Member Blog: Novel Foods Applications Stalled?

The UK CBD market had an estimated value of £300 million in 2020 and by the end of 2022 estimates had doubled that figure. This goes to show that CBD being deemed a “novel” food in January 2019 has had little impact on market growth and if predictions are right will exceed £1 billion by 2025. With the FSA’s March 2021 deadline long behind us and having made submissions by the deadline, many companies will be feeling comfortable. However, it’s worth remembering that the authorization process is still on-going, so while products that are part of a validated application are allowed to remain on the market they are still not authorized as novel foods. And now with the FSA conducting market research to aid in their risk assessment of consumer CBD products, some concerning data has been published.

The FSA commissioned Fera Science Ltd to carry out a survey to obtain a brief overview of current CBD products on sale in England and Wales in order to help FSA’s risk assessment of CBD products. The products selected covered, oils, sprays and edibles (including drinks). The study collected various data on the products. This included testing for CBD content, cannabinoid profiles, heavy metals, pesticides, residual solvents, Polycyclic Aromatic Hydrocarbons (PAHs) & mycotoxins. A summary of the results are shown below:

- Heavy metals (cadmium, mercury & lead) and arsenic were not detected in the majority of samples, meaning levels were below the limits of quantification of the method. Seven samples contained lead, four samples arsenic and two samples contained cadmium. Mercury was not found in any sample. A definitive statement as to whether products exceed maximum levels cannot be made due to uncertainty as to whether products would be classified as a food (i.e. oil) or a food supplement.

- A low incidence of low levels of mycotoxins, with Fusarium mycotoxins found more frequently than aflatoxins and ochratoxin A, mostly at the methods reporting limit. Three samples were found to contain ochratoxin A at the methods reporting limit.

- A total of seven pesticide residues were found across all of the products (each product was tested for over 400 pesticides). There are no specific Maximum Residue Limits (MRL) for CBD products.

- One oil product was found to have PAHs above the regulated levels, if classed as a product for direct consumption. If classed as a food supplement the PAHs were within regulated levels.

- Three samples contained residual solvents. One product was over the MRL.

- Most products contained CBD close to the declared value. Two oils had substantially different levels than that declared (one higher and one lower). CBD was not detected in one of the drink products. These are potentially non-compliant with compositional and standards requirements.

- Delta 9-THC was detected in 87 % (26) of the samples analysed. Of these 40% (12) were found to have THC+ (the total sum of illicit cannabinoids in the product) above the 1mg threshold.

Although Fera only tested a small number of products, the fact that such a large percentage of products were found to have issues is concerning to say the least. It throws into question how many other products currently on the market that are part of a validated NF application, but aren’t up to spec.

The next question is, are you 100% sure that your current market offerings meet their product specifications? If not then there’s no time like the present to take a closer look at your products and their manufacturing process. It’s also important to remember that if you do need to make changes then these changes need to be updated in your current regulatory filings.

If you would like to discuss this further, please reach out to us at info@arcuscompliance.com.

Committee Blog: Defining Legal Hemp – It Isn’t Always Simple Math

By: Todd Glider, Chief Business Development Officer, MobiusPay Inc.

Contributing Authors: Paul Dunford, Green Check Verified | Shawn Kruger, Avivatech | Kameron Richards, Kameron Richards Esq.

Produced by: NCIA’s Banking & Financial Services Committee

If you are a cannabis-related business, and are looking to accept credit cards, it is only possible to do so if you are selling a product that is defined as legal hemp by the 2018 Farm Bill.

The 2018 Farm Bill provides that:

“The term ‘hemp’ means the plant Cannabis sativa L. and any part of that plant, including the seeds thereof and all derivatives, extracts, cannabinoids, isomers, acids, salts, and salts of isomers, whether growing or not, with a delta-9 tetrahydrocannabinol concentration of not more than 0.3 percent on a dry weight basis.”

For the most part, it’s pretty cut-and-dry. Marijuana is a schedule 1 drug. Hemp is not. If your product has less than .3% Delta-9 on a dry weight basis, it’s not marijuana, it’s hemp. And since it’s hemp, it’s federally legal. And since it’s federally legal, it can be purchased with checks, credit cards, or debit cards. Hemp products are, reductively, as incendiary as a stick of butter.

Of course, there is the law and there is how acquiring banks—banks that offer merchant accounts—interpret the law. Across the U.S., there are hundreds of acquiring banks. Of those, only six or seven offer merchant accounts to hemp businesses.

That’s it, plus payment service provider Square.

The immediate problem for the few acquiring banks that have, laudably, said, “Yes,” to hemp is, “how do we distinguish products that are .3% Delta-9 or less (and therefore, yawningly legal) from those that are over .3% Delta-9 (and therefore, illegal as angel dust)?”

Enter the Certificate of Analysis, or COA, or lab report. While there is nothing in the law stating that COAs are required to prove that a product is within the federally legal limit, their role is sacrosanct during the boarding process. For every hemp-derived product, there must be a corresponding COA proving that the product being sold is hemp, and not marijuana.

Fortunately, there are labs across the nation. The U.S. Department of Agriculture website lists 85, as of May 2023. Manufacturers and businesses ship their samples to these labs. The labs run their tests and the COAs are issued.

Simple, right?

Not really.

There are no standards in place for these reports. No templates. Every laboratory’s COAs—while substantively providing the same information—look a little different. Furthermore, most bankers haven’t seen a lab report since high school chemistry, and you’ve got a recipe for confusion or misunderstanding (frequently both).

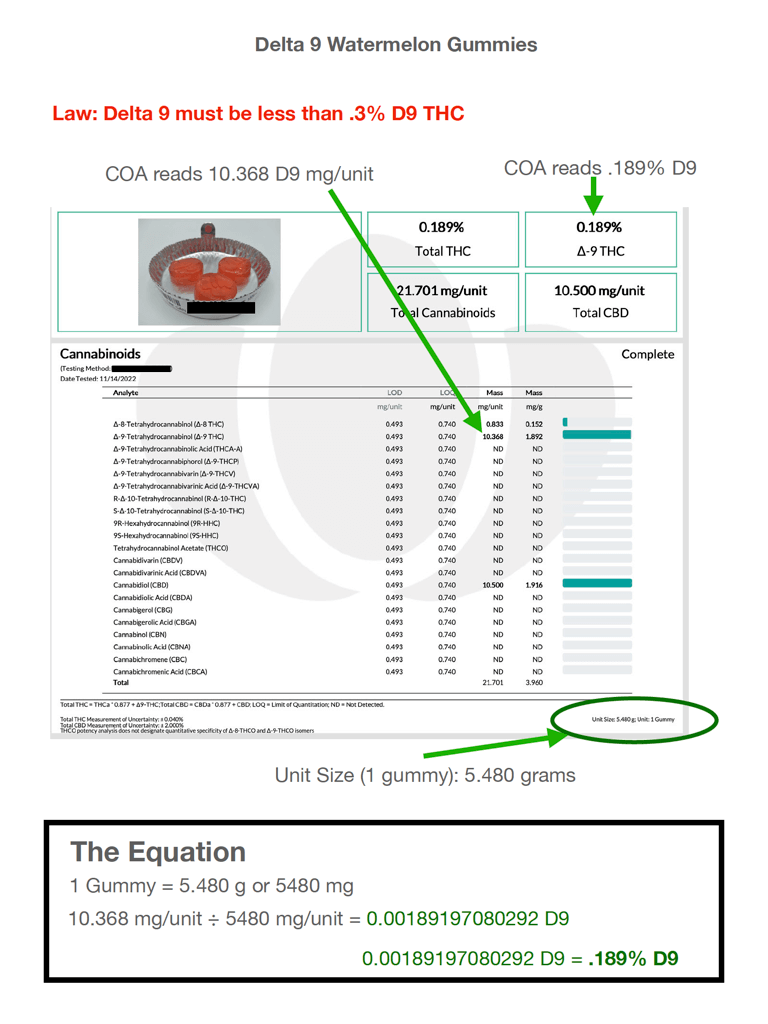

This COA, when it was initially presented to the bank, was rejected. To the underwriter, it was an open and shut case.

When the bank opened its door to offering acquiring to hemp businesses, its policy was to reject anything with greater than .3% Delta-9 by weight.

The top of this COA showed an instance of Delta 9 that read .189%. That passed muster, certainly. However, when he delved further into the analyte detail, he noted additional Delta-9 figures in excess of the .3% limit:

- 10.368 in the mg/unit cell

- 1.892 in the mg/g cell

It was not clear to the bank’s underwriter which of the two—per-unit or per-gram—corresponded with the by-weight percentage he was to be mindful of, but both were certainly over the .3% limit.

So, open and shut case: DECLINED

The salesperson that brought the merchant to this bank was surprised by the rejection. He hadn’t looked at the COAs very closely, but it seemed unlikely that this merchant had been selling products on her website that were in excess of .3% Delta-9.

Why? Because if the merchant had been selling products on its website in excess of .3% Delta-9, it would have been engaging in egregious felony drug trafficking. The salesperson doubted that was the case.

The salesperson did something he didn’t normally do: he took out his calculator.

He wanted to know why it read .189% Delta 9 at the top, but 10.368 in the analyte table. He noted the unit size at the bottom of the page was a gummy weighing 5.480g.

For the sake of simplicity, he multiplied that by 1000 to convert it to milligrams. That made it 5480 mg

Then he entered the onerous 10.368mg from the mg/unit figure in the analyte table and divided it by 5480mg. The resulting calculation netted the following total: .0018919.

Next, he converted it to a percent, and found that the result was .189%, which matched the figure at the top of the COA, exactly.

The next day, the salesperson presented the COA to the bank, with the markings and The Equation just as shown here.

It was an open and shut case: ACCEPTED

This situation is an example of why banks and credit unions unknowingly reject compliant hemp businesses from merchant processing solutions. As stated, a simple mathematical calculation was the difference between being accepted or rejected for necessary merchant processing services. Without proper merchant servicing not only are cannabis businesses’ profitability affected because they can only take cash; cash is also not as traceable or auditable as electronic transactions.

In general, businesses providing services to the cannabis industry are often challenged with disentangling legal risks with the benefits of their necessary services providing more transparency. With enhanced knowledge of the cannabis industry and its parameters, the cannabis industry will recognize a greater participation by all businesses necessary for the life of the industry thereby enhancing cannabis businesses’ likelihood to succeed but also enhancing the legitimacy and regulation of the industry.

Committee Blog: A Novel Cannabinoid Conundrum – Loopholes, Liability, and Legislation

by Matthew Johnson and Doug Esposito

by Matthew Johnson and Doug Esposito

members of NCIA’s Risk Management and Insurance Committee

For better or for worse, the cannabis industry is easily the most fascinating experiment in state regulation that this country has ever seen.

Rules vary widely from state to state.

Product testing requirements lack uniformity.

Packaging and labeling are a compliance nightmare.

State laws aren’t the only things that vary, though…

Product Liability definitions of what is even ‘covered’ by a cannabis insurance policy range widely between insurance companies. Now, a tidal wave of novel cannabinoid products threatens to upend the traditional American perception of cannabis – and possibly teach a few lackadaisical insurers an expensive lesson.

So, let’s delve into the issues associated with product liability and novel cannabinoids in the American cannabis industry…

American cannabis companies face a daunting task when it comes to navigating the complex and constantly evolving landscape of regulations governing the production, distribution, and sale of cannabis products. With 40 sets of rules governing different state markets, plus a handful of federally licensed businesses, ensuring compliance can seem like an insurmountable challenge.

One of the most significant issues facing cannabis companies is product liability, including the ongoing blight of product recalls. As with any consumer product, there is a risk of harm associated with the usage of cannabis products – things like adverse reactions, contamination, mislabeling, or improper dosage, to name a few. The legal and financial implications of product liability can be severe, including lawsuits, fines, and irreversible reputational damage. Given the complexity of the state-segregated cannabis supply chains and the lack of clear federal guidance, it is additionally challenging for companies to identify and mitigate potential risks.

Traditional cannabis companies must also contend with the emergence of novel cannabinoids. As researchers continue to explore the potential therapeutic benefits of cannabis, previously unknown cannabinoids are being discovered and brought into the mainstream. These compounds may have unique properties and potential therapeutic applications, but they also pose challenges in terms of safety and regulation. For example, some novel cannabinoids may be more potent or have different effects than traditional cannabinoids like THC and CBD. What’s worse, some novel cannabinoid products can even produce substances that are deleterious to human health (for example – the vaporization of THC-O Acetate produces toxic ketene gas).

The challenges associated with product liability and novel cannabinoids highlight the need for clear and consistent regulation of the cannabis and hemp industry. While some states have taken steps to create comprehensive regulatory frameworks for cannabis, the lack of federal guidance has created an incoherent patchwork of rules and regulations that can be difficult for even the most seasoned minds in compliance to navigate.

Without sensible and congruous regulations, companies may be forced to operate in a legal gray area, increasing the risk of non-compliance and potential harm to consumers. In fact, this is exactly what’s happening with the unregulated intoxicating cannabinoid market. A veritable alphabet soup of novel intoxicants like Delta-8 THC, THCP, THC-O Acetate, and others have sprung up to fill the gap in access perpetuated by the federal illegality of ‘normal’ marijuana products. Beyond that, some folks are synthesizing Delta-9 THC (the ‘normal’ THC molecule) from hemp and marketing it as if it were naturally occurring THC from marijuana.

These products are increasingly problematic for cannabis consumers. While intoxicating hemp-derived products are technically legal through a loophole in the Farm Bill, states have had to take action to ban or regulate novel cannabinoid products. The states that haven’t acted are effectively endorsing the sale of untested cannabis goods often derived from federally legal hemp. This means that novel cannabinoid products get a free pass in many areas for heavy metals, mycotoxins, pesticides, residual chemicals, and other contaminants that the regulated marijuana industry must monitor to maintain good standing with a state cannabis program.

As if varying state regulations weren’t enough, insurers’ definitions of what is considered ‘cannabis’ vary widely too. Some policy forms contemplate hemp-derived cannabinoids as ‘cannabis’ and some do not.

A few examples of policy wording are below:

Carrier A:

- “Medical Marijuana means cannabis or marijuana, including constituents of cannabis, THC, and other cannabinoids, as a physician-recommended form of medicine or herbal therapy”

Carrier B:

- Simple exclusion for ‘Hemp-Derived Intoxicating Cannabinoids’

Carrier C:

- “Cannabis” means:

- Any good or product that consists of or contains any amount of Tetrahydrocannabinol (THC) or any other cannabinoid, regardless of whether any such THC or cannabinoid is natural or synthetic.

- The paragraph above includes, but is not limited to, any of the following containing such THC or cannabinoid:

- (1) any plant of the genus Cannabis, or any part thereof, such as seeds, stems, flowers, stalks and roots; or

- (2) any compound, byproduct, extract, derivative, mixture or combination, such as, but not limited to:

- (a) Resin, oil or wax;

- (b) Hash or hemp; or

- (c) Infused liquid or edible marijuana;

- Whether or not derived from any plant or part of any plant set forth in the paragraph above.

From the get-go, you can infer a few things from these definitions/exclusions:

- Carrier A: not an adult-use cannabis company’s best choice as it only defines ‘medical marijuana.’ This could leave the door open for potentially uncovered claims from recreational products.

- Carrier B: insurance company is looking to protect itself from issues with the new wave of novel cannabinoid products – but specifically, only the dozen or so intoxicating cannabinoids that can legally be synthesized from hemp (without testing mandates in most states). An important takeaway is that this definition would cover non-intoxicating cannabinoids like CBN or CBC, even if they were derived from hemp.

- Carrier C: this language is/was commonly used across a number of insurance carriers who cover cannabis. Their policies may carry some restrictions, but this broad definition of cannabis includes synthetic cannabinoids and could expose the carrier to major lawsuits.

Those with broader definitions that include all cannabis-derived products often restrict their product liability coverage in other ways. All things considered, the industry has a long way to go until the available product liability coverage can truly be called comprehensive.

To address these challenges, policymakers, industry leaders, and consumers must work together to create a regulatory framework that protects public health and safety while supporting the growth of the cannabis industry. This should include clear guidelines for product labeling, testing, and dosing to ensure that consumers have access to safe and accurately labeled cannabis products. It should also include provisions for product recalls and liability to protect consumers in the event of unexpected quality control issues.

Additionally, the framework should support ongoing research into the therapeutic potential of cannabis, including novel cannabinoids. This research should be conducted in a manner that ensures the safety and efficacy of new compounds before they are introduced to the market. By creating a robust regulatory framework that balances innovation with consumer protection, we can ensure that the cannabis industry continues to grow and evolve in a responsible and sustainable manner.

As risk professionals in this field, it’s our duty to convey the urgency of these issues and the need for action. By working together to create a regulatory framework that supports both innovation and consumer protection, we can ensure that the cannabis industry continues to thrive while safeguarding public health and safety.

It’s time for policymakers, industry leaders, and consumers to come together to address these critical challenges and build a sustainable future for the American cannabis marketplace that is inclusive of all the various products that can be developed from cannabis.

Matt Johnson leads the Risk Services division for QuadScore, the nation’s leading cannabis insurer. Matt works to keep the cannabis industry safe from unexpected losses through all manner of risk mitigation techniques, ranging from facility security assessments to fire protection improvements.

Matt Johnson leads the Risk Services division for QuadScore, the nation’s leading cannabis insurer. Matt works to keep the cannabis industry safe from unexpected losses through all manner of risk mitigation techniques, ranging from facility security assessments to fire protection improvements.

Matt has the unique ability to study the claims activity for hundreds of cannabis operators across virtually every active state in the USA. Through this lens, he can offer unique insights into the most common claims and how to prevent them.

In addition to learning from past mistakes, Matt also keeps an eye on future claims drivers from emerging areas such as hemp-derived novel cannabinoids. Before starting with QuadScore, Matt spent a number of years working for a Berkshire Hathaway insurance company.

Doug Esposito has been a Property & Casualty Specialist with AssuredPartners and leads the firm’s Renewable Energy and Cannabis Practice with specific expertise in these industries. Doug’s current cannabis & hemp practice clients include indoor/outdoor cultivators, manufacturers, distribution companies, dispensaries, non-storefront delivery, labs and property owners, so he knows what challenges are facing the growing industry and is skilled at providing solutions. Doug is also one of AssuredPartner’s experts in alternative risk mechanisms including self-insured and captives programs.

Doug Esposito has been a Property & Casualty Specialist with AssuredPartners and leads the firm’s Renewable Energy and Cannabis Practice with specific expertise in these industries. Doug’s current cannabis & hemp practice clients include indoor/outdoor cultivators, manufacturers, distribution companies, dispensaries, non-storefront delivery, labs and property owners, so he knows what challenges are facing the growing industry and is skilled at providing solutions. Doug is also one of AssuredPartner’s experts in alternative risk mechanisms including self-insured and captives programs.

Doug currently serves as the Co-Chair of the California Cannabis Industry Associations’ (CCIA) Risk Management committee and serves on the National Cannabis Industry Associations’ (NCIA) Risk Management & Insurance Committee. He understands the importance and need to educate the insurance carriers and the public on the benefits of cannabis and hemp both medicinally and economically. “I truly respect the spirit of the industry’s medicinal origins and I’m committed to helping build this industry to reach new levels of growth, success, safety and acceptance,” shared Doug.

U.S. Federal Appeals Court Legalizes Delta-8 THC, Setting Precedent for the Cannabis Industry

By Sadaf Naushad, NCIA Intern

By Sadaf Naushad, NCIA Intern

Thanks to the Agricultural Improvement Act of 2018 (2018 Farm Bill), hemp is now federally legal, permitting U.S. farmers to cultivate, process, and sell hemp. Since its passing, however, businesses in the hemp industry have found themselves in a legal gray area.

With the 2018 Farm Bill eliminating restrictions on the psychoactive cannabinoid delta-8 THC, the companies deemed their delta-8 THC products within legal guidelines. Several jurisdictions disagreed, calling for clarification on the status of delta-8 THC.

Last week, the U.S. Court of Appeals for the Ninth Circuit addressed the dilemma, claiming delta-8 THC products as federally legal.

Let’s consider what delta-8 THC legalization means for the future of the cannabis industry.

Because recreational cannabis use remains federally illegal, delta-8 THC products continue to gain popularity nationwide. Manufacturing developments have led to enhanced consumer products, in which cultivators safely extract delta-8 THC cannabinoids from hemp plants.

While delta-9 THC constitutes a major psychoactive cannabinoid in the marijuana plant, delta-8 THC appears in trace amounts of the plant. Its psychoactive properties grant consumers gentler side effects compared to delta-9 THC.

On Thursday, a three-panel judge of the U.S. Court of Appeals published their opinion regarding delta-8 THC, ruling products containing the psychoactive ingredient as federally legal. According to the panel, delta-8 THC qualifies as a legal substance under the present federal definition of hemp. Federal law outlines hemp as “any part of” the cannabis plant, in which “all derivatives, extracts and cannabinoids” with less than 0.3% delta-9 THC by weight are allowed.

Had U.S. Congress unintentionally created a loophole leading to the legalization of delta-8 THC, the U.S. Federal Appeals Court stated that Congress should be responsible for resolving the issue. The panel specified that they would not replace its own judgment with Congress’ policy rulings. In the meantime, the Court defines the federal hemp law as “silent with regard to delta-8 THC.”

According to a Politico article, “Members of Congress have proposed fixes to federal hemp laws that would close this loophole. Rep. Chellie Pingree (D-Maine) introduced a bill in February to limit hemp and hemp products by calculating the total THC rather than focusing on Delta-9 THC. At the same time, state hemp regulators are voicing for a similar change advocating for the 1 percent total THC definition of hemp. Meanwhile, some states have moved to ban the sale of Delta-8 THC products or to regulate them similar to recreational marijuana.”

NCIA takes a strong position that Delta-8 products and any other psychoactive cannabinoids must be restricted to adults over 21 and regulated by the states so that these products are subject to the same testing requirements, track-and-trace rules, and excise taxes as other adult-use cannabis products.

Furthermore, if you are interested in learning more or getting involved with NCIA’s Government Relations work please contact Madeline Grant at madeline@thecannabisindustry.org to schedule a call. As the oldest and largest trade association, our Government Relations team has been hard at work for over a decade educating and working with congressional offices. NCIA held its Virtual VIP Lobby Days last week, May 16-19 on Capitol Hill. NCIA’s Evergreen members participated in congressional meetings all week long to advocate and educate members of Congress(s) and staff on the importance of cannabis policy reform. We discussed the importance of keeping the Secure and Fair Enforcement (SAFE) Banking in the America COMPETES Act and descheduling cannabis at the federal level. You can read more about cannabis and banking from last week’s blog HERE.

NCIA members were able to share their personal stories about being in the cannabis space and relay their expertise to further understanding of the struggles and hurdles cannabis businesses face every day. There is never a time more important than now to support NCIA’s efforts for cannabis policy reform.

Follow NCIA

Newsletter

Facebook

Twitter

LinkedIn

Instagram

News & Resource Topics

–

This Just In

Member Blog: The Evolving Cannabis Legal & Regulatory Landscape in 2026

How THCa Vapes Are Changing Consumer