 or less (and therefore, yawningly legal) from those that are over .3% Delta-9 (and therefore, illegal as angel dust)?”

Enter the Certificate of Analysis, or COA, or lab report. While there is nothing in the law stating that COAs are required to prove that a product is within the federally legal limit, their role is sacrosanct during the boarding process. For every hemp-derived product, there must be a corresponding COA proving that the product being sold is hemp, and not marijuana.

Fortunately, there are labs across the nation. The U.S. Department of Agriculture website lists 85, as of May 2023. Manufacturers and businesses ship their samples to these labs. The labs run their tests and the COAs are issued.

Simple, right?

Not really.

There are no standards in place for these reports. No templates. Every laboratory’s COAs—while substantively providing the same information—look a little different. Furthermore, most bankers haven’t seen a lab report since high school chemistry, and you’ve got a recipe for confusion or misunderstanding (frequently both).

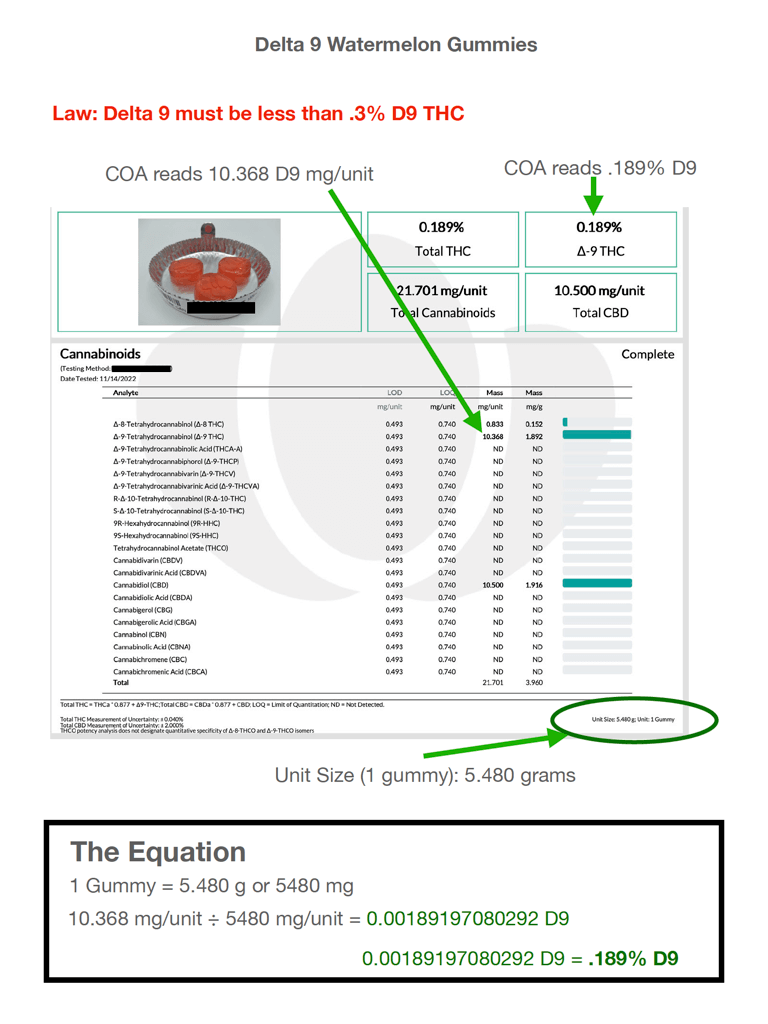

This COA, when it was initially presented to the bank, was rejected. To the underwriter, it was an open and shut case.

When the bank opened its door to offering acquiring to hemp businesses, its policy was to reject anything with greater than .3% Delta-9 by weight.

The top of this COA showed an instance of Delta 9 that read .189%. That passed muster, certainly. However, when he delved further into the analyte detail, he noted additional Delta-9 figures in excess of the .3% limit:

10.368 in the mg/unit cell

1.892 in the mg/g cell

It was not clear to the bank’s underwriter which of the two—per-unit or per-gram—corresponded with the by-weight percentage he was to be mindful of, but both were certainly over the .3% limit.

So, open and shut case: DECLINED

The salesperson that brought the merchant to this bank was surprised by the rejection. He hadn’t looked at the COAs very closely, but it seemed unlikely that this merchant had been selling products on her website that were in excess of .3% Delta-9.

Why? Because if the merchant had been selling products on its website in excess of .3% Delta-9, it would have been engaging in egregious felony drug trafficking. The salesperson doubted that was the case.

The salesperson did something he didn’t normally do: he took out his calculator.

He wanted to know why it read .189% Delta 9 at the top, but 10.368 in the analyte table. He noted the unit size at the bottom of the page was a gummy weighing 5.480g.

For the sake of simplicity, he multiplied that by 1000 to convert it to milligrams. That made it 5480 mg

Then he entered the onerous 10.368mg from the mg/unit figure in the analyte table and divided it by 5480mg. The resulting calculation netted the following total: .0018919.

Next, he converted it to a percent, and found that the result was .189%, which matched the figure at the top of the COA, exactly.

The next day, the salesperson presented the COA to the bank, with the markings and The Equation just as shown here.

It was an open and shut case: ACCEPTED

This situation is an example of why banks and credit unions unknowingly reject compliant hemp businesses from merchant processing solutions. As stated, a simple mathematical calculation was the difference between being accepted or rejected for necessary merchant processing services. Without proper merchant servicing not only are cannabis businesses’ profitability affected because they can only take cash; cash is also not as traceable or auditable as electronic transactions.

In general, businesses providing services to the cannabis industry are often challenged with disentangling legal risks with the benefits of their necessary services providing more transparency. With enhanced knowledge of the cannabis industry and its parameters, the cannabis industry will recognize a greater participation by all businesses necessary for the life of the industry thereby enhancing cannabis businesses’ likelihood to succeed but also enhancing the legitimacy and regulation of the industry.

Member Blog: Debit and Credit Card Processing at Your Cannabis Dispensary, Finally

Accepting money for legal and licensed cannabis dispensaries has been like the wild west over the past few years. In the U.S., the banking landscape for marijuana businesses is confusing and can seem flat-out impossible to organize. Because of this, many shops still take cash for most of their payments. In 2023 this should not be the case. The problem is that many dispensaries have no access to debit card processing that allows them to take card sales but with severe limitations. Here we’ll look at some signs it is time to upgrade your cannabis debit card processing provider.

Processing Fees & Rates Per Transaction

The most straightforward item to look at is the processing rates and per-transaction fees for your cannabis dispensary. This has gotten more competitive over the years, with merchant service providers pushing down rates to stay relevant. But the fact remains that many cannabis merchant services have higher rates and more expensive per-transaction fees than what businesses should be paying in 2023.

Long gone are the days of dispensaries and marijuana accessory shops being labeled “high-risk” by banks. We’ve come a long way, but dispensaries are still looked at in an unfair light when compared with traditional business varieties. If you are facing direct deposit times longer than one business day, providing high cash reserves to your processor, and paying anything more than regular processing fees, it’s time to make a change.

Why Offer Credit & Debit Card Processing

When a patient or customer enters a dispensary to make a purchase, dispensaries that do not have a cashless payment option may find they are limiting the amount of product they can sell. Look at it this way; a patron comes into the dispensary with $80. They plan to spend a total of $80 on cannabis. However, when they get to the counter and see the great options, they think, “I’m here now; why don’t I double up my order and save myself the next trip.” Or they see the menu options and want to try a few varieties, quickly getting over $80. But they only have $80 cash in hand, no ATM nearby, and the dispensary doesn’t have a card-paying option. The dispensary misses out on more business, and the patient or patron is disappointed.

This is the last place we want to find our customers as business owners. If they have a desire and you have the product, you should be able to meet them in the middle and offer additional options for making their purchase.

The Point Is…

Dispensaries who offer cash-only payment options lose sales, period. How many times have you seen customers in this scenario? They come to your cannabis dispensary and browse the menu. Make a few choices, but when it’s time to pay, a problem, your dispensary only takes cash, and the customer doesn’t have any on them. Don’t leave sales on the table (literally) because you don’t take any form of card payment. POS systems are often free and can be installed easily in a matter of minutes. It also eliminates the need for making cash deposits at the bank or installing a cash management system to keep staff in check. It is a true win-win for dispensary owners and accessory businesses. In 2023, not offering a card payment option is just silly.

Benefits of Changing your Merchant Service Provider

There are a few key reasons to upgrade your processor; let’s take a quick look:

get new and better processing rates

eliminate per transaction fees

upgrade your card reader and touchless payment options

allow customers to make larger purchases

eliminate cash where possible and streamline the customer experience

take higher tickets per customer

improve direct deposit time frames

increase sales volume and profit margins

Offering customers every available payment option will give them confidence in their cannabis purchases. Therefore making them more likely to return.

Find the right Cannabis Merchant Service in the U.S.

So many merchant services are out there, but few specialize in the cannabis industry. This industry isn’t like others, so it stands to reason that working with a cannabis-specific company makes the most sense. You don’t want to use a big box bank that will look for reasons to pile on fees and moral judgment. Working with a smaller cannabis-focused outfit is something the entire industry should consider.

Stuart Lutterman is the owner/founder of Brother Processing Solutions (BPS), a family-run business with more than fifteen (15) years of experience in the Merchant Account/Credit Card Processing industry. BPS specializes in all cannabis business varieties from farming, processing, packaging, and sales of both recreational & medical dispensaries as well as Indigenous-owned businesses. BPS works closely with every client, understanding their individual needs, and providing a direct point of contact to financial services across the board. https://BrotherProcessing.com

Dispensaries who offer cash-only payment options lose sales, period. How many times have you seen customers in this scenario? They come to a cannabis dispensary and browse the menu. Make a few choices, but when it’s time to pay, a problem… your dispensary only takes cash, and they don’t have any on them. This problem is so common we shot a commercial about it.

Member Blog: Dude, Where’s My Payments?

by Gary Strahle,

Cannabis industry merchant service providers get shut down. How has this impacted retailers and at what cost? Learn how operators are mitigating theft and working with the National Cannabis Industry Association to drive legislation.

In order to best understand what payment methods will suit you best, you must first understand the inherit risks that are associated.

Let’s put it bluntly; there is no such thing as a federally compliant payment in cannabis, not even cash. Given states have legalized the sale of medical adult-use cannabis, it is still very confusing and in some cases crippling when choosing your method of payments.

Cash is king.

Because federal banks legally can not do business with the cannabis industry, retailers have limited options for securing their resources. This makes dispensaries targets for theft. Criminals are coming after both product and cash which requires operators to make heavy investments in security systems. These include state-of-the-art video surveillance, 24/7 on-site security, steel doors, bulletproof glass, expensive safes, terrible insurance policies, and a lot of trips to your favorite credit union. State-chartered credit unions are the only banks accepting cash from cannabis businesses.

Although cash comes with some inherit benefits, coins don’t. Coin change is a big problem for retailers as there has been a national coin shortage. What are you supposed to do when your angry customer is complaining over the 75 cents you can’t return to them? Do you give them customer credit? Do you make an adjustment or a discount? Do you request your POS provider to create a “round up” feature that brings every cash-related transaction up to the nearest dollar?

Benefit:Tax Exposure.

Risk: Tax Exposure, Theft, Time, Money

So what about Cashless ATM?

A cashless ATM is where customers break out their debit card at the register to pay for their retail purchase. Just like any other ATM, you are drawing against an even $10 or $20 amount from your bank account. So if your purchase was for $17, a budtender would hand you back $3 cash in change for your purchase.

While there has been mixed results with cashless ATM’s there was a crackdown made by Visa and Mastercard to shutdown these types of transactions on their network. A significant number of retailers lost their capability to process all of a sudden and had to revert to cash-only payments. While a good chunk of the high risk payment providers were shut down, others continued processing without service interruption for reasons I will explain later.

Although cashless ATM payments can mitigate some of the risks involved with cash on hand, they are subjected to a number of costs that can factor into your daily management and or customer experience. First, if your payment terminals are not integrated with your retail POS, good luck reconciling your money at the end of the day. Budtenders will frequently miscode payments on the POS and assign card payments to cash transactions or vice versa. This makes it extremely tedious to reconcile your books. On the other hand, everyone hates ATM fees. Our colleagues have witnessed fees as high as $25 in places like Las Vegas. Typically you will see most cashless ATM fees between $3-3.50, however, it is common to see them even higher.

Benefit: Processed as an ATM transaction(not a Cannabis Transaction) Settlements are deposited directly into the bank.

Risk: Added fees to customer.

What is different about Pin Debit?

Pin debit allows charges to the penny. This is a cool way to allow customers to pay with their debit card without having to pay the ATM fees. It is relatively new and still unclear if these processors will get away with miscoding their RCC. If you looked at the customers bank statement you would see the charge from your dispensary just like a cashless ATM however the way it got there is much different. Processors are telling networks and banks that these are “pharmacy” transactions. When a customer calls the bank and discusses your transaction at a cannabis dispensary it would seem like things could start going down hill quick for both the payment provider and the merchant (dispensary). With all risk considered it remains as an option for many to process their payments. In conclusion what I’m about to share about credit payments would make you consider pin debit twice.

Benefit:To the penny charges, no ATM fees.

Risk:Miscoded RCC, Merchant Service Shut Down.

How about plain debit or credit?

Don’t do it. This from personal experience has impacted my life. A close family friend was indicted and served time in jail for fraudulently processing credit card payments for delivery giant Eaze. This was a get-rich-quick scheme that broke friendships, businesses, families, and a healthy portion of the retail cannabis industry. Just like pin debit, credit charges are miscoded but in this case purchases were being identified as “dog treats” or “flowers.” The charges would not show up on the customer bank statement as a purchase from a dispensary. Understanding the high risks associated with processing cards in such a way is explicitly fraudulent and has the highest likelihood of involving some form of trouble .

Benefit:Massive increase in Sales.

Risk:Non-payment, Chargebacks, Miscoded RCC, Merchant Service Shut Down.

In summary.

If you or your business are looking to service card payments for your customers, choose your options wisely. In my own personal opinion, you face the least amount of risk using an integrated cashless ATM solution, however if the customer is demanding a more traditional debit experience then it could be worth running a cost/benefit analysis.

The bottom line is that those who have the most dynamic and redundant integrated card payment solution will be the most continuous while mitigating the risks of cash. The payment providers getting shut down do not have redundancy in their network providers or payment methods and therefore non sustainable.

Some payment providers will eat the time in jail and or fines as they are or were able to make a significant amount of money greater than the cost of the punishment.

Until we can successfully make legislative changes being pushed forward by NCIA, those who care about making change should donate to their cause and participate in NCIA’s 11th Annual Cannabis Industry Lobby Days in 2023.

Author: Gary Strahle is a Technical Architect with over a decade worth of operational cannabis industry experience. 2023 NCIA Retail Committee Chairman. Avid surfer and golfer with a passion to help others.

Cannabis Cloud – Applications, Consulting & Payments. Founded in 2015, providing service to over 2,500 cannabis businesses. Specialized as a Salesforce Partner innovating industry standard solutions from seed to sale, Cannabis Cloud’s payments integrated Retail Point of Sale hosts a robust api for connecting Metrc as well as external menus such as Weedmaps or Leafly.

Member Blog: Payment Processing In The Cannabis Space

There is a lot of confusion about payment processing in the cannabis space because payment processing is somewhat confusing to begin with, and because, in the cannabis space, ambiguity is a way of life.

The title of this very blog post could, realistically, seem misleading to some.

So, to be clear, when I say, “Cannabis Space,” I mean the entire industry — from plant-touchers (CBD included) to the ancillary businesses built up around it.

The passage of the 2018 Farm Bill marked an exciting new chapter for the industry. Suddenly, CBD, or, more specifically, any ingestible cannabis product containing .3% THC or less by volume, was classified as hemp. And since it is marijuana, and not hemp, that is defined as a Schedule I substance under the United States Controlled Substance Act, the Farm Bill, technically, made products like CBD as legal as cow milk — federally, anyway.

The upshot of this new classification is that now, at least some players in the cannabis space can market their products to a national base of consumers and clients, and they can do so by accepting credit cards as payment.

However, the myriad Acquiring Banks across the United States have not exactly jumped for joy at the prospect of providing credit card processing in the form of merchant accounts to CBD retailers. Reticence rules. CBD is considered high risk, and four years on, only a handful of them have thrown their hat in the ring.

Jargon Alert I: Acquiring Banks and Issuing Banks

In merchant processing parlance, banks fall into two categories: Acquiring Banks and Issuing Banks. Acquiring Banks, or, Acquirers, provide merchant processing accounts to businesses wishing to accept credit card transactions. Issuing Banks, short for Card Issuing Banks, are banks that offer branded payment cards directly to consumers. For example, if your bank has ever offered you a Visa card, it is an Issuing Bank (not that it couldn’t also be an Acquiring Bank, too).

Jargon Alert II: CBD is ‘High Risk’

CBD is deemed high risk by the card associations (i.e., Visa, MasterCard, American Express), and when the card associations deem a product or industry high risk, most Acquiring Banks tap out. This is because financial institutions are, by nature, risk averse (subprime mortgage crisis notwithstanding).

So let’s talk for a minute about risk. High risk, that compound term, is a truncation of a longer phrase: ‘Higher risk of fraud or chargebacks.’

Why are CBD products at higher risk of fraud? It’s impossible to say for sure since the Visas and MasterCards of the world are publicly traded companies with their own trade secrets and IP, but there are several characteristics unique to CBD, or any cannabis product now federally legal, that likely figured into that decision.

Those FDA disclaimers that CBD retailers must print or paste on all product packaging and webpages are as good a place as any to start. They are mandatory because none of the benefits assigned to CBD have been clinically proven. There just isn’t enough data or testing at this point, and no big story there. That’s what happens when you demonize a plant for 100 years.

Consequently, from the perspective of the FDA, and the card associations, by extension, consumers are making CBD purchases with baked-in expectations based, exclusively, on word-of-mouth advice and anecdotal data. That’s a recipe for dissatisfied customers. And dissatisfied customers tend to charge back transactions.

The card associations, and the banks who provide merchant accounts, worry incessantly about fraud and chargebacks.

Too Close for Comfort

Dissatisfied customers aside, there are onerous legal nuances that make the prospect of boarding cannabis merchants, even those selling products that are federally legal, daunting for banks.

Selling a product with .31% THC across state lines is felonious. It is a federal offense. Violating a law like that could get a bank’s charter revoked, or, at a minimum, result in massive fines.

On the other hand, selling a product with .30% THC across state lines is 100% federally legal. As stated above, safe as milk, federally.

That is a heck of a distinction. If any product contains more than .3% THC by volume, it is ‘marijuana’ in the eyes of the federal government. From the perspective of the banks, that’s a little close for comfort. Furthermore, banks don’t operate laboratories. They must rely on testing data presented to them in the form of third-party lab reports — Certificates of Analysis or COAs for short — to verify that the products being sold are federally legal.

The last thing an Acquiring Bank wants to do is violate a federal law EVER. It could result in a loss of their charter, lawsuits, and massive fines. And it’s important to keep in mind that the Acquiring Banks out there offering merchant accounts to CBD retailers are not giant, publicly traded institutions like Bank of America or Wells Fargo. They tend to be much smaller, and therefore, have infinitely smaller war chests for court cases.

Still, separating the federally legal Tier I cannabis product from the federally illegal Tier I cannabis product should be pretty cut-and-dry. If the product you’re selling is .3% THC by volume or less, it is exempt from the Controlled Substance Act (CSA). If that threshold is documented in the product’s Certificates of Analysis (COA), you ought to be able to sell it.

Unfortunately, it’s not that simple. When bank underwriters look at percentages of Delta 8, Delta 9, and Delta 10 on the COAs that cross their desks, they’re frequently at sixes and sevens trying to figure the whole thing out.

From the perspective of the 2018 Farm Bill, a cannabis product is hemp if it contains .3% Delta-9 THC or less by volume, but what everybody says is “.3% THC or less by volume.” Consequently, when the compliance officer at the bank is performing her due diligence by inspecting the COAs corresponding to each product, she may encounter a lot of crooked numbers, and she may blanch at the results.

Those results, often, look something like the following:

00.195% D9-THC

52.475% d8-THC.

Federally, the Delta-9 threshold is the only threshold that matters. The 2018 Farm Bill says as much, and the 9th Circuit Court of Appeals in California affirmed it in a ruling this past May. Therefore, in the example above, the Delta-9 threshold has not been crossed. It’s not even close. It is textbook HEMP, even if the Delta-8 threshold is off the charts.

However, if the compliance officer was provided the remit, “.3% or lower,” he’s likely to look at this and say, “Fail,” without realizing that the Delta-8 THC information is irrelevant as far as federal law goes.

Complicating the underwriting further is the fact that there is, to date, no standard template for COA reports. Every lab presents them differently. Bank compliance officers rarely moonlight as scientists. Like most of us, these CBD COAs are probably the first lab reports they’ve looked at since high school chemistry.

Furthermore, the banks can set their own rules. They don’t have to board CBD merchants. Few do, and those few that do have their own standards and practices.

Todd Glider has been an e-Commerce leader since the start of the Internet age. He has an MFA in Creative Writing from the University of Miami, and has served as CEO for small and medium-sized technology companies in Spain, Austria and the United States. As our Chief Business Development Officer, Todd introduces MobiusPay’s suite of award-winning financial services to new industries, and implements the development strategies and key partnerships needed to bring value to new customers.

MobiusPay, Inc. is a U.S.-based global financial services organization that is committed to empowering individuals and businesses. For more than a dozen years, MobiusPay has leveraged state-of-the-art secure billing technology, long-standing relationships with financial institutions and award-winning customer support to provide merchant processing and payment solutions to brick and mortar and digital businesses around the world.

Stuart Lutterman is the owner/founder of Brother Processing Solutions (BPS),

Stuart Lutterman is the owner/founder of Brother Processing Solutions (BPS),  Author: Gary Strahle is a Technical Architect with over a decade worth of operational cannabis industry experience. 2023 NCIA Retail Committee Chairman. Avid surfer and golfer with a passion to help others.

Author: Gary Strahle is a Technical Architect with over a decade worth of operational cannabis industry experience. 2023 NCIA Retail Committee Chairman. Avid surfer and golfer with a passion to help others.

Todd Glider has been an e-Commerce leader since the start of the Internet age. He has an MFA in Creative Writing from the University of Miami, and has served as CEO for small and medium-sized technology companies in Spain, Austria and the United States. As our Chief Business Development Officer, Todd introduces MobiusPay’s suite of award-winning financial services to new industries, and implements the development strategies and key partnerships needed to bring value to new customers.

Todd Glider has been an e-Commerce leader since the start of the Internet age. He has an MFA in Creative Writing from the University of Miami, and has served as CEO for small and medium-sized technology companies in Spain, Austria and the United States. As our Chief Business Development Officer, Todd introduces MobiusPay’s suite of award-winning financial services to new industries, and implements the development strategies and key partnerships needed to bring value to new customers.

Follow NCIA

Newsletter

Facebook

Twitter

LinkedIn

Instagram

News & Resource Topics

–

This Just In

Beyond Rescheduling: Inside NCIA’s 14th Annual National Cannabis Industry Lobby Days

DOJ Reschedules Medical Cannabis to Schedule III & Announces June 2026 Hearing on Broader Rescheduling