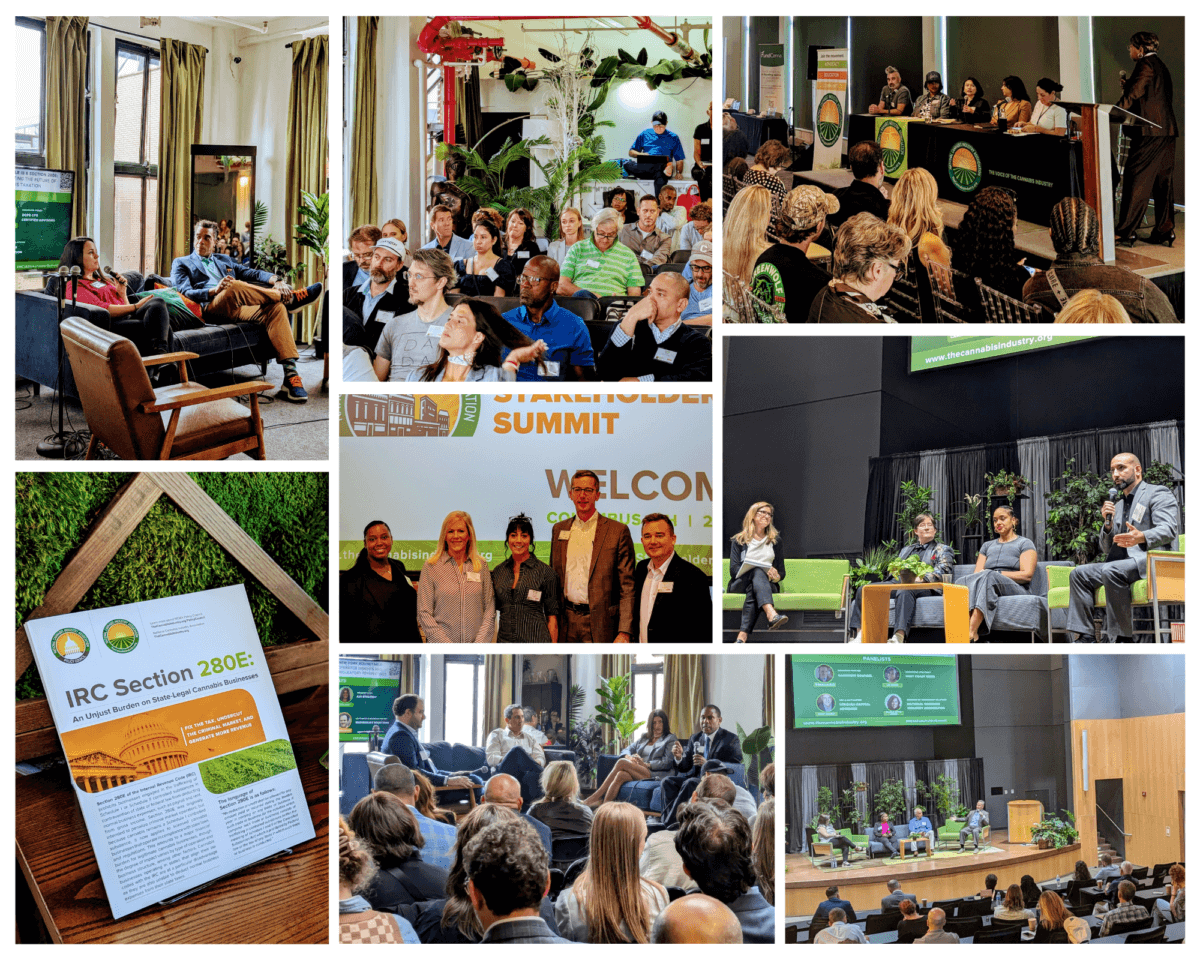

Be Part of a Movement, Not a Moment: Highlights from NCIA’s Fall Stakeholder Summits

This fall, the National Cannabis Industry Association (NCIA) held four Stakeholder Summits across the United States, gathering cannabis industry operators, regulators, investors, and advocates to tackle the unique regulatory, operational, and strategic challenges facing cannabis businesses today. Held in Michigan, New York, Ohio, and Southern California, these Summits offered actionable insights into the evolving landscape of cannabis regulation and taxation, fostering a spirit of collaboration and movement-building in support of a thriving, equitable industry.

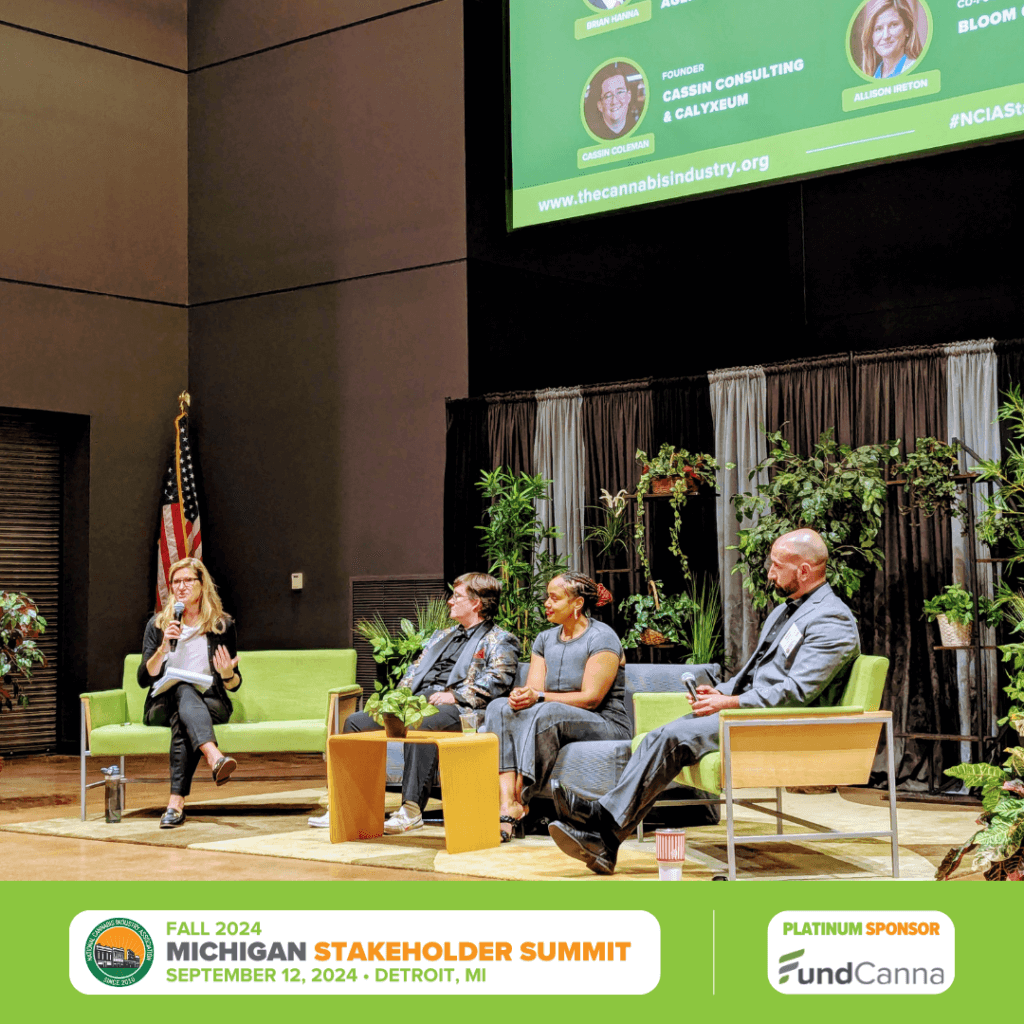

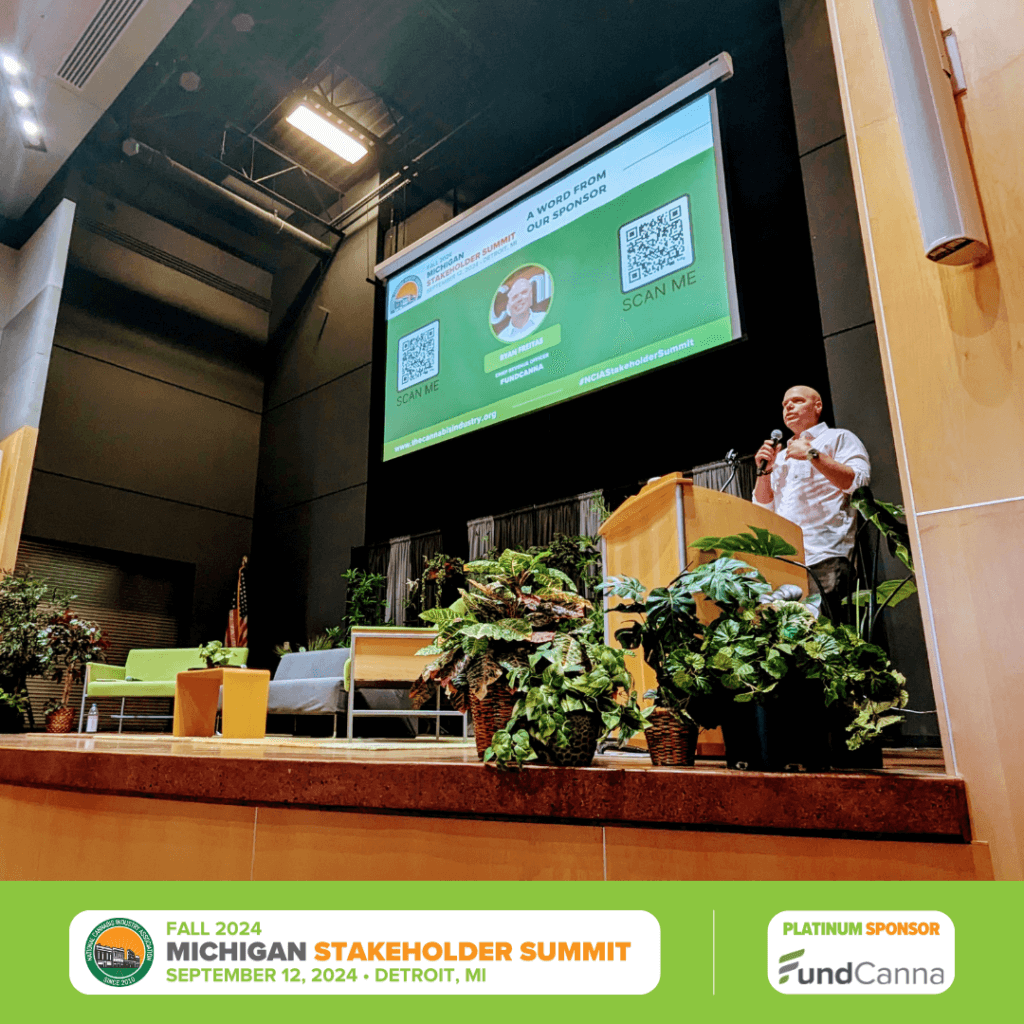

Michigan Stakeholder Summit: Regulatory Adaptation and Collaborative Solutions

The Michigan Stakeholder Summit brought to light the latest regulatory shifts impacting cannabis operators in the state. From changes in the Hemp Farm Bill to Michigan’s approach to intoxicating hemp sales, the panel on “Operator Insights and Regulatory Perspectives” shed light on pressing issues. Brian Hanna, Executive Director of the Cannabis Regulatory Agency, addressed upcoming regulatory changes and discussed the need for balanced enforcement to protect Michigan’s legal market. Discussions also covered navigating compliance with agencies like the Department of Environment, Great Lakes, and Energy (EGLE) and MIOSHA, while maintaining operational efficiency.

One core theme emerged from panelists such as Rebecca Collett of Calyxeum and Allison Ireton of Bloom City Club: collaboration is essential. As the Michigan cannabis market faces evolving dynamics, including the rapid issuance of new licenses and pressures on medical caregivers, the need for a transparent dialogue between regulators and industry stakeholders remains critical. Attendees left with actionable strategies for adapting to compliance requirements, maintaining business viability, and ensuring consumer protection.

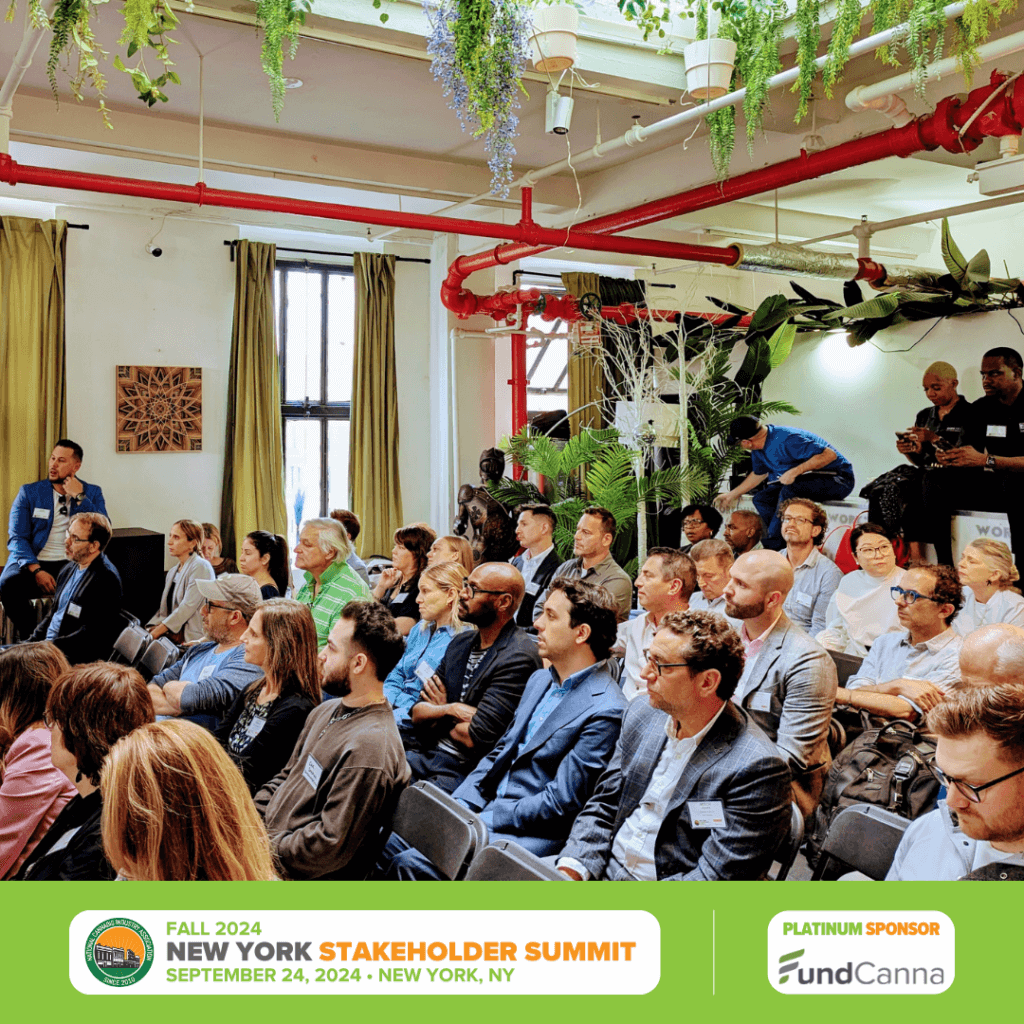

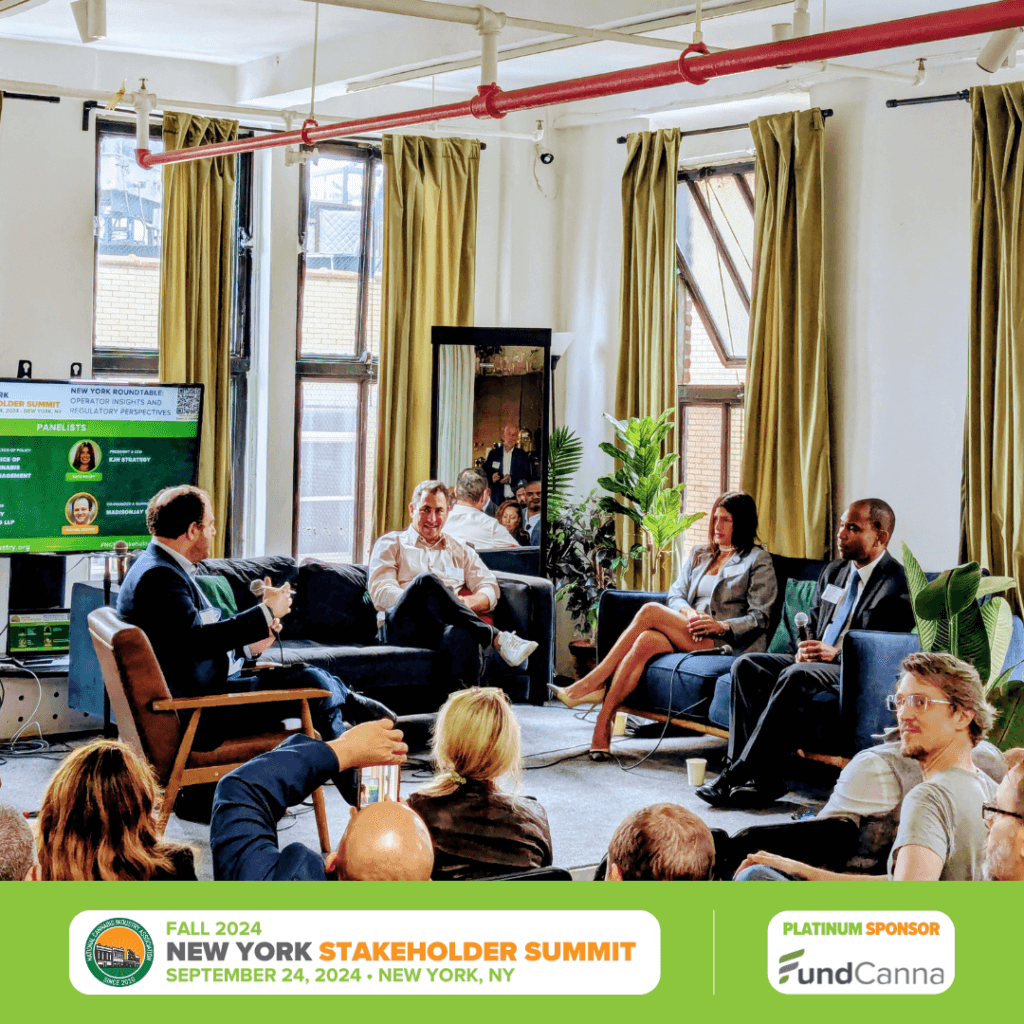

New York Stakeholder Summit: A Regulatory Landscape in Transition

In New York, the Stakeholder Summit focused on how operators can succeed in a rapidly maturing market. Led by John Kagia from the Office of Cannabis Management (OCM) and industry veterans like Jeffrey Schultz of Foley Hoag LLP, the “Operator Insights and Regulatory Perspectives” panel delved into the complexities of New York’s regulatory landscape. The session addressed social equity provisions, compliance hurdles, and strategies for growth in a highly regulated environment.

Key questions included navigating the intake process for new operators and the impact of recent enforcement actions on the illicit market. Kate Hruby of KJH Strategy emphasized the need for well-defined compliance guidelines to reduce ambiguity, while Marcella Osello of DOPE CFO Certified Advisors shared insights on the financial challenges facing small businesses in New York. The panel underscored the importance of partnerships between operators and policymakers, leaving attendees with insights on building a resilient business within a market in flux.

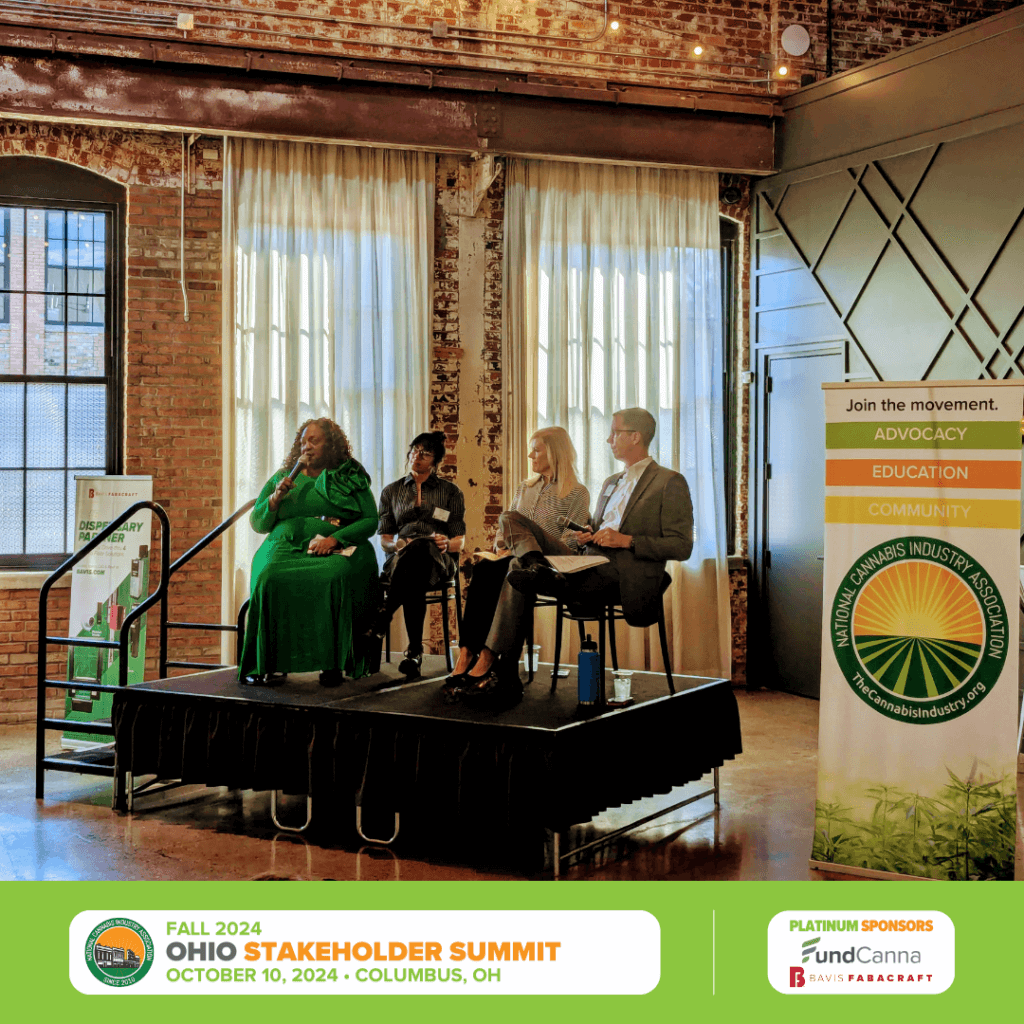

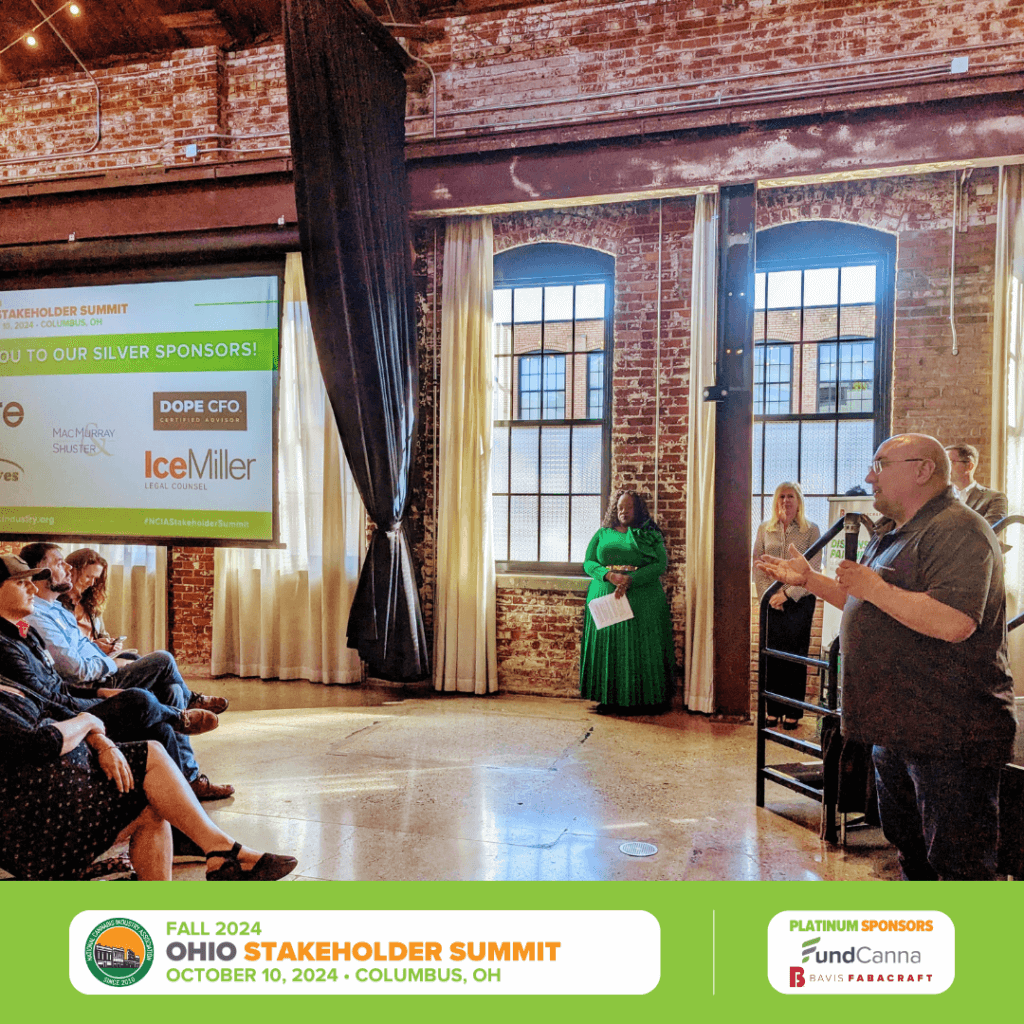

Ohio Stakeholder Summit: Legislative Updates and Strategic Business Growth

The Ohio Summit explored the convergence of legislation, legal complexities, and operational strategy essential for growth in Ohio’s cannabis market. Ohio State Representative Juanita Brent (D – District 22) shared updates on recent legislative actions affecting cannabis operators and emphasized the need for proactive policy advocacy, particularly as the legislative landscape shifts with changes in state leadership.

Legal experts like John Oberle of Ice Miller LLP and Helen Mac Murray of Mac Murray & Shuster LLP highlighted the nuances of Ohio’s regulatory requirements, with a focus on compliance around testing, product dosing, and advertising restrictions. Emillie Kelleher of BeneLeaves provided practical strategies for scaling a cannabis business within these parameters, underscoring the importance of understanding regulatory demands while fostering consumer trust. Ohio’s legislative season is critical for the cannabis industry, and the call to action was clear: advocate, educate, and ensure that the industry’s voice is heard as Ohio’s regulations continue to evolve.

Southern California Stakeholder Summit: Advancing Equity and Policy Innovation

In Los Angeles, top regulators, operators, and industry advocates gathered to explore the unique challenges and growth opportunities within the region’s cannabis market. Michelle Garakian, Executive Director of the Los Angeles Dept. of Cannabis Regulation, and Laura Magallanes, Deputy Chief of the Office of Cannabis Management for Los Angeles County, shared insights on compliance, while moderator Yvette McDowell guided a discussion on strengthening industry-regulator collaboration. Jazmin Aguiar, Emerging Markets Consultant for Council Member Imelda Padilla, contributed her expertise on market expansion and policy development, underscoring the importance of community engagement in regulatory planning.

Equity operator Kika Keith, founder of Gorilla RX Wellness, advocated for streamlined processes and resources to support equity businesses, while Jerred Kiloh, President of the United Cannabis Business Association, called for policy reform, including excise tax reduction, alongside stronger enforcement against illicit operators. Panelists encouraged attendees to engage in advocacy and build stronger partnerships with local agencies, presenting a path forward for a compliant, thriving, and equitable cannabis industry in Southern California.

Schedule III & Section 280E: Navigating the Future of Cannabis Taxation

Across all four Summits, the “Schedule III & Section 280E: Navigating the Future of Cannabis Taxation” panel served as a pivotal discussion into how the potential rescheduling of cannabis could reshape financial and regulatory landscapes. Featuring a diverse lineup of industry experts and regional operators from across the cannabis supply chain, the discussion highlighted the anticipated end of 280E limitations and its impact on tax planning, capital access, and broader market opportunities.

Each panel featured unique perspectives: in Michigan, Thomas Lavigne, Jay Snipes and Scott Greiper explored strategic financial planning for capital investment in a post-280E landscape and how operators could prepare for new deductible expenses. In New York, Al Foreman and Marcella Osello shared expertise on how rescheduling could influence capital markets and growth for smaller operators. In Ohio, Thomas Haren and Ashley Mosby emphasized proactive compliance and planning for tax relief, while in Southern California, Neil Rosenfield, Henry Wykowski, and Eric Kaufmann discussed the regulatory adjustments needed to fully benefit from Schedule III status, with a focus on operational scalability and tax strategy. Panelists across all locations encouraged operators to adopt forward-thinking approaches, aligning financial practices with both current and evolving regulatory environments.

Honoring Our Speakers: Driving Conversations That Shape the Cannabis Industry

The success of the Fall 2024 Stakeholder Summits would not have been possible without the expertise and passion of our distinguished speakers. These industry leaders, policymakers, and advocates generously shared their knowledge, providing actionable insights and fostering critical dialogue on the challenges and opportunities facing cannabis businesses today. We extend our heartfelt gratitude to each of them for their invaluable contributions.

Schedule III & Section 280E: Navigating the Future of Cannabis Taxation

Thank you to each of these exceptional speakers for advancing the conversations that define the future of our industry. Their insights and leadership continue to inspire progress and innovation across the cannabis landscape.

Thank You to Our Sponsors and Partners: A Driving Force Behind the Fall 2024 Stakeholder Summits

Platinum Sponsors

FundCanna and Bavis Fabacraft led the way as our Platinum Sponsors, opening each Summit with impactful contributions that set the stage for dynamic discussions and actionable takeaways. Their support was instrumental in creating events that inspired collaboration and innovation across all four Summits.

Together, these sponsors and partners exemplify the power of collaboration and the impact of collective action. Their support not only elevated the Fall 2024 Stakeholder Summits but also strengthened our shared mission to create a sustainable and equitable future for the cannabis industry.

Thank you for being an essential part of this movement and for helping us continue to inspire, advocate, and lead as we shape the future of cannabis.

Building a Movement for Change

The NCIA’s Stakeholder Summits brought together a diverse array of voices committed to the growth and integrity of the cannabis industry. From navigating complex compliance landscapes to advocating for inclusive regulatory frameworks, the message across each session was clear: this is a movement, not just a moment. Industry stakeholders must collaborate, advocate, and actively participate in shaping the future of cannabis in the United States.

For cannabis operators, now is the time to align with the NCIA’s mission, engage in industry advocacy, and contribute to a movement that transcends individual business interests. Together, we can forge a resilient industry that not only meets today’s challenges but also paves the way for a sustainable and equitable future.

The conversation continues in 2025 — NCIA will hold follow-up Stakeholder Summits in Sacramento and Denver in Q1 and Q2, culminating with our first-ever National Stakeholder Summit in May 2025. This event will coincide with our 13th Annual Cannabis Industry Lobby Days in Washington, D.C., where we’ll unite industry leaders to make an impact on the national stage.

Join the movement — Drive meaningful change and help define the cannabis industry for generations to come by becoming a member of NCIA. Learn more about membership here.

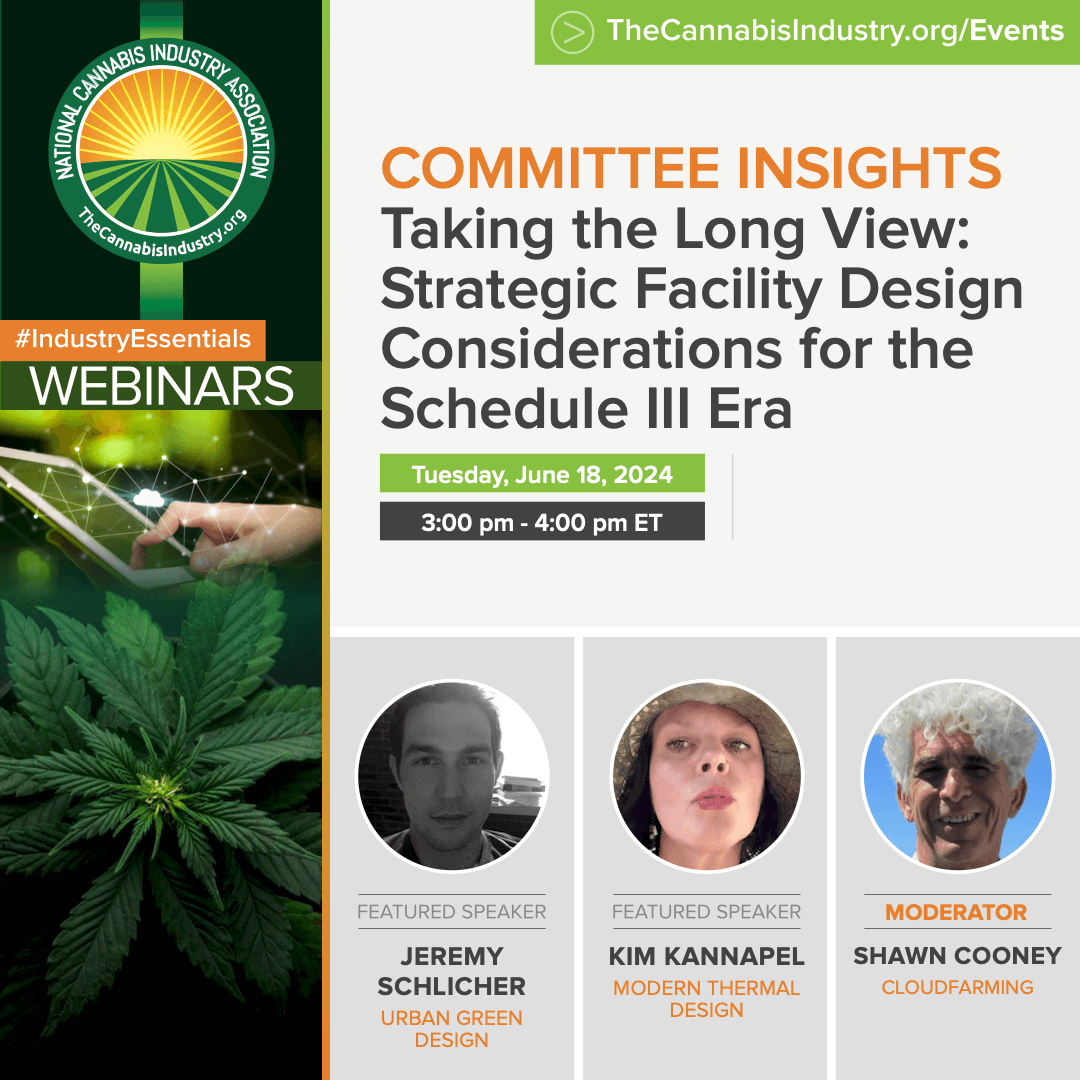

Taking the Long View – Strategic Facility Design Considerations for the Schedule III Era

In the dynamic landscape of the cannabis industry, regulatory changes can significantly impact how businesses operate and plan for growth. The recent proposal to reschedule cannabis from Schedule I to Schedule III has sparked discussions across the industry, particularly regarding facility design and operational strategies. This blog dives into key insights from the National Cannabis Industry Association’s webinar on “Taking the Long View – Strategic Facility Design Considerations for the Schedule III Era,” highlighting expert advice and practical recommendations for stakeholders navigating these changes.

The webinar, hosted by Brian Gilbert of the NCIA, served as a crucial platform for industry professionals to explore the implications of cannabis rescheduling on facility design and operations. The session focused on four main pillars: understanding tax changes, enhancing operational efficiency, promoting sustainable growth, and implementing practical strategies to navigate regulatory shifts.

Key Takeaways

1. Policy and Tax Implications

The discussion, led by Shawn Cooney of Cloud Farming, Chair of NCIA’s Facilities Design Committee, underscored the potential financial benefits for businesses following cannabis rescheduling (00:03:41). A highlight was the exploration of Section 280E, which could offer substantial tax savings once regulatory changes are implemented. Jeremy Schlicher of Urban Green Design expanded on these insights, offering strategic financial planning advice aimed at leveraging tax incentives to reinvest in facility improvements (00:07:21).

2. Operational Efficiency and Sustainability

Efficiency in energy management emerged as a critical theme throughout the webinar. Experts emphasized the importance of conducting energy audits and adopting efficient lighting and HVAC systems (00:10:18). These measures not only reduce operational costs but also align with sustainability goals crucial for long-term viability in the industry. Practical recommendations tailored to cultivation, manufacturing, and retail sectors were discussed to optimize workflow efficiencies and regulatory compliance (00:15:10).

3. Cultivation Methods and Environmental Considerations

Kim Kannapel of Modern Thermal Design provided invaluable insights into cultivation methods and environmental sustainability. The webinar highlighted the viability of various methods—indoor, greenhouse, and outdoor—each catering to different market segments and regulatory landscapes. The discussion underscored the role of climate and local regulations in shaping cultivation decisions (00:37:28), emphasizing the need for adaptable strategies that prioritize energy efficiency and environmental stewardship.

As Chair of NCIA’s Facility Design Committee, Shawn Cooney brought deep regulatory expertise to the discussion. He emphasized the importance of holistic sustainability practices and compliance with evolving regulatory frameworks. His insights into tax implications and strategic planning resonated with participants seeking clarity on financial strategies post-rescheduling (00:25:32).

Kim Kannapel’s contributions focused on environmental sustainability within cannabis cultivation. Her expertise in optimizing cultivation methods highlighted the interconnectedness of environmental stewardship and operational efficiency. By advocating for adaptive strategies, Kim encouraged businesses to consider long-term environmental impacts when designing and expanding their facilities (00:37:28).

A staunch advocate for the innovative triple bottom line approach, Jeremy Schlicher brings a wealth of knowledge to the discussion on strategic facility design in the cannabis industry. He emphasizes the integration of economic prosperity, environmental stewardship, and social responsibility in every aspect of facility planning and operations. Jeremy’s insights into maximizing operational efficiency through sustainable practices, such as energy audits and efficient HVAC systems, underscore his commitment to reducing environmental impact while enhancing business profitability.

Importance of Participating in the Public Comment Period

Participating in the public comment period is crucial for shaping the future regulatory landscape of the cannabis industry. The Department of Justice’s proposal to reschedule cannabis presents a unique opportunity for stakeholders to voice their perspectives and influence policy decisions. NCIA has launched a dedicated tool to streamline this process, making it easier for industry professionals to submit informed comments.Submit your comment here.

Recap of Episode I & II

Episode I: Understanding Section 280E and its Impact on Cannabis Businesses

In Episode I, the focus was on the financial and tax implications of rescheduling cannabis. Section 280E was a major topic, with discussions centered on how the rescheduling could lead to significant tax savings and the importance of strategic financial planning for businesses to maximize these benefits.

Episode II: Cannabis Rescheduling’s Impact on Research and Safety

Episode II delved into the implications of cannabis rescheduling on research and safety protocols. This session emphasized the potential for increased research opportunities and the necessity for businesses to stay ahead of regulatory changes to maintain compliance and ensure product safety.

Looking Ahead: Preview of Episodes 4 & 5

Episode IV: Navigating Insurance and Risk Management in the Schedule III Era

Join us for the fourth episode of NCIA’s multi-part #IndustryEssentials webinar series, “Navigating Insurance and Risk Management in the Schedule III Era,” led by our Risk Management & Insurance Committee. This session delves into the evolving landscape of cannabis insurance and risk management, highlighting the opportunities and challenges presented by the rescheduling of cannabis to Schedule III.

Date: Tuesday, July 9th, 2024 Time: 3:00 PM EST – 4:00 PM ET

Episode V: Cannabis Manufacturing in the Schedule III Era

Building on the insights from our first four episodes, join us for the fifth installment of NCIA’s #IndustryEssentials multi-part webinar series. This session, led by our expert Cannabis Manufacturing Committee, will focus on the profound impacts and implications of rescheduling cannabis on the manufacturing sector. As we navigate these unprecedented changes, our panel of industry leaders will provide critical insights and practical guidance to help your business adapt and thrive in this new landscape.

Advancing the Industry Together: NCIA’s Mission in Action

The overarching theme of this series is to equip cannabis industry stakeholders with the knowledge and strategies needed to navigate the complex landscape of regulatory changes. By understanding the financial, operational, and research implications of cannabis rescheduling, businesses can better position themselves for sustainable growth and success. Each episode builds on the previous one, creating a comprehensive resource for industry professionals to stay informed and proactive in their planning and operations.

The webinar “Taking the Long View – Strategic Facility Design Considerations for the Schedule III Era,” offered a comprehensive roadmap for stakeholders navigating regulatory changes in the cannabis industry. By addressing tax implications, promoting operational efficiency, and advocating for sustainable growth practices, the session equipped participants with actionable strategies to thrive amidst evolving regulatory landscapes.

Call to Action

As the industry continues to evolve, staying informed and proactive is crucial for cannabis businesses. Explore NCIA’s resources, including upcoming webinars and educational materials, to deepen your understanding of regulatory changes and strategic facility design considerations. Engage with industry peers and experts to share insights and best practices that drive sustainable growth and operational excellence.

For those not yet members, consider joining the National Cannabis Industry Association (NCIA) to unlock unmatched benefits, resources, and access. Membership provides exclusive opportunities to influence industry standards, gain regulatory insights, and network with industry leaders. Join NCIA today to leverage these benefits and stay ahead in the competitive cannabis market.

Start Making Sense: What Does Schedule III & Section 280E Mean for Me?

Rescheduling cannabis signifies a monumental shift for our industry, specifically presenting a potential pathway to alleviate the burdens imposed by Section 280E. In a new multi-part #IndustryEssentials webinar series, led by experts from our 14 member-led Committees, NCIA will provide a comprehensive analysis of the immediate and long-term impacts on different sectors within the cannabis industry.

In our debut session, led by the Banking & Financial Services Committee, we provided invaluable insights into the transformative implications of rescheduling cannabis to a Schedule III drug and its consequent impact on Section 280E of the Internal Revenue Code. In “Schedule III & Section 280E: What Does It Mean for Me?” broadcast LIVE on Thursday, May 30th, we explored the game-changing potential of this shift, offering actionable insights for businesses navigating the evolving regulatory environment.

Neil Rosenfield, CPA:Provided insights into the significance of comprehending and championing advocacy organizations to address regulatory hurdles.

Steven Gotsdiner, CPA: Illuminated accounting requirements tailored to cannabis businesses, drawing attention to the nuances across various states.

Eric Kaufman, COO: Shed light on the hurdles encountered by cannabis enterprises, while also elucidating the potential benefits stemming from regulatory changes.

Aaron Smith, NCIA: Emphasized the pivotal role of industry participation in policy reform endeavors, highlighting NCIA’s instrumental role.

Among the topics explored during the webinar was the profound impact of rescheduling cannabis on federal legality, state and local tax obligations, and the broader regulatory landscape. With cannabis poised to transition to Schedule III, businesses are poised to embrace newfound opportunities while confronting challenges inherent in navigating this regulatory terrain.

Neil Rosenfield of BakerTilly USA underscored the significance of contributing to and championing advocacy organizations to effectively address regulatory hurdles. Aaron Smith echoed this sentiment, emphasizing the pivotal role of industry participation in policy reform endeavors, highlighting NCIA’s instrumental role in spearheading these changes.

Another focal point of discussion revolved around the ramifications of rescheduling on tax obligations and deductions governed by Section 280E. The panelists provided invaluable insights into the implications for tax planning, including adjustments to tax bills, cash flows, and essential updates to accounting records and charts of accounts.

Steven Gotsdiner of HBK CPAs illuminated accounting requirements tailored to cannabis businesses, drawing attention to the nuances across various states. Eric Kaufman, COO of FundCanna, shed light on the hurdles encountered by cannabis enterprises, while also elucidating the potential benefits stemming from regulatory changes, such as managing surplus cash flows and preparing for shifts in interstate commerce.

Eric Kaufman explored whether rescheduling cannabis to Schedule III would reduce the cost of capital for operators and recommended strategies for deploying increased cash flows to scale and grow businesses effectively.

The webinar also delved into the anticipated timeline for these regulatory shifts, offering insights into potential implementation trajectories spanning from 2023 to 2025. Strategies for navigating diverse timelines and regulatory fluxes were discussed, equipping businesses with the tools needed to adapt and flourish in an ever-evolving landscape.

Thanks to the informed engagement of our audience members, a cornerstone of what makes our webinar series so valuable for members, the discussion touched on the definition of “Good Accounting Practices” and whether this includes Generally Accepted Accounting Principles (GAAP). The panelists also speculated on the possibility of new excise taxes replacing 280E and the potential impacts on federal protections like bankruptcy and IPOs.

As the program was extended in order to answer all of our audience questions, the session concluded with insights into how these regulatory changes might affect the CBD and hemp industries. The panelists emphasized the importance of staying informed and adapting to varying state-level requirements.

As the cannabis industry continues its evolution, proactive engagement with regulatory changes remains paramount for business success. The insights shared during NCIA’s #IndustryEssentials webinar series offer a compass to navigate the labyrinth of regulatory complexities and position businesses for enduring prosperity. By fostering active engagement and advocacy, cannabis enterprises can shape a regulatory landscape conducive to industry growth and development.

To continue facilitating these crucial dialogues amongst operators, regulators, and stakeholders, NCIA relies on the support of dedicated members like you. Join NCIA today to access exclusive resources, stay informed about the latest industry developments, and be part of a community committed to driving positive change in the cannabis industry.

Supporting advocacy efforts is integral to driving meaningful change in the cannabis industry. By becoming an NCIA member, you’re not just investing in your business’s success; you’re also supporting initiatives that shape the future of the industry. Together, we can amplify our collective voice and effect tangible change.

As we conclude this recap of our insightful session on Schedule III and Section 280E, we’re thrilled to announce the next episode in NCIA’s #IndustryEssentials multi-part webinar series: “Committee Insights: Advancing Cannabis Science: Research Opportunities and Challenges Post-Rescheduling.” Led by our esteemed Scientific Advisory Committee, this episode promises to explore the exciting realm of scientific research and consumer safety in the wake of cannabis rescheduling.

Join us for an engaging discussion with industry experts, gain valuable insights, and shape the future of cannabis science and consumer safety. Register now to reserve your spot and be part of the conversation!

Member Blog: Tax Court Decision for Harborside Health Center

The Tax Court’s recent decision in Harborside Health Center v. Commissioner is more bad news for the cannabis business community. The taxpayer, a prominent California dispensary, was assessed approximately an additional $30 million in tax by the IRS for the years 2007 to 2012, years in which Harborside had total revenue of approximately $102 million. Harborside lost, so it will have to pay that amount plus also pay another 20% of the tax owed in accuracy-related penalties – the Tax Court did not decide the penalty issue and left it for a later opinion. At this point, Harborside can either pay the tax (plus possibly penalties) or appeal to the Ninth Circuit Court of Appeals.

GROUNDS OF THE DECISION

The court decided against Harborside on every single argument made by its counsel. Three of the issues are straightforward:

The doctrine of res judicata didn’t apply, so the fact that a civil forfeiture case against Harborside had been dismissed with prejudice did not prevent the IRS from assessing a tax liability.

The language in Section 280E of the Tax Code that deductions are disallowed to a trade or business that “consists of trafficking in controlled substances” applies to businesses that have more than the one activity of trafficking. Harborside argued that “consists of” means the business must ONLY be trafficking for the disallowance to apply, and the Tax Court rejected that interpretation.

Harborside had only one trade or business so it could not deduct any expenses related to a separate trade or business. The taxpayer had argued it had multiple lines of business, but the opinion held that Harborside didn’t make significant profits from any of the other claimed lines of business so there was only one business.

MOST IMPORTANT CONSEQUENCE OF DECISION

The holding in the case that has the widest applicability to the cannabis community regards what Harborside may include in its cost of goods sold. The increase in tax owed by Harborside mostly comes from reclassifying expenses from cost of goods sold to ordinary business expenses and then denying deductions for those expenses under Tax Code Section 280E.

The taxpayer argued that the broader cost of goods sold rules under Code Section 263A applied in addition to the earlier (and narrower) definition of cost of goods sold under Section 471 However, the Tax Court endorsed the reasoning in IRS Chief Counsel Advice Memorandum 201504011 (2015) regarding the interaction of Section 263A and Section 471 with respect to cannabis-related cost of goods sold calculations. It is the IRS view that a clause of Section 263A prevents allocating indirect cannabis-related costs into cost of goods sold because the deduction for those costs would be denied under Section 280E.

Harborside contended that the Sixteenth Amendment to the Constitution compels using Section 263A rules in addition to the Section 471 cost of goods sold rules. The Tax Court was very dismissive of the argument, pointing out that “Section 471 wasn’t found unconstitutional during the many decades when it was the only means of calculating COGS [cost of goods sold], and it wouldn’t be unconstitutional now if Congress repealed Section 263A.”

It is also worth noting that the Tax Court held that Harborside was a reseller, not a producer, and that producers are subject to a different set of regulations under Section 471 that allow additional expenses to be included in cost of goods sold.

WHAT NOW?

Harborside is important because it is the first Tax Court case to squarely address the interaction between Sections 263A and 471 in the context of a cannabis business. However, there are other courts that can hear federal tax cases besides the Tax Court, and there are other arguments that can be made besides the one made by taxpayer’s counsel (even in Tax Court). While the best option for relief for cannabis taxpayers is to change the law, even if the law is changed, there will still be years of audits under the current law, so the questions raised by the Harborside decision will continue to be litigated. For further discussion, please see our blog on our website.

James B. Mann is a partner with the Tax practice group of Greenspoon Marder LLP. Mr. Mann has over 25 years of experience serving as a trusted advisor to a broad range of stakeholders in the energy and financial services industries. He counsels clients on the new changes in the tax law, as well as cannabis tax issues and cannabis tax controversy proceedings. Mr. Mann has a law degree from Harvard Law School and an MBA from Columbia University.

Rachel Gillette is among the first attorneys in the nation to dedicate her practice to the cannabis industry. Since 2010, Ms. Gillette has helped marijuana/cannabis businesses with licensing and regulatory compliance, business law and transactions, contract drafting and review, tax litigation, corporate formation, and tax matters, including audit representation. She works with startups and entrepreneurs, investors, and ancillary industry businesses to help develop the cannabis innovation ecosystem, and is a zealous advocate for the industry.

Ms. Gillette regularly represents clients before the IRS’s Examinations, Appeals, and Collections Divisions, including marijuana businesses facing the challenges of IRS adjustments under 280E. She has successfully protested local, state and federal tax deficiencies on behalf of her clients, having prevented hundreds of thousands of dollars in incorrectly assessed taxes, interest, and penalties. She can assist individual and business taxpayers in 280E proposed assessments, offers in compromise, audit examinations, innocent spouse claims, sales, use, and employment tax matters, trust fund tax penalty assessments, penalty abatement’s, and levy releases.

For several years, Ms. Gillette was the executive director of the Colorado state chapter of NORML, the National Organization to Reform Marijuana Laws. She was a founding member of Women Grow and the National Cannabis Bar Association. She an advocate as well as an attorney, and is committed to helping change laws – and perceptions – relating to cannabis and ensuring state licensed and legal marijuana businesses are fairly taxed and regulated.

Ms. Gillette received her Juris Doctorate from the Quinnipiac University School of Law in Hamden, Connecticut, where she served as Associate Editor of the Quinnipiac University Probate Law Journal. During law school, she interned with the New Haven Public Defender’s office, where she developed her commitment to advocacy for those facing the many challenges of the criminal justice system.

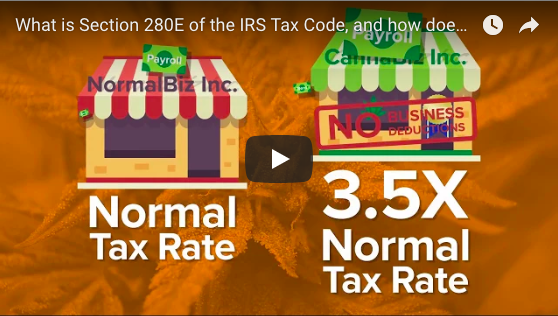

VIDEO: How Section 280E of the IRS Tax Code Burdens the Cannabis Industry

As tax season officially concludes, many cannabis businesses are feeling the burden of Section 280E, which can have the effect of taxing direct-to-plant businesses at a rate up to 3.5 times higher than other businesses. This unfair provision in the federal tax code affects the entire industry’s growth potential.

Watch this video below to learn more about Section 280E. Find out more about the solution: The Small Business Tax Equity Act which would allow for the fair and equal treatment of cannabis businesses.

Guest Post: Tax Time – Using an LLC To Minimize Section 280E Selling Costs

Although there are many legal considerations when choosing the right type of legal entity for your business, one consideration that is often overlooked is Section 280E. Corporations, including S corporations, are required to pay reasonable salaries to owners and officers working in the business. By “reasonable” in this context we mean a certain minimum salary amount. This requirement is due to Social Security tax issues that are beyond the scope of this article. The point is that owners must draw a salary and if that owner is involved in selling, marketing and/or delivery, then these salaries are subject to disallowance under 280E.

IS A LIMITED LIABILITY COMPANY RIGHT FOR MY BUSINESS?

A Limited Liability Company is different in this regard. There is no requirement to pay a salary to the business owner who works the business. Instead the net profit of the business is the income reported by the owner. (This applies to both single-member LLCs as well as to multi-member LLCs that are taxed like partnerships.) When owners report net income rather than salary, then they have no salary expense to be disallowed under Section 280E.

CONSULT YOUR CPA

Note that this benefit does not have to be limited only to the founder-LLC member. It is possible, with proper advice and planning, to create an LLC structure whereby all of the workers get treated as LLC members. Such a structure could substantially reduce your 280E expenses and give you the competitive advantage you need to succeed.

Want to learn how to navigate the complex tax & legal landscape of the growing cannabis industry? Join us for NCIA’s first Cannabis Tax And Law Symposium on January 21-22, 2015 in San Diego, CA, offering CPE and/or MCLE credits to attorneys or accountants that attend to learn more about these important topics! Register today.

Luigi Zamarra, CPA, has been a member of NCIA since 2013. Luigi CPA is an accounting firm located in Oakland, CA, that helps all types of businesses and individuals with tax planning, tax compliance, and tax dispute services. Luigi specializes in the medical marijuana industry. He helps these businesses comply with IRC Section 280E so as to balance tax cost against audit examination risk.

*Disclaimer: NCIA does not provide legal or financial services or advice. Any views or opinions presented in this guest blog post are solely those of the author and do not necessarily represent those of the organization. You must not rely on the legal information on our website as an alternative to legal or financial advice from your lawyer or other professional services provider.

James B. Mann is a partner with the Tax practice group of Greenspoon Marder LLP. Mr. Mann has over 25 years of experience serving as a trusted advisor to a broad range of stakeholders in the energy and financial services industries. He counsels clients on the new changes in the tax law, as well as cannabis tax issues and cannabis tax controversy proceedings. Mr. Mann has a law degree from Harvard Law School and an MBA from Columbia University.

James B. Mann is a partner with the Tax practice group of Greenspoon Marder LLP. Mr. Mann has over 25 years of experience serving as a trusted advisor to a broad range of stakeholders in the energy and financial services industries. He counsels clients on the new changes in the tax law, as well as cannabis tax issues and cannabis tax controversy proceedings. Mr. Mann has a law degree from Harvard Law School and an MBA from Columbia University. Ms. Gillette regularly represents clients before the IRS’s Examinations, Appeals, and Collections Divisions, including marijuana businesses facing the challenges of IRS adjustments under 280E. She has successfully protested local, state and federal tax deficiencies on behalf of her clients, having prevented hundreds of thousands of dollars in incorrectly assessed taxes, interest, and penalties. She can assist individual and business taxpayers in 280E proposed assessments, offers in compromise, audit examinations, innocent spouse claims, sales, use, and employment tax matters, trust fund tax penalty assessments, penalty abatement’s, and levy releases.

Ms. Gillette regularly represents clients before the IRS’s Examinations, Appeals, and Collections Divisions, including marijuana businesses facing the challenges of IRS adjustments under 280E. She has successfully protested local, state and federal tax deficiencies on behalf of her clients, having prevented hundreds of thousands of dollars in incorrectly assessed taxes, interest, and penalties. She can assist individual and business taxpayers in 280E proposed assessments, offers in compromise, audit examinations, innocent spouse claims, sales, use, and employment tax matters, trust fund tax penalty assessments, penalty abatement’s, and levy releases.

Follow NCIA

Newsletter

Facebook

Twitter

LinkedIn

Instagram

News & Resource Topics

–

This Just In

NCIA Applauds Reintroduction of SAFE Banking Following Lobby Days

Beyond Rescheduling: Inside NCIA’s 14th Annual National Cannabis Industry Lobby Days