A potential U.S. Central Bank Digital Currency (CBDC) represents one of the most disruptive technologies on the horizon for the financial world, with profound implications for the cannabis industry. While a “digital dollar” could theoretically solve the industry’s payment rail issues overnight, it also introduces significant threats related to privacy, data security, and direct federal oversight, creating a high-stakes dilemma for cannabis businesses and the institutions that bank them. However, recent developments have fundamentally altered this landscape, particularly the January 2025 Executive Order 14178 halting U.S. CBDC development and ongoing progress with cannabis banking legislation.

Current State Analysis

The conversation around a U.S. CBDC has evolved dramatically from academic theory to active research, most notably through the Federal Reserve’s collaboration with MIT on “Project Hamilton,” which completed its Phase 1 research in February 2022. However, in January 2025, President Trump issued Executive Order 14178, explicitly prohibiting federal agencies from “undertaking any action to establish, issue, or promote a CBDC” and revoking previous digital asset policies. This makes the United States the only major economy to halt CBDC development through executive action. Despite this policy shift, understanding the potential impacts of CBDCs remains relevant, as policy positions can change with administrations, and other countries continue rapid CBDC development that could influence global financial systems. For the cannabis industry, banking challenges persist despite the executive order. The core issue remains the industry’s reliance on private-sector workarounds. Fintechs and banks have invested heavily in BSA/AML programs to manage the risks of handling cash deposits.

Legislative Developments

Simultaneously, significant progress has occurred with cannabis banking legislation. The SAFE Banking Act evolved into the SAFER Banking Act (S.2860), which passed the Senate Banking Committee with a bipartisan 14-9 vote and awaits a Senate floor vote. This legislation would provide safe harbor protections to financial institutions serving state-legal cannabis businesses, potentially resolving many banking challenges independent of any CBDC considerations. Additionally, cannabis rescheduling efforts at the federal level could fundamentally alter banking access. While rescheduling alone wouldn’t resolve all banking issues, it would reduce regulatory burden and risk perception for financial institutions considering cannabis banking services.

Regulatory Landscape

The introduction of a CBDC, if policy were to reverse, would create a direct and unavoidable conflict with the Controlled Substances Act (CSA). Every transaction involving a CBDC would be recorded on a central ledger managed by the Federal Reserve, raising critical policy questions about privacy versus surveillance. The Federal Reserve’s previous white papers presented various models, from anonymous, token-based systems (similar to cash) to account-based systems that would link every transaction to a verified identity. If the U.S. were to adopt an identity-based CBDC in the future, the federal government would have a real- time, unalterable record of every dollar spent at every state-licensed dispensary in the country.

Alternative Pathways

With CBDC development currently halted, the cannabis industry must focus on alternative pathways to banking normalization:

1. Legislative Solutions: Continued advocacy for the SAFER Banking Act and similar legislation that would enable traditional banking services.

2. Existing Compliance Frameworks: Further investment in robust compliance programs under current FinCEN guidance, which remains relevant despite policy shifts.

3. Private Sector Innovation: Development of alternative payment solutions that can operate within current regulatory frameworks.

4. State-Level Banking Solutions: Some states are exploring state-chartered banking options specifically for cannabis businesses.

Key Takeaways

• The January 2025 Executive Order significantly altered the U.S. CBDC landscape but hasn’t resolved cannabis banking challenges

• The SAFER Banking Act represents the most immediate potential solution for cannabis banking issues

• Banks should continue investing in current compliance technologies rather than waiting for CBDC or legislative solutions

• The cannabis industry must actively engage with multiple parallel policy debates that impact banking access

• Privacy concerns remain central to any digital payment solution for the cannabis industry, whether government or privately issued

• Cannabis rescheduling efforts represent another potential pathway to improved banking access independent of payment technology development

Service Solutions | 10.26.22 | Show Me the Money – The Current State of Cannabis Lending

NCIA’s Service Solutions series is our sponsored content webinar program which allows business owners the opportunity to learn more about premier products, services and industry solutions directly from our network of established suppliers, providers and thought leaders.

In this edition originally aired on Wednesday, October 26, 2022 we were joined by the experts from cannabis-focused financial institutions FundCanna, Safe Harbor Financial, and AVANA Companies to dive deep into the current state of cannabis lending with leading industry journalist John Schroyer of Green Market Report.

A decade after California and Colorado became the first adult use states, the regulated U.S. cannabis market encompasses over 70,000 cannabis-related businesses. Shockingly, most of those businesses still lack easy access to debt and other forms of growth and operating capital. From federal prohibitions and the impact of IRS regulation 280e, to state and local taxation issues, the costs of operating a regulated cannabis company continue to remain nearly unendurable.

Learn what may change in the coming six to 12 months so you’ll know how to access debt capital most cost-effectively in this ever evolving environment. No matter your place in the industry or the supply chain from cultivators, manufacturers, vendors, suppliers, distributors and retailers this conversation will provide the insights to meet your financial needs.

At the conclusion of the discussion our panel hosted a moderated Q&A session to provide NCIA members an opportunity to interact with leading minds from the financial services space, join today to contribute to future conversations!

Panelists:

Adam Stettner

Founder & CEO

FundCanna

Sundie Seefried

Founder and CEO

Safe Harbor Financial

02:13 – Equity vs. Debt: With equity dried up, should cannabis companies be looking at debt financing to grow now?

07:28 – Equity vs. Debt: What do borrowers need to do before approaching a debt provider (vs. an equity provider)?

13:25 – Equity vs. Debt: What can cannabis companies or entrepreneurs do to improve their overall credit worthiness prior to seeking capital?

17:16 – How has the interest rate increases by the Federal Reserve impacted capital markets (and the industry at large) in 2022?

26:07 – Audience Q&A: “If there’s “no reason not to have banking” for your cannabis business how can I easily (and inexpensively) establish and maintain a compliant bank account?”

28:56 – Lending: What significant lending challenges are your clients currently facing within the industry?

33:56 – Lending: What advice can you provide business owners for evaluating lenders that you should (or shouldn’t) work with and tips for avoiding predatory lending practices?

39:05 – Cannabis Reform: What impact do you expect President Biden’s recent announcement will have on the industry?

49:32 – Audience Q&A: “Are your financial institutions planning to offer lending and banking services in New York, New Jersey and other new markets?”

51:42 – Audience Q&A: “With the mindset of “Investors are betting on the Jockey not the Horse.” What type of CEO or founding team would be a red flag or not a viable investment?”

55:19 – Audience Q&A: “How can I start to shift my retail company from being primarily a cash-only business?”

1:05:03 – NCIA Member Appreciation Credit Sequence

Sponsored By:

VIDEO: Capitol Hill Update On Cannabis Banking Hearing In Congressional Committee

Every day, our Government Relations team is keeping our finger on the pulse of what’s happening on the Hill and how it affects our industry. In this case, we have important news from D.C. about movement to fix the banking crisis faced by cannabis industry operators.

Watch this video to learn more about the historic hearing that took place on February 13 in the Subcommittee on Consumer Protection and Financial Institutions. They held the first ever hearing on marijuana and financial services, entitled: Challenges and Solutions: Access to Banking Services for Cannabis-Related Businesses. Up for discussion was a new version of the Secure and Fair Enforcement (SAFE) Banking Act.

There’s no better way to stay informed and connected with what’s happening in federal policy than by being a member of NCIA – the largest and most influential national trade association representing the legal cannabis industry. We fight on your behalf year-round in the halls of Congress for our industry to be treated fairly like any other legitimate industry in this country.

Be sure to register in advance for our popular Cannabis Caucus event series – tickets are complimentary for NCIA members, and a limited number of non-member tickets are available. Join us throughout the month of March in Los Angeles, San Francisco, Denver, Lansing, and Philadelphia. For more information, visit our website.

And now is the time to start planning your trip to Washington, D.C. to join us on Capitol Hill! For the 9th year in a row, we’re hosting our Annual Cannabis Industry Lobby Days on May 21-23. This is your chance to walk the halls of Congress and make your voice heard about the unfair tax and banking policies that cripple our industry. This event is exclusively for current NCIA members, so if you’d like to join us for what NCIA members say is “the most important and exciting NCIA event of the year,” then now is the time to join NCIA at one of our three levels of membership, and then join us in May in our nation’s capitol.

If you’re already planning to join us, now is a perfect time to read up on our latest Policy Council report to learn more about priorities for our industry in the 116th Congress.

Help Economists Determine the Cost of the Banking Crisis

Editor’s Note: From time to time, NCIA hears from researchers looking into an issue related to the cannabis industry. Recently, two Northwestern University economics Ph.D. candidates contacted us because they are studying the economic impact of the cannabis industry’s lack of banking access. In order to complete their research, they need real-world data from cannabis businesses like yours.

This blog post explains their research. We encourage our members to take part in their research, as the results can help support our case for an immediate banking solution. To get involved, contact them at bornstein@u.northwestern.edu or gaby@u.northwestern.edu.

A large number of banks in this country are not willing to work with businesses in the cannabis industry, even when those sales are legal under state law. This is causing major difficulties for thousands of business owners that are forced to operate on a cash-basis. But are they the only ones to suffer? Using straightforward economic analysis we ask who is losing due to these restrictions. The short answer is – almost everyone. Not only businesses are being hurt, but also consumers. In addition, such restrictions also decrease the revenues of the government.

While it is not difficult to argue, as we do below, why restricted access to banking services is bad for the economy, quantifying the different costs is a complicated task. It requires rich data on the costs incurred by businesses together with modern econometric techniques. In the next few months, we plan on collecting the required data to tackle such task. We believe that quantifying these costs is both of scientific interest and of that of the legal cannabis industry. If you are in the legal cannabis industry and would like to get more information about our study, we encourage you to contact us! Our contact information is listed at the top of the page.

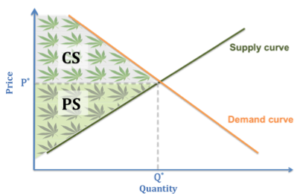

In economics, when we want to analyze the effects of a government policy on market participants (consumers and producers) a first and simple approach is to look at the changes in consumer surplus (CS) and producer surplus (PS). These two measures represent what consumers and producers win by participating in the market.

FIGURE 1

As reference, Figure 1 shows what market equilibrium, CS and PS would be in the market for marijuana products if everyone had access to banking. If we think of the market demand function as representing how much consumers benefit from each transacted quantity, CS can be computed as the shadowed area in Figure 1 below the demand curve. Similarly, if we think of the market supply function as representing how much it costs to sellers to produce each transacted quantity, PS is the shadowed area in Figure 1 above the supply function.

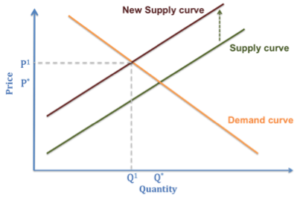

FIGURE 2

What is the effect of banking restrictions on market equilibrium, CS and PS? Not having access to banking implies that producers have to take additional measures in order to be able to sell: install ATMs, hire security companies, allocate extra time to counting and moving cash, etc. This means that for each quantity transacted, the cost of doing so is higher than before. For the sake of simplicity, let’s think that these extra costs can be measured in dollars and correspond to a linear cost of $T per unit. In this case, such increase would shift the market supply curve as shown in Figure 2. Market equilibrium would feature a higher price and lower quantity.

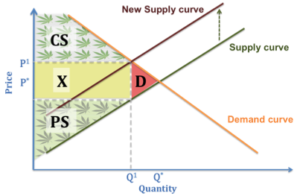

We can decompose the effect on CS and PS as shown in Figure 3. There are two factors that reduce both CS and PS. First, consumers and producers share the burden of the extra cost generated by the lack of access to banking, this is represented by area X in Figure 3 that reduces both surpluses. Second, since the quantity transacted is now lower than before, there is an irrecoverable loss for both consumers and producers represented by area D in figure 3.

FIGURE 3

What is the difference between areas X and D? Well, area X is not entirely a loss to society as a whole: it includes payments to security companies, so it is a transfer from one sector to another, but it also includes the cost of the extra time needed to process cash payments, which could be better allocated to leisure or working in something else. Area D, on the other hand, is entirely a loss to society: if the market had access to banking, costs would be lower and quantity transacted would be greater and at a lower equilibrium price. New consumers would be incorporated into the market, and existing consumers would pay less.

Gideon Bornstein and Gabriela Cugat are two economics PhD candidates from Northwestern University in Evanston, Illinois, who are studying the costs incurred by businesses transacting only with cash.

Follow NCIA

Newsletter

Facebook

Twitter

LinkedIn

Instagram

News & Resource Topics

–

This Just In

Member Blog: What Consumers Really Want in a Pre-Roll

Member Blog: The Evolving Cannabis Legal & Regulatory Landscape in 2026