Cannabis Rescheduling Explained: What We Know, What We Don’t, and What’s Next

Last week, President Trump made history when he signed an executive order (EO) directing the Attorney General to expedite the process of reclassifying cannabis to Schedule III and removing barriers to research to “increase medical marijuana and CBD research to better inform patients and doctors.”

There’s no disputing that this is a game-changing moment for the cannabis industry and how the plant is viewed writ-large, but there’s still many questions and unknowns. Let’s take a look at some of the most frequently asked questions I’m getting about what’s next and what it all means:

What Did the Cannabis Rescheduling Executive Order Actually Say?

The EO directs the Attorney General to expedite completion of the process of rescheduling marijuana to Schedule III of the Controlled Substance Act (CSA). It also directs the White House Deputy Chief of Staff for Legislative, Political, and Public Affairs to work with the Congress to allow Americans to benefit from access to appropriate full-spectrum CBD products while still restricting the sale of products that pose serious health risks. Additionally, the EO directs the Department of Health and Human Services (HHS) to develop research methods and models utilizing real-world evidence to improve access to hemp-derived cannabinoid products in accordance with Federal law and to inform standards of care.

When Will Cannabis Rescheduling to Schedule III Take Effect?

What This Means for 280E Relief and Cannabis Businesses

The truth is, we really don’t know. There is no deadline, and we know that it will be at least30 days due to the Administrative Procedure Act (APA). As of publication, the Attorney General has not filed any type of final rule and neither the DEA nor the DOJ has responded to the public comments that were received on the proposed rule in 2024.

We also have to consider litigation that will surely be filed by our opponents. For instance, Smart Approaches to Marijuana (commonly known as Project SAM) had already stated that they plan to file against the Administration (likely on procedural grounds).

The APA establishes the framework for judicial review of agency actions and while the APA itself does not specify a statute of limitations for general review, the default period for a civil action against the United States is generally six years after the claim first accrues, however, specific statutes for judicial review of certain agency actions may impose shorter deadlines, sometimes requiring a petition to be filed within 30 days after the final agency action.

In short, we have to wait and see (frustrating, I know!).

How Cannabis Rescheduling to Schedule III Affects Banking

A move to Schedule III does not solve the cannabis industry’s banking problems completely. Such a move would/will likely result in lower perceived legal risk for banks, more compliance comfort, expanded access to traditional services, and possibly even improve capital markets access; but it would/will not provide safe harbor for cannabis businesses or automatically change FinCEN guidance. That’s why it’s more important now than ever that we continue to advocate for the introduction and passage of bills like the SAFER Banking Act and the CLAIM Act.

NCIA’s Position on Cannabis Rescheduling to Schedule III

NCIA supports President Trump’s decision to officially direct the Attorney General to reclassify cannabis as a Schedule III substance. Medical professionals, patients, and millions of Americans have long understood that cannabis has accepted medical use and does not belong in the same category as the most dangerous controlled substances. By taking this step, the Administration is recognizing the realities of today’s regulated markets and the work states have done to responsibly oversee them.

That said, Schedule III cannot be the final word. NCIA urges policymakers to build on today’s decision by establishing a framework that respects states’ rights, supports responsible operators, and provides clear federal enforcement guidelines in order to provide certainty to the thousands of businesses operating openly and in compliance with state law. NCIA will continue working to ensure that this industry can thrive under policies that are fair, consistent, and reflective of modern realities.

After more than half a century of prohibition, the importance of this moment cannot be understated- but our association knows that this is just the beginning of a new day for cannabis. As we close out the year, NCIA is thankful to our members for their support and urges those of you who aren’t members to join today or make a donation. Together, we’ll continue to move this industry forward and ensure that progress continues in Washington, DC and beyond.

Wishing you and yours a wonderful holiday season and happy new year!

Rooted in Community: Fox Rothschild

At the core of NCIA is a dynamic network of business owners, advocates, industry professionals, and entrepreneurs all working towards a shared mission – cultivating a fair, inclusive, and thriving cannabis industry. Our “Rooted in Community” series highlights the members who strengthen and shape that vision every day. This month, we’re proud to spotlight Evergreen MemberFox Rothschild, a premier legal leader in the cannabis community, uniting more than 1,000 attorneys from coast to coast. The firm delivers the expansive reach and robust resources of a national practice while maintaining the personalized service and deep relationships typically found in a boutique firm.

NCIA: What problem does Fox Rothschild help solve in the market?

Fox Rothschild: The cannabis industry operates amid a web of complex, and often conflicting, state and federal laws that are difficult for businesses to navigate. That is where we come in. Our firm regularly advises cannabis operators, investors, and businesses on the full spectrum of legal issues – from licensing and regulatory compliance to corporate transactions, real estate taxes and employment matters. By combining deep industry knowledge with practical legal strategy, we help clients minimize risk, stay ahead of regulatory shifts and seize new opportunities in a rapidly evolving market.

NCIA: How is Fox Rothschild different from competitors in this space?

FR: Ranked by Chambers USA as a Band 1 law firm for Cannabis Law, our attorneys advise cannabis clients across the country on how to navigate a complex web of state and federal laws involving corporate formation, financing, banking, compliance, intellectual property, tax, employment and real estate. But what really sets us apart is our approach: we invest the time to get to know our clients and understand their needs so we can better develop creative strategies that drive results. Bottomline, we find ways to help cannabis businesses navigate this fast-changing, highly regulated industry with confidence.

FR: We joined the National Cannabis Industry Association (NCIA) almost a decade ago because we wanted to be at the center of the conversations shaping the industry’s future. Many of our clients and the companies we care about are active members in the NCIA and value the association’s role in advancing thoughtful policy, responsible growth and collaboration across the cannabis sector. By actively engaging with NCIA, our team gains valuable insights into the evolving regulatory and business landscape, allowing us to better anticipate challenges, identify opportunities and provide informed, strategic counsel. Being part of this community keeps us connected to real-world issues impacting operators and investors. It also reinforces our shared commitment to supporting a sustainable and equitable cannabis industry.

NCIA: Why is membership important to you?

FR: Our NCIA membership is invaluable. It allows us to stay connected to the people and issues driving this rapidly evolving industry. NCIA provides a unique forum where industry leaders, advocates and professionals can exchange ideas and address shared challenges. Through NCIA’s resources, network and events, we learn how to better support our clients and contribute to a more transparent, responsible and sustainable cannabis marketplace.

NCIA: Tell us about a relationship your membership has helped build?

FR: Fox Rothschild was proud to represent the NCIA pro-bono in December 2024 at a landmark hearing on the DEA’s proposal to reclassify marijuana as a Schedule III drug. Our liaison, Michelle Rutter Friberg, NCIA’s Director of Government Relations, was our boots-on-the-ground resource during the (now adjourned) hearing. Her knowledge and track record proved invaluable for us, and we continue to appreciate her insights.

NCIA: How has Fox Rothschild evolved since it started?

FR: We were among the first national law firms to launch a dedicated Cannabis Law Practice, positioning our team as trailblazers in this rapidly evolving industry. Over time, the practice has grown to include other leading attorneys in the Cannabis Law space, including some who are now at the forefront of efforts to reschedule cannabis. Fox attorneys now serve clients in every jurisdiction that has legalized medical or recreational cannabis, including California, New York and Pennsylvania. Our evolution mirrors the growth of the industry – innovative, strategic, and results driven.

Longstanding members like Fox Rothschild are the heart of NCIA’s community. A community grounded in the belief that the cannabis industry will become a robust and essential part of the national economy. We envision an industry that is fairly taxed, responsibly regulated, and readily accessible to the patients who rely on it most. Thank you, Fox Rothschild, for being truly Rooted in the Community!

Together with our members, NCIA is building a stronger cannabis industry – rooted in community and driven by shared purpose. Join the community, join NCIA.

How to Make the Most Out of Lobby Days

Dr. Amanda Reiman in conversation with Jeremy Marsh, from the Office of Congresswoman Dina Titus

NCIA’s 13th annual Cannabis Industry Lobby Days is rapidly approaching and new and seasoned attendees alike may be wondering how to make the most out of the precious time with electeds’ offices. Meeting with allies and skeptics both present unique challenges and opportunities. To provide advice on how to make the most out of Lobby Days, I reached out to Congresswoman Dina Titus’ office and spoke with Legislative Assistant Jeremy Marsh. Following his advice will help you walk away from Lobby Days feeling accomplished and confident that your message got through.

Stories from the community matter

White papers and data points are fine, but what really moves the needle are stories from the community and the front lines. Tailoring stories to the district/state of the office you are meeting with shows how constituents and local businesses are impacted by policy. These stories are great tools for supportive legislators to take to the floor and their committees. And, when meeting with a legislative office that has supported cannabis in the past, be sure to thank them! Standing up for cannabis is still a risk and those willing to take it should be acknowledged.

Rescheduling and hemp are still areas of confusion

Elected officials are more cannabis savvy now than ever before, but there are still some issues where education is needed. Don’t assume that elected officials, even supporters of cannabis are experts in all of the hot button issues being discussed in the industry. Mr. Marsh explains that rescheduling/descheduling and hemp regulation are two areas where confusion persists. Explain the issue before asking for support, and have some fact sheets ready with background information, as well be willing to answer questions and give context to these issues. Be sure you yourself can clearly explain the issues you are bringing into your Lobby Days visits.

Be early and be flexible

If you’re early you’re on time, if you’re on time, you’re late. This adage was drilled into my head by my Dad (thanks Dad!) and it is a great rule of thumb for Lobby Days. Try to be at least 5 minutes early to each meeting. Time is precious and being early shows that you are taking the process seriously. It also gives you time to collect your thoughts and your breath before heading into a meeting. Lines to get into the Capitol can be long, so keep this in mind before your first meeting of the day. If you are going to be late to a meeting, call the office and let them know. At the same time, be flexible. Schedules are constantly shifting for elected officials, so don’t take it personally if you are meeting with a staffer, or in the hallway outside the office. ALL communication is important, and many vital conversations happen outside the office doors (just watch Veep!).

The economy and public safety are selling points for opponents

Many would argue that meeting with opponents is just as, if not more, valuable than meeting with allies. And although cannabis has gained support from both sides of the aisle over the years, many are still skeptical of changing the laws around cannabis. If you meet with someone who has not traditionally been supportive, discussing the economic and public safety benefits of legalization is a good focus. Cannabis tax revenue has been used to support schools, roads, substance abuse programs, job placement and more. And, research shows that, after legalization, fewer teens are using cannabis, and fewer people are using opiates. You don’t have to be a fan of cannabis to be a fan of legalization.

NCIA’s 13th annual Cannabis Industry Lobby Days is a chance to bring the cannabis issue front and center with lawmakers. Once a source of snickers and jokes, the cannabis movement has become a major political force. Even so, assumptions about those involved in cannabis persist. Being prepared, professional and well versed on the issues will make an impression. And being a part of shedding a positive light on this industry and the people who work in it feels really great.

NCIA’s Statement on Interlocutory Appeal in Federal Cannabis Rescheduling Hearing

The historic hearing scheduled to examine how marijuana is classified under federal law that could have potentially moved it into Schedule III of the Controlled Substances Act has been postponed indefinitely.

The DEA’s Chief Administrative Law Judge (ALJ) Mulrooney recently granted a request for leave to file an interlocutory appeal, resulting in the cancellation of the merit-based hearing and effectively pausing the proceedings for at least three months. With a new administration being sworn in imminently and a new DEA Administrator who has yet to be selected, future action remains uncertain.

The movants (Village Farms International, Hemp for Victory, Office of the Cannabis Ombudsman of Connecticut, et. al.) behind the request were Designated Participants (DPs) without standing who purport to be pro-rescheduling, despite the fact that their motion will require operators to continue paying the exorbitant tax rates that 280E imposes and has galvanized prohibitionists. The interlocutory appeal was filed in an attempt to remove the DEA as the proponent of the rescheduling rule due to evidence the agency was biased against cannabis and had engaged in communications with prohibitionist group Project SAM and other opponents outside of the legal process.

While we agree that the DEA was unsurprisingly not free from bias, NCIA did not subscribe to this strategy because removing the DEA from its own administrative court was never a viable option and would have only resulted in delay or perhaps the end of the rescheduling process.

As the only pro-cannabis party granted standing in these proceedings, we are very disappointed in this unfortunate turn of events initiated by parties without legal standing.

“We believe this to be an ill-conceived strategy that benefits no one but the prohibitionists seeking to hinder reform,” said NCIA CEO & Co-founder Aaron Smith. “Our members need rescheduling and tax relief now, and we remain committed to advancing these reforms through whatever means available in the weeks and months ahead.”

This development underscores the importance of NCIA’s ongoing work advocating for the cannabis industry in Congress and the new administration. It will be up to the next DEA Administrator to determine the future of cannabis scheduling and NCIA will be working hard to ensure getting the process back on track is a priority.

Our pro bono legal teams at Greenbridge Corporate Counsel and Fox Rothschild are exploring every avenue possible to get the proceedings back on track and ensure meaningful progress continues.

NCIA Only Pro-Cannabis Organization Granted Standing in DEA Rescheduling Proceedings

On November 19, the DEA’s Chief Administrative Law Judge John Mulrooney issued a ruling granting the National Cannabis Industry Association (NCIA) full standing to participate in the upcoming hearings on the agency’s proposed rule to reclassify marijuana from Schedule I to III in the federal Controlled Substances Act.

NCIA was the only party granted standing that supports rescheduling, while all 12 parties in opposition to the proposed change were given the nod to move forward. We are proud to be able to represent the cannabis industry in these important proceedings, which could yield a groundbreaking outcome for the legal cannabis industry should our efforts prove successful.

The hearing will officially commence on January 21, 2025 and conclude during the first week of March. The Administrative Law Judge (ALJ) presiding over the proceedings has stipulated that each Designated Participant (DP) may present one witness that can testify for 90 minutes maximum. According to the schedule outlined by the ALJ, NCIA’s witness will testify on January 29.

NCIA unequivocally supports descheduling marijuana entirely, however, we recognize that the federal government is currently only considering rescheduling. As such, our organization is in favor of a move to Schedule III, but filed a “limited objection” to the proposed rule that focuses mainly on how the DEA could use this opportunity to make currently unscheduled cannabinoids Schedule I (or III).

Quotes from the Judge on NCIA’s limited objection: “cleverly put”, called it “a fine bit of lawyering“, and opined that it was “good to read something so thoughtful“. Our organization would like to highlight the work of policy co-chairs Khurshid Khoja and Michael Cooper, as well as the team at Fox Rothschild for spearheading our crafty argument!

These hearings are the final phase of a process to review and reclassify cannabis that was set in motion by President Biden in October 2022. NCIA has advocated for the legal cannabis industry throughout this process, strongly supporting the move to Schedule III as a critical first step toward ultimately making cannabis legal at the federal level.

Moving cannabis to Schedule III would not only be the first federal acknowledgment of the medicinal value of cannabis, it would eliminate the unjust burden of Tax Code Section 280E on the cannabis industry, allowing all businesses in the sector to take the ordinary business deductions afforded to other industries.

Currently, plant-touching cannabis businesses are collectively overpaying the IRS more than $2 billion annually in excess taxes. This stifles profitability and drives up costs across the entire industry—for licensees and ancillary businesses alike. So there is a lot at stake in the upcoming hearings and NCIA is up to the task of representing the industry and bringing home a big win for regulated cannabis.

I invite anyone interested in a favorable outcome to join our efforts by becoming a member of NCIA now so that we have the resources we need to make the best possible case for the cannabis industry in these proceedings. There are also opportunities for business leaders to pull up a seat at the table and provide input to NCIA during this important process, set up a call with someone on our team to learn more.

NCIA Members United in D.C. at Lobby Days! Join Us Next Year!

Photo By CannabisCamera.com

by Michelle Rutter Friberg, NCIA’s Deputy Director of Government Relations

Essentially every industry and association with a presence in Washington, D.C. hosts their own lobby days, advocacy days, or fly-ins – whatever you want to call them – where their members come to the Capitol to lobby Congress on their respective industry and legislative issues.

Thanks to NCIA, the cannabis industry is no different. In fact, just a few weeks ago, more than 100 members of the National Cannabis Industry Association (NCIA) descended upon Capitol Hill for NCIA’s 11th Annual Cannabis Industry Association Lobby Days. Lobby Days are an opportunity to advocate for our industry and tell Capitol Hill staff about the real, lived, on-the-ground experiences that cannabis professionals experience daily.

Planning 150+ meetings over the course of two days with 100+ attendees and 21 teams is about as easy as it sounds. That’s not to mention the multiple events, a congressional briefing, and training sessions! But that’s exactly what the NCIA team does for our members every spring. At lobby days, NCIA members gather to amplify our message and make their voices heard in the halls of Congress, while simultaneously forging strong relationships with the most influential leaders in the cannabis industry.

With more than 80 freshman members in Congress this session and multiple bills that have yet to be reintroduced, we wanted to focus our efforts on educating new members about the issues the cannabis industry – and the people that comprise it – face regularly. Many of these members and their staff have never heard of 280E, haven’t had to vote on SAFE Banking (yet!), and are on the fence about legalization, while others have never even talked with a cannabis professional. As a result, it was incredibly important to us that we reach out to those offices and provide them with the resources they need to best inform their position on the various policy areas that cannabis touches.

After arriving in D.C., attendees were greeted with a tropical vibe at our welcome reception at Tiki TnT & Potomac Distilling Company. This gave teams an opportunity to meet up ahead of meetings and mingle with other professionals who made the trip. The next day, we all gathered bright and (very) early for our mandatory breakfast training ahead of shuttling to the Capitol grounds for our group photo. At the training, attendees were able to grab a quick bite to eat, drink some coffee, get together with their teams, and get the final “do’s and don’ts” for their meetings. After our training and group photo, our teams split off for their meetings and reconvened at the end of the day for our stunning closing reception. There, attendees debriefed after an incredibly productive day and unwound with beautiful views, some drinks, and a dreamy jazz band. On the final day, attendees began their morning with a Senate briefing focused on SAFE Banking, where they rubbed elbows with congressional staff. Post-briefing, teams broke off for their final meetings, and just like that, lobby days 2023 was a wrap!

It’s no secret that the cannabis industry is undergoing significant struggles and we’re feeling that squeeze in Washington, D.C. Many companies have downsized and laid off government relations professionals, while others continue to just hope that Congress will pass reform magically. The truth is that lobbying, advocating, and being active in the legislative process are critical to moving our industry forward. Stay tuned for other citizen lobbying opportunities, and take it to the next level by sponsoring NCIA’s 12th Annual Cannabis Industry Lobby Days in 2024!

The legal cannabis industry is growing at an unprecedented rate, with more and more states legalizing its use for medical and recreational purposes. However, despite this progress, cannabis businesses face a major obstacle: Section 280E of the Internal Revenue Code. This provision is a significant burden on cannabis businesses, limiting their ability to take deductions for basic expenses like rent, utilities, and employee salaries. The result is a higher tax burden and reduced profitability, putting cannabis businesses at a disadvantage compared to other industries.

Section 280E was introduced in the 1980s as a way to prevent drug dealers from taking business deductions on their tax returns. At the time, the provision was aimed primarily at illegal drug dealers. However, when it comes to cannabis businesses, Section 280E has become a significant hurdle. The problem is that while cannabis is legal for medical or recreational use in many states, it remains a Schedule I drug at the federal level. This means that cannabis businesses are still subject to the same limitations as illegal drug dealers when it comes to tax deductions.

The impact of Section 280E on cannabis businesses is significant. Without the ability to deduct basic expenses, cannabis businesses face higher tax burdens and reduced profitability. This makes it difficult for them to reinvest in their operations and grow their businesses. In addition, the provision makes it challenging for cannabis businesses to obtain financing, as many traditional lenders are hesitant to work with them due to the regulatory environment and the industry’s status as a Schedule I drug.

The insurance industry plays a vital role in supporting the cannabis industry. With the help of insurance professionals, cannabis businesses can protect their assets, mitigate risks, and navigate the complex regulatory environment. However, insurance providers also face challenges in the cannabis industry due to the regulatory environment and the industry’s status as a Schedule I drug. For example, some insurance companies are hesitant to provide coverage to cannabis businesses due to concerns about federal prosecution.

Despite these challenges, there are insurance providers that specialize in the cannabis industry and offer tailored solutions to cannabis businesses. By working with these providers, cannabis businesses can protect their assets and minimize risks, while also demonstrating to potential investors and lenders that they are taking the necessary steps to manage their risks.

In addition to the insurance industry, there are other steps that policymakers can take to support the cannabis industry. Revising Section 280E is one of the most critical steps that can be taken. By allowing cannabis businesses to take more deductions on their tax returns, policymakers can help level the playing field and create a more equitable regulatory environment for the industry. This would enable cannabis businesses to reinvest in their operations, grow their businesses, and create jobs.

One could say that 280E could be equally or more importantly about de-scheduling cannabis than about changing a tax code. This a vital step that policymakers can take to remove cannabis from the list of Schedule I drugs. The current classification of cannabis as a Schedule I drug is outdated and based on outdated stereotypes. This is also contributing to a massive roadblock with the potential to destroy many businesses in the legal market, which only helps the illicit market thrive. Removing it from the list of Schedule I drugs would enable researchers to study cannabis more effectively and provide a clearer understanding of its medical benefits and potential risks. It would also allow cannabis businesses to operate more freely and obtain financing from traditional lenders.

Creating a more supportive regulatory environment for the cannabis industry is critical to its success.

With the help of insurance professionals, tailored solutions, and supportive policymakers, the cannabis industry can continue to grow and contribute to the economy. Revising Section 280E and removing cannabis from the list of Schedule I drugs are essential steps that can be taken to support this critical industry.

Valerie has over 16 years of experience in the insurance industry with specialized niches in cannabis, real estate, and community associations. With experience working for companies such as McDermott Costa Insurance Brokers, AmWINS Group, Inc., Commercial Coverage Ins. Agency, and Colemont Insurance Brokers, Valerie has developed a love of helping clients navigate the world of insurance by creating an understanding of the value behind insuring their business. In addition to her professional work, Valerie serves as the CREW East Bay Chair on the Programs Committee, is a National Cannabis Bar Association member, NCIA member, and volunteers in East Bay communities with Richmond Grows Seed Lending Library to show people how to save vegetable seeds and grow their own food. In 2021, Valerie received the 2021 and 2022 CREW East Bay Connections Award and was a nominee for the Elevate 2021 Industry Impact award.

With a drive and passion for helping people, Valerie has gone back to her long-standing roots in the plant medicine industry and uses her unique lens of growing up surrounded by cultivators and sellers to validate her client’s business needs. Valerie strives to break the mold of how insurance and cannabis has partnered together to give back to the community she grew up in. With a strong insurance background and an in-depth knowledge of the cannabis industry, Valerie has been a trusted advisor for over 70 cannabis clients.

For more information on Liberty’s National Cannabis Practice Group, please reach out toValerie Taylor, Vice President (National Cannabis Practice Leader), The Liberty Company Insurance Brokers.

Long-Awaited Cannabis Bills Introduced

Photo By CannabisCamera.com

by Michelle Rutter Friberg, NCIA’s Deputy Director of Government Relations

Over the last few weeks, a number of cannabis bills were introduced in Congress: the long-anticipated SAFE Banking Act and the CLAIM Act were reintroduced in both chambers, while over in the House, the HOPE Act and 280E legislation dropped. Keep reading to find out more about these bills and the chances of them moving forward:

Finally… SAFE Banking

After the SAFE Banking Act failed to pass into law last session, advocates have been waiting with bated breath for the legislation’s reintroduction – with a particular interest in what changes may (or may not have) been made.

In the Senate, the bill is being led again by Sen. Jeff Merkley (D-OR) and Sen. Steve Daines (R-MT), while the House version is being spearheaded by Rep. Earl Blumenauer (D-OR) and Rep. Dave Joyce (R-OH) – both of whom are chairs of the Congressional Cannabis Caucus.

While the bill does not contain wide-ranging revisions, there were some changes. These changes include adding language to explicitly apply the bill’s protections to community development financial institutions (CDFIs) and minority depository institutions (MDIs), as well as ensuring that workers and operators in the cannabis industry are able to obtain federally backed mortgage loans. In response to concerns raised by some conservatives, this version also includes changes and clarifications intended to ensure that federal law enforcement agencies are able to fully enforce anti-money laundering statutes against unlawful operators.

NCIA is optimistic that the legislation will receive either a hearing or markup in the coming weeks and looks forward to this bill finally passing the Senate someday soon!

HOPE Act

Also recently reintroduced was the Harnessing Opportunity by Pursuing Expungement (HOPE) Act. First introduced last session, the bill was just dropped by Rep. Alexandria Ocasio-Cortez (D-NY) and Rep. Dave Joyce (R-OH).

This bipartisan bill aims to help states with expunging cannabis offenses by reducing the financial and administrative burden of such efforts through federal grants. The overwhelming majority of cannabis-related charges are handled by state and local law enforcement and despite the fact that expungement programs for cannabis-related offenses have recently advanced in states and cities around the country, many criminal record-keeping systems are not ready for or able to support these efforts.

The HOPE Act would address these complications by creating a new grant program under the U.S. Department of Justice, which would be authorized to make grants to states and local governments to reduce the financial and administrative burden of expunging convictions for cannabis offenses that are available to individuals who have been convicted of such offenses under the laws of the State.

CLAIM Act

Yet another bicameral, bipartisan piece of legislation was recently reintroduced: the Clarifying Laws Around Insurance of Marijuana (CLAIM) Act. Introduced in the House by Reps. Nydia Velazquez (D-NY) and Warren Davidson (R-OH) and in the Senate by Sens. Bob Menendez (D-NJ) and Rand Paul (R-KY), the legislation would protect insurers, brokers, and agents from being penalized by federal regulators for providing insurance services to state-licensed marijuana companies.

Assuming that the SAFE Banking Act moves through “regular order” as expected, I would predict that many of the protections in the CLAIM Act get attached to SAFE. This is the third Congress that the CLAIM Act has been introduced.

Small Business Tax Equity Act

Everyone involved in the cannabis industry has heard of 280E, but many people were surprised to learn that legislation addressing the punitive measure was not introduced during the last congressional session.

That changed a few weeks ago when Congressman Earl Blumenauer (D-OR), along with four of his colleagues introduced H.R. 2643: the Small Business Tax Equity Act, which exempts a trade or business that conducts cannabis sales in compliance with state law from IRC Section 280E.

Abolishing 280E is one of NCIA’s main priorities, but unfortunately, the chances of this legislation passing standalone is little to none. We will continue to explore other vehicles which 280E reform may be attached to and seek to provide any tax relief we can to the legal cannabis industry.

The last few weeks have been a whirlwind of activity here in D.C. – and we don’t plan on slowing down ahead of NCIA’s 11th Annual Cannabis Industry Lobby Days being held on May 16-18! Register today so that you’re a part of our virtual training sessions and we can begin planning your lobbying experience.

Video: NCIA Today – Thursday, April 20, 2023

It’s the 4/20 Cannabis Industry Update!

Join NCIA Director of Communication Bethany Moore for an update on what’s going on with NCIA and our members.

A Unified Cannabis Industry Voice in Washington

Photo By CannabisCamera.com

by Michelle Rutter Friberg, NCIA’s Deputy Director of Government Relations

When I first started at NCIA nearly nine years ago, there were a lot less people lobbying for cannabis reform on Capitol Hill. As our industry has grown and expanded, so has the government relations presence in D.C., but that also means that unification and coordination has become more difficult. New trade organizations have been created, individual companies with competing interests have hired their own lobbying firms – it’s a lot to keep track of! As a result, one of the things we’ve heard most from Capitol Hill staffers is that a unified voice would be incredibly helpful when trying to get legislation over the finish line.

So, NCIA got to work to make that happen, convening a working group comprised of the trade organizations in the cannabis space we work closely with on the Hill. In the following weeks, we sent a unified industry letter on SAFE Banking and hosted a briefing and reception for freshman members and staff on Capitol Hill.

Industry Letter

On March 21, NCIA, along with the National Cannabis Roundtable (NCR), United States Cannabis Council (USCC), Minority Cannabis Business Association (MCBA), and National Hispanic Cannabis Council (NHCC) sent a letter to Senate Banking Committee Chairman Sherrod Brown (D-OH) and Ranking Member Tim Scott (R-SC) calling on them to act to address the continued lack of equitable access to banking and capital for cannabis related businesses and expeditiously take action on the bipartisan SAFE Banking Act upon its reintroduction. You can read the full text of the letter here.

Just a day later, the American Bankers Association (ABA) Washington Summit was held. Chairman Brown said, “Prognosis is positive… I’m hopeful we can do it [SAFE Banking] relatively soon.” Ranking Member Scott also spoke about the importance of moving the bill forward through “regular order” while reiterating that he doesn’t necessarily support the legislation himself. Scott, who is running for president in 2024, also said that cannabis reform broadly is, “something that we’re going to have to wrestle with as a nation and as a Congress and get to an answer there.”

Looks like the Senators agree with our letter!

Freshman Briefing and Reception

As lobbyists, one of our biggest jobs is educating members of Congress and their staff about the issues facing our industry and how to address them. That can be difficult, however, there’s 535 members of Congress and a lot of staff turnover (not to mention elections every two years!).

To combat this, NCIA, NCR, USCC, and the American Trade Association for Cannabis and Hemp (ATACH) came together to host a briefing on Cannabis 101 for freshman members of Congress and their staff. This is the first time that all of the major trade organizations have come together to host an event like this and it was incredibly well received. Former Colorado Senator Cory Gardner (R) even said to me personally how remarkable the coalition was!

The briefing included messages from all four members of the Congressional Cannabis Caucus, panels on “Incremental Approaches & Comprehensive Reform” and “Current Operational Landscape Potential & Challenges” as well as a fireside chat between Rep. Troy Carter (D-LA) and Sen. Gardner.

Following the briefing, a reception was held in Rayburn Cafeteria where more than 100 Hill staffers and lobbyists mingled to discuss all things cannabis. All of the feedback we received was overwhelmingly positive, with questions about when the next event would be! I made sure to remind everyone that NCIA’s 11th Annual Cannabis Industry Lobby Days would be taking place May 16-18, and that we look forward to visiting their offices and educating them further.

You won’t want to miss this event – register today and sign up for our newsletter to make sure you continue to get all of the latest information and updates about how to get involved with our work in Washington!

Come Meet Congress – 11th Annual Cannabis Industry Lobby Days

by Madeline Grant, NCIA’s Government Relations Manager

Will you join us as a united front in Washington, D.C. this year?

Hundreds of cannabis industry professionals from all over the country will descend on Capitol Hill this month for the 11th year for NCIA’s Annual Lobby Days. It’s more important than ever before to make your voice heard and advocate for the federal reforms our industry needs to truly thrive.

Whether it’s access to banking for your business, much-needed federal tax reforms, or some of the many other struggles faced by our industry that could be remedied by congressional action, we need you to tell your stories on Capitol Hill with us on May 16-18.

Here’s our top four reasons for you to register today to join us for this exciting and impactful event this year:

New members of Congress

Last November, we saw midterm elections bring in a new class of freshman members of Congress. Many of these new faces replaced the old guard of those with long-standing prohibitionist views toward cannabis. Many of them lean more progressive, which means they are more likely to be friendly toward our issues. This infusion of new blood, new minds, and new perspectives in the halls of Congress can work in our favor.

NCIA’s Lobby Days is the best way to get direct access to some of these offices so we can get off on the right foot with them on our issues. Joining us in D.C. means you will inform and educate these new members of Congress on the struggles we face like tax reform, veterans’ medical access, social equity, and of course, the SAFE Banking Act specifically. How many new co-signers can we get on this bill? Let’s find out together.

Discuss incremental and comprehensive reform

With new members of Congress come new staffers that need to be educated on cannabis policy reform. In an environment where there are hundreds of issues, it’s important we reach every Hill office. When we descend on Capitol Hill, NCIA members will have the ability to discuss their personal stories in the cannabis space. The government relations team is constantly on Capitol Hill meeting with offices; however, hearing directly from businesses is something special.

As we are at the beginning of the 118th Congress, cannabis legislation will continue to be introduced and this is our opportunity to get members of Congress on board. It’s all about baby steps; as we educate congressional offices they now have the ability to reach out to NCIA for resources and information. Over the past ten lobby days, NCIA sees a significant increase in co-sponsorship for cannabis legislation.

When we go into meetings the government relations team will provide talking points covering incremental reform; such as SAFE banking and 280E reform. Further, we have the opportunity to gather intel regarding their view on comprehensive reform. We’ve seen bills, such as the Cannabis Administration and Opportunity Act and the States Reform Act. Although these bills have not had any legislative success, it’s important for Hill offices to understand the importance of state and federal conflict for the cannabis industry.

Meeting 200+ other politically active industry professionals

It’s not a conference — it’s different. There’s no expo floor or panel discussions, just people. And it happens to be some of the most politically engaged leaders of our industry who attend Lobby Days. You’ll rub shoulders and team up with cannabis industry pioneers who have been in the game for years. You’ll learn the “ins and outs” of the Beltway from lobby day veterans who join us every year to advocate for our industry. Hear about it for yourself by watching this re-cap video from last year’s 10th Annual Lobby Days:

Learn how to lobby and take those lessons home

This isn’t our first rodeo, but it might be yours, and that’s okay. Even if you’ve never done citizen lobbying before, NCIA’s government relations team makes it easy by offering training before the event, as well as on-site. We’ll give you materials to help you tell your stories including descriptions of our priority legislation, and background information on the offices you’ll be speaking with. And you won’t have to go it alone! We will team you up with a small group of your fellow cannabis industry peers to navigate the halls of Congress together.

Lobby Days with NCIA will empower you to go back to your home state to advocate on the industry’s behalf. You’ll know what to say, how to say it, and what to expect.

Together, we can make a real difference and push our industry past the tipping point. Hundreds of NCIA members have already registered for this event, so what are you waiting for? Register today, schedule your flight, and book your hotel. We can’t wait to see you there.

Managing finances and complying with complex regulations in the highly regulated cannabis market can be challenging for business owners. For this reason, it’s crucial to have a competent cannabis accountant. In this article, we will discuss four major reasons why a good accountant is essential in the cannabis market, grouped into distinct categories.

Mitigate the risk

Having specialized professionals, such as a cannabis accountant, can bring a wealth of knowledge and expertise to your business. They understand the unique challenges and regulations associated with the cannabis industry and can provide guidance and support to help you make informed decisions and navigate potential risks. By leveraging their expertise, you can ensure the success and stability of your business in this rapidly evolving industry.

Accountant who has experience working in volatile and new industries is well-equipped to handle the risks that come with operating in such environments. By regularly identifying and measuring these risks, the accountant can help mitigate them and ensure the stability and success of a business.

At the early stages of starting a business, it’s critical to bring on board a competent cannabis accountant and attorney. Don’t let the simplicity of creating an entity mislead you into missing out on getting proper counsel on the appropriate entity type. Stay attentive to accounting and legal concerns and make informed decisions. If the chosen entity type does not align with your business goals, a knowledgeable cannabis accountant will discuss the potential consequences of each option. This will enable you to make an informed decision.

Given the ongoing discourse surrounding entity type and its status as a commonly asked question, I deemed it worthwhile to introduce this information. It should be noted that a Limited Liability Company (LLC) is not officially classified as a tax entity by the IRS. The taxation of an LLC can vary and may be classified as a single-member LLC, a corporation, or a partnership.

One of the biggest risks in the cannabis industry is the risk of failure and the accumulation of a large tax debt. The cannabis industry is heavily regulated and taxed, which can present significant financial challenges for businesses operating in this field. In order to mitigate this risk, it is important for cannabis businesses to have a strong understanding of the tax laws and regulations applicable to their operations, and to have a robust system in place for tracking and reporting their financial transactions. Working with a knowledgeable and experienced cannabis accountant can help ensure that tax laws are applied correctly and that businesses stay in compliance with the regulations, reducing the risk of financial failure and tax debt. The establishment and enhancement of robust internal controls, coupled with diligent monitoring, can also significantly contribute to mitigating potential risks as well.

It is noteworthy that individuals who own cannabis businesses are known for taking risks. As a result, it is essential to have accountants and attorneys who are skilled in evaluating and reducing these risks. Selecting your advisory team carefully is of utmost importance.

Aligned Mission and vision

It is necessary for the business owner and accountant to have a clear and transparent understanding of each other’s needs and goals, in order to create a win-win situation. The highly regulated and complex cannabis market can be challenging, and having an accountant who is passionate and aligned with the business owner’s mission and vision can help smooth the business cycle and avoid conflicts. An accountant’s mission is to help their clients manage their financial resources effectively and efficiently. This involves tracking the financial performance of the business, providing advice on financial decisions, and ensuring compliance with legal and regulatory requirements. In order to carry out this mission effectively, an accountant needs to have a deep understanding of the business owner’s goals, objectives, and overall strategy.

When a cannabis accountant’s mission is aligned with a business owner’s, they can work together to achieve common goals. This alignment helps the accountant understand the business owner’s financial needs, which enables them to provide more targeted advice and recommendations. It also helps the business owner understand the importance of financial management and how it can contribute to the success of their business. It also helps the business owner feel more confident in their accountant’s advice and recommendations, which can lead to collaborative and effective working relationships and more successful outcomes.

Experience or training in the cannabis industry

The cannabis industry is new and constantly evolving, and it is important to have an accountant who is trained and up-to-date with the latest developments. Many CPA firms are now specializing in the cannabis industry, giving business owners more options to choose from. A cannabis accountant should be familiar with 280E of the Internal Revenue Code, which can be a monster in terms of tax for the industry. They should also have knowledge of cost accounting and inventory management, which are crucial for producing accurate financial statements. Cannabis accountants with a background in manufacturing industry can bring their expertise to the industry and be of even greater value.

The use of the word “trained” is intentional in highlighting the fact that the cannabis industry is new and constantly evolving. Even though accounting firms with decades of experience are doing their best, when they have a high volume of clients, they may not be able to provide timely service and may lack time for innovation and data analysis. There are many cannabis think-tank groups and programs that can give trained accountants the same advantages, or even more, as experienced ones, as technology has revolutionized all industries, including accounting.

Analytical Reporting

A knowledgeable cannabis accountant should be able to provide financial statements and analyze them to help the business understand its financial position and take actionable steps towards its goals. They should be able to simplify complex financial analysis and provide key performance indicators and ratios that can help the business stay on track. They also have the responsibility of managing cash flow, which is key for the success of any business, especially in a competitive market. Many businesses fail because they run out of cash, not profit.

An insightful analysis takes the information one step further and presents the data in context in a way that identifies the necessary actions to be taken to maintain or improve the organization’s operations. Reports that allow managers to do their jobs better and make better decisions will be highly valued.

In a competitive market, the role of accountants and CFOs becomes increasingly important.

Ultimately, conducting business is a spiritual pursuit that involves the right mindset, effective communication, and teamwork. A business will flourish and make a positive impact if it brings together a team with a strong cultural alignment and a growth mindset.

We have great respect for those who work in the cannabis industry, as they often put their lives or licenses on the line. Let us strive for greater compliance and work towards creating a better world for all.

Sevana Janian is a Certified Public Accountant in California with more than 17 years of experience in tax and accounting. She is a member of the Cultivation Committee of the National Cannabis Industry Association (NCIA) for the year 2023. She is also a member of AICPA and CalCPA organizations. Sevana enjoys traveling with her family and playing the piano during her leisure time. She is committed to networking with others to expand her personal and professional knowledge. Sevana is passionate about inspiring and motivating the younger generation to succeed.

Green Plus CPA aims to offer a world-class automated tax and accounting solution nationwide for CEOs and business owners in the cannabis industry who seek accurate financial statements. Established in 2022, we are deeply interested in the medicinal properties of the cannabis plant and firmly believe in its potential to heal. We are enthusiastic about supporting and serving this industry that has been overlooked.

Lobby Congress with NCIA – Hear From First-Time Attendees

Spring is almost here, and NCIA’s 11th Annual Cannabis Industry Lobby Days are just two months away!

Over the past decade, NCIA members have made real, measurable progress moving the dial for cannabis policy reform. Year after year, our industry continues to gain support from members of Congress on both sides of the aisle on crucial issues like banking access, 280E reform, and federal de-scheduling.

It’s not a matter of IF, it’s a matter of WHEN and HOW. Lobby Days is YOUR opportunity to make sure federal legalization is favorable to main street cannabis.

This is the most important cannabis event of the year, so you don’t want to miss this opportunity to join your industry peers in the halls of Congress. Be sure to REGISTER NOW to join NCIA members to advocate for the issues most important to small cannabis businesses and to share your personal stories with national lawmakers who need to hear from Main Street Cannabis now more than ever.

Never lobbied Congress before?

Hear from these first-time attendees of last year’s Lobby Days:

Committee Insights | 12.7.22 | How To Use A Marketing Mindset To Raise Capital For Your Cannabis Company

NCIA’s #IndustryEssentials webinar series is our premier digital educational series featuring a variety of interactive programs allowing us to provide you timely, engaging and essential education when you need it most.

In this edition of our NCIA Committee Insights series, originally aired on December 7 and produced by NCIA’s Marketing & Advertising Committee, our panel of cannabis finance specialists, leading operators and capital raising experts will guide you through best marketing practices and considerations to deploy when fundraising in the cannabis industry from a marketing perspective.

Learn tips and tricks and do’s and don’ts from marketing pro’s and industry insiders to best position your company to get the attention of investors in the current market conditions just as you’ve done when targeting consumers.

The cannabis industry is one of the fastest-growing sectors in Michigan. It’s also an ever-changing industry, leading to myriad challenges for businesses operating within this space. One issue licensees face is a significant gap in vital business intelligence that’s needed to remain relevant in an extremely competitive market.

To help fill this gap, Rehmann partnered with A&K Research, Inc. of Northville, Mich. to survey cannabis operations within the state and to create the 2022 Michigan Cannabis CFO Outlook. As one of the leading professional advisory firms serving the cannabis industry in Michigan, Rehmann spearheaded this project to help cannabis licensees make empowered business decisions based on peer feedback.

The 2022 Michigan Cannabis CFO Outlook shares findings from the survey, including top challenges the cannabis industry faces in Michigan. Top-of-mind concerns: managing the financial side of the business; deciding whether it’s time to sell the business and how best to go about it; staying on top of compliance requirements; navigating federal legislation and resulting tax burdens; and understanding potential changes in lending laws that impact relationships between banking institutions and legitimate cannabis-related businesses.

In addition, this report features industry spotlights highlighting current cannabis businesses facing these issues in real-time. They share how they’re navigating this ever-evolving industry and economic landscape.

Michigan Marijuana Sales

Just how quickly is this industry growing? Michigan saw $21 million in medical cannabis sales and $188 million adult-use marijuana purchases in July 2022 – a total that is about $15 million greater than the previous monthly record set in April 2022. Most of the marijuana sales for both medical and recreational use were for flower products, followed by vape cartridges. Data also shows a continuation of a sales trend in Michigan’s marijuana market, with medical cannabis purchases decreasing and adult-use sales increasing.

Report Takeaways

Here’s a snapshot of report insights and some of our takeaways. You can download the full 2022 Michigan Cannabis CFO Outlook here.

Tax and M&A Activity

39% of companies are considering or are in the process of selling their business. This could be due to the current challenges of operating within the Michigan cannabis market or for a variety of other reasons. Many licensees are entrepreneurs who enjoyed starting and growing the business from the ground up and are ready to move on.

Half of the companies are paying an effective tax rate between 20% and 30%. One in five currently show a loss from operations. This was surprisingly much lower than we expected. It’s not uncommon to see tax rates of over 50% within the industry depending on where the business falls in the vertical chain and how aggressive you can be with your structure or costing model.

Cannabis Business Operations

Just over one-quarter (28%) of businesses have been subject to some level of federal, state, or reporting audits. The industry is still young, and as we continue to look at this data year over year, we expect this number to drastically increase. It’s important to have your finances in order to be prepared for that time to come.

Almost two-thirds (65%) use QuickBooks for their accounting system, with the remainder being dispersed between Sage, SAP, Dynamics, and Xero. Accounting for the cannabis industry can be extremely complex. Many cannabis businesses started with QuickBooks and are now outgrowing that system and ready for more powerful systems to meet their unique needs.

Perceptions of the Current Michigan Cannabis Industry

The majority (56%) expect retail pricing needing another 1-3 years to stabilize. One of the biggest concerns within the industry is pricing of cannabis. We’ve seen a significant drop in retail pricing over the past several years and there is concern that it may drop even more.

Nearly half (42%) think that between 26% and 50% of wholesalers are losing money at current retail prices. Given the struggles with pricing, growers who are selling wholesale are facing a lot of challenges at this point. As more and more operations start up within Michigan (a state without a license cap), the market continues to move toward oversaturation.

What some of the survey respondents had to say about the state of the industry:

“As a small-sized grower focusing on high-end quality, we are impacted greatly by falling retail prices. The rampant increase in licenses/grows caused a glut in the market that has yet to subside. We are focusing all our efforts on lowering costs to keep up with falling prices.” [Grower]

“The industry is currently in a very fragile state. The testing numbers are overinflated for potency, customers are going back to the black market and the current pricing is not sustainable. In addition, new businesses for all areas are opening and believe there is enough capacity for everyone to make money.” [Testing Facility]

“If 280E would go away, things would be much better. Limited licensing for cultivation and processing would also help.” [Grower, Processor & Provisioning Center / Retailer]

To download your digital copy of the full report today, click here.

Chris Rosmarin manages the commercial audit practice in Grand Rapids and also leads the Firm’s cannabis practice. He provides audit and other assurance services, due diligence services and accounting advisory services to various companies both large and small.

Chris understands that clients expect and deserve a partner that is responsive, invested in the relationship and dedicated to helping them respond to their challenges. He strives to deliver on those expectations by meeting deadlines and being available and present throughout the relationship.

Rehmann is a professional advisory firm that provides accounting and assurance, business solutions and outsourcing, specialized consulting, and wealth management services. For over 80 years, Rehmann has provided forward-thinking solutions to our clients. With nearly 900 associates in Michigan, Ohio, and Florida, we are the momentum behind what’s possible. We focus on the business of business — allowing companies and individuals to focus on what makes them extraordinary. We help you look to the future with confidence, thanks to our unrivaled expertise and integrity. Through our partnerships with our clients and communities, we drive impact that empowers our world. Find us online at rehmann.com.

Service Solutions | 10.26.22 | Show Me the Money – The Current State of Cannabis Lending

NCIA’s Service Solutions series is our sponsored content webinar program which allows business owners the opportunity to learn more about premier products, services and industry solutions directly from our network of established suppliers, providers and thought leaders.

In this edition originally aired on Wednesday, October 26, 2022 we were joined by the experts from cannabis-focused financial institutions FundCanna, Safe Harbor Financial, and AVANA Companies to dive deep into the current state of cannabis lending with leading industry journalist John Schroyer of Green Market Report.

A decade after California and Colorado became the first adult use states, the regulated U.S. cannabis market encompasses over 70,000 cannabis-related businesses. Shockingly, most of those businesses still lack easy access to debt and other forms of growth and operating capital. From federal prohibitions and the impact of IRS regulation 280e, to state and local taxation issues, the costs of operating a regulated cannabis company continue to remain nearly unendurable.

Learn what may change in the coming six to 12 months so you’ll know how to access debt capital most cost-effectively in this ever evolving environment. No matter your place in the industry or the supply chain from cultivators, manufacturers, vendors, suppliers, distributors and retailers this conversation will provide the insights to meet your financial needs.

At the conclusion of the discussion our panel hosted a moderated Q&A session to provide NCIA members an opportunity to interact with leading minds from the financial services space, join today to contribute to future conversations!

Panelists:

Adam Stettner

Founder & CEO

FundCanna

Sundie Seefried

Founder and CEO

Safe Harbor Financial

02:13 – Equity vs. Debt: With equity dried up, should cannabis companies be looking at debt financing to grow now?

07:28 – Equity vs. Debt: What do borrowers need to do before approaching a debt provider (vs. an equity provider)?

13:25 – Equity vs. Debt: What can cannabis companies or entrepreneurs do to improve their overall credit worthiness prior to seeking capital?

17:16 – How has the interest rate increases by the Federal Reserve impacted capital markets (and the industry at large) in 2022?

26:07 – Audience Q&A: “If there’s “no reason not to have banking” for your cannabis business how can I easily (and inexpensively) establish and maintain a compliant bank account?”

28:56 – Lending: What significant lending challenges are your clients currently facing within the industry?

33:56 – Lending: What advice can you provide business owners for evaluating lenders that you should (or shouldn’t) work with and tips for avoiding predatory lending practices?

39:05 – Cannabis Reform: What impact do you expect President Biden’s recent announcement will have on the industry?

49:32 – Audience Q&A: “Are your financial institutions planning to offer lending and banking services in New York, New Jersey and other new markets?”

51:42 – Audience Q&A: “With the mindset of “Investors are betting on the Jockey not the Horse.” What type of CEO or founding team would be a red flag or not a viable investment?”

55:19 – Audience Q&A: “How can I start to shift my retail company from being primarily a cash-only business?”

1:05:03 – NCIA Member Appreciation Credit Sequence

Sponsored By:

Video: NCIA Today – Thursday, October 22, 2022

NCIA Director of Communications Bethany Moore checks in with what’s going on across the country with the National Cannabis Industry Association’s membership, board, allies, and staff. Join us every other Thursday on Facebook for NCIA Today Live.

Video: Defending Main Street Cannabis Businesses

As the only national advocate for small and mid-sized cannabis businesses, NCIA works every day to advance policy reforms favorable to the whole industry — not just the wealthiest few. Hear from NCIA Board Members why our mission and advocacy work is crucial to defending the interests of everyday businesses in the cannabis industry.

We are Main Street Cannabis, not Wall Street Cannabis.

Become a member of NCIA today so that everyone can benefit from cannabis legalization — not just the wealthiest few.JOIN NCIA TODAY

Joining NCIA ensures that your interests are heard in our nation’s halls of power as the rules for national legalization are written. We’re also the only full service trade association in the industry, which means that our members enjoy unparalleled ROI and benefits to help them thrive in an increasingly challenging environment.

Video: Main Street Cannabis Heads to Capitol Hill in D.C. in September!

This is your chance to unite with other NCIA members to advocate for the issues most important to small cannabis businesses – from SAFE Banking to federal de-scheduling – and to share your personal stories with national lawmakers who need to hear from Main Street Cannabis businesses.

Watch this video to hear from NCIA’s CEO and Co-founder, Aaron Smith, about why you should attend this most impactful and crucial event next month. Not yet a member? Join today and then make your plans to join us in D.C.

Midsummer Movement: The Pre-August Recess Rush in D.C.

Photo By CannabisCamera.com

By Michelle Rutter Friberg, NCIA’s Deputy Director of Government Relations

As Congress gets ready to beat the D.C. heat and leave Washington for their annual August recess, there’s at least one thing on their minds: cannabis.

Last week, Senate Majority Leader Chuck Schumer (D-NY) along with Finance Committee Chair Ron Wyden (D-OR), and Sen. Cory Booker (D-NJ) introduced their much anticipated Cannabis Administration and Opportunity Act (CAOA), which is now the Senate’s only pending legislation that would provide comprehensive cannabis policy reforms across the nation.

The landmark bill would remove cannabis from the federal Controlled Substances Act and move regulatory responsibility from the Drug Enforcement Administration (DEA) to the Alcohol and Tobacco Tax and Trade Bureau (TTB), the Food and Drug Administration (FDA), and other agencies to protect public health and safety. The bill would also institute a federal excise tax of 5-25% on cannabis on top of the already-hefty state taxes imposed on the industry, concerning advocates for small cannabis businesses and equity operators.

The long-awaited CAOA was introduced after sponsors circulated a discussion draft last year. NCIA and other advocacy organizations provided comprehensive feedback to the bill’s authors last year. Notable changes to the legislation include:

Increases the permissible THC by dry weight from the current 0.3 percent to 0.7 percent and refines the definition of “hemp,” and consequently “cannabis” by taking into account the total THC in a cannabis product, rather than just delta-9 THC.

Changes to the weight quantity to qualify a person for felony cannabis distribution or possession charge under the section from 10 pounds to 20 pounds.

Provides that a court shall automatically, after a sentencing review, expunge each federal cannabis conviction, vacate any remaining sentence, and resentence the defendant as if this law had been in place prior to the original sentencing.

Enables a noncitizen who has received a deportation order based on a cannabis-related offense to file a motion to reconsider that decision. If the motion to reconsider is filed within 30 days of the removal order, the motion may allow for the cancellation of the deportation order.

Establishes a new 10-year intermediary lending pilot program in which SBA would make direct loans to eligible intermediaries that in turn make small business loans to startups, businesses owned by individuals adversely impacted by the war on drugs, and socially and economically disadvantaged small businesses.

Removes the requirement to maintain a bond for any cannabis business that had less than $100,000 in excise tax liability in the prior year and reasonably expects excise tax liability in the current year to be below such amount.

Incorporates rules similar to rules currently applicable to permitted malt beverage producers and wholesalers.

While the historic nature of the CAOA cannot be understated, the bill has a multitude of challenges ahead of it. Not all Senate Democrats support the legislation, making the 60-vote filibuster threshold nearly impossible. Plus, with only a couple dozen legislative days between now and the end of the session, time is also working against advocates.

Dovetailing with the introduction of the CAOA, the Senate Judiciary Committee’s Subcommittee on Criminal Justice and Counterterrorism will hold a hearing titled “Decriminalizing Cannabis at the Federal Level: Necessary Steps to Address Past Harms” this Tuesday. While the witness list has not been made public as of publication, expect the hearing to focus on the newly introduced legislation and how it would affect communities most impacted by the war on drugs.

In other news, the House and Senate will vote on a revised research bill, the Cannabidiol and Marihuana Research Expansion Act, this week. The bill is expected to pass both chambers and be sent to President Biden’s desk for his signature. The Senate bill is sponsored by Sens. Dianne Feinstein (D-CA), Chuck Grassley (R-IA), and Brian Schatz (D-HI) and passed by unanimous consent in March. The House bill is sponsored by Reps. Earl Blumenauer (D-OR) and Andy Harris (R-MD), and passed 343-75 in April. One of the notable areas of compromise? The House bill would have allowed researchers to do their studies on cannabis that’s actually being sold to consumers in dispensaries. That was removed during negotiations, meaning that researchers will still have to obtain their cannabis from the University of Mississippi’s cultivation facility.

There’s still time before recess begins, so make sure you stay tuned to NCIA’s podcast, social media, and newsletter to stay up-to-date on all the latest from Washington, D.C.! Interested in making more of an impact? Don’t forget to register for our upcoming 10th Annual Cannabis Industry Lobby Days on September 13-14, 2022!

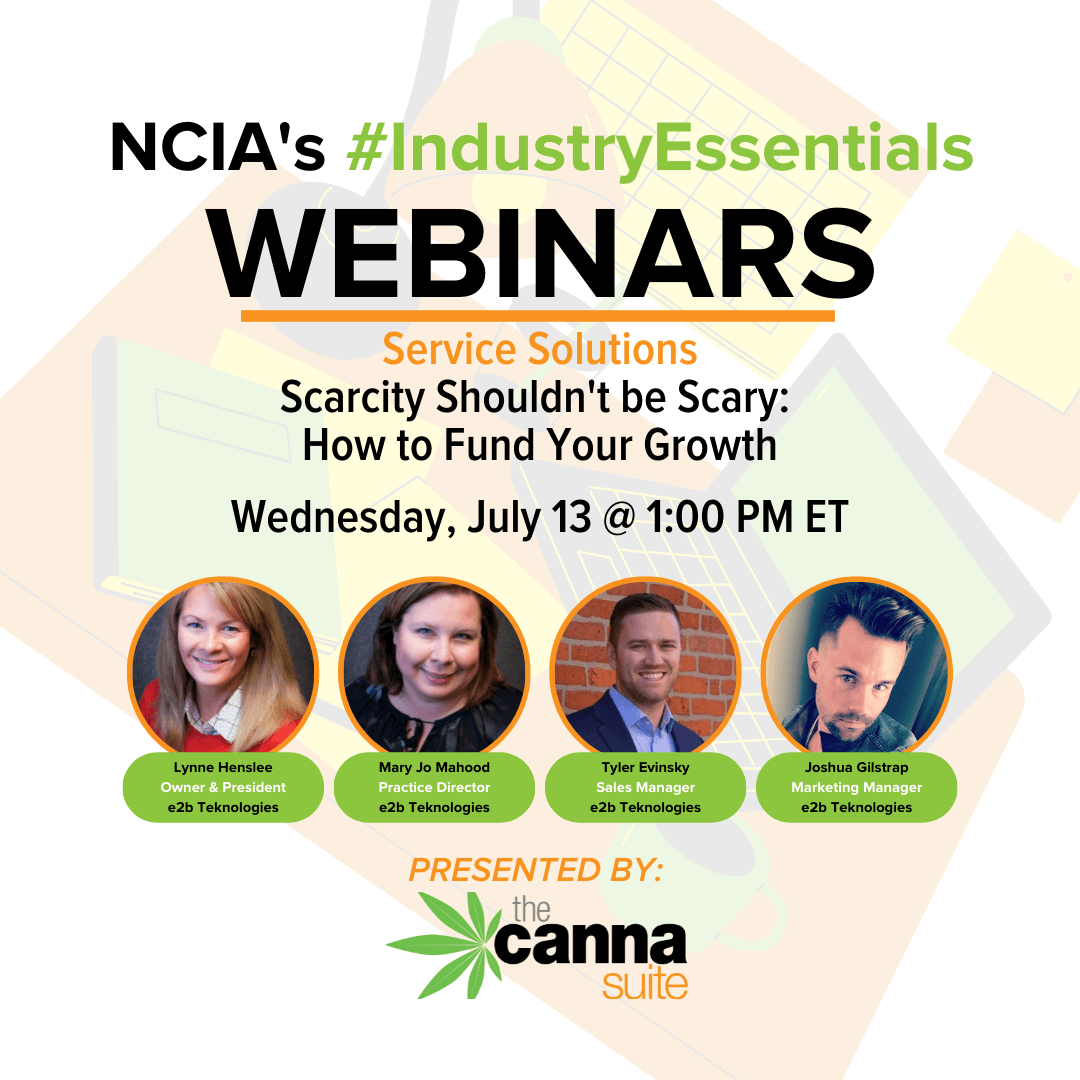

Service Solutions | 7.13.22 | Scarcity Shouldn’t be Scary – How to Fund Your Growth

NCIA’s Service Solutions series is our sponsored content webinar program which allows business owners the opportunity to learn more about premier products, services and industry solutions directly from our network of established suppliers, providers and thought leaders.

In this edition originally aired on Wednesday, July 13, 2022 we were joined by e2b Teknologies whose team of leading integration & technology experts discussed some easy steps to prepare your business for funding and accelerated growth. As you all know, competition was stiff for funding prior to 2022 but with the current economy and rising interest rates, capital is much harder to acquire today. You should be taking steps get noticed and get the MONEY you need to grow your business now.

After viewing you’ll walk away with a better understanding of:

• How to leverage a team properly

• What’s most important – It may not be what you think.

• What’s necessary in terms of reporting, compliance, and record-keeping

• Evaluating potential technology partners

Sit back and settle in for an informative and timely program outlining the challenges facing operators and how you can position yourself for success with the right tools to help succeed at scale.

Equity Member Spotlight: Banyan Tree Dispensary – Adolfo “Ace” Castillo

NCIA’s editorial department continues the Member Spotlight series by highlighting our Social Equity Scholarship Recipients as part of our Diversity, Equity, and Inclusion Program. Participants are gaining first-hand access to regulators in key markets to get insight on the industry, tips for raising capital, and advice on how to access and utilize data to ensure success in their businesses, along with all the other benefits available to NCIA members.

Tell us a bit about you, your background, and why you launched your company.

My name is Adolfo Castillo. People who know me call me Ace. Before I started my first cannabis business, I had a 10-year career in the banking industry. I started in a call center as a customer service associate. I then moved into a traditional banking center where I learned sales and eventually became the assistant manager. It was at the end of my tenure in 2008 that my Tia Eloise was diagnosed with terminal cancer. At the request of my mother, she asked me to get some cannabis in hopes that it would help her sister eat. Although it did not cure cancer, it really helped her appetite and gave her a bit of relief. Unfortunately, my Tia Eloise lost that battle, but it was the relief that I was able to provide that helped bring me peace when she passed away. This all happened around the same time that bill SB 420 was signed into California law, establishing statewide guidelines for Prop. 215. This law paved the way for cooperatives and collectives to begin operating legally in my city. It was at that moment that my love for cannabis became a passion. I felt a need to help more people gain access to cannabis, so I partnered with a friend of mine who sold weed and I took what I had learned about business and applied it to opening my first medical cannabis dispensary.

What unique value does your company offer to the cannabis industry?

I named the dispensary Banyan Tree after an experience I had in Maui about 13 years ago. It was my first visit to Maui so I decided not to bring any cannabis products to avoid any problems at the airport. When I arrived, I asked a few locals where I could find some good smoke and they all pointed me to the Banyan Tree. It was true. As soon as I found the Banyan Tree, I could tell this was the place to be. The smell was in the air and I met some really nice Hawaiians who were happy to hook me up. I want our guests to have the same experience when they visit our dispensary. Banyan Tree is a destination. A place where friends can meet to find quality cannabis.

As a local native, I understand the cannabis culture in my town. The legacy market has thrived for so long in Fresno. One of our biggest challenges will be convincing medicinal users and cannabis connoisseurs to buy their cannabis from a licensed facility and not from the streets. In order to create the best experience possible, it starts with a well-trained, knowledgeable staff. I am lucky to have two educators on my team who have helped me put together a robust employee development program that will ensure that the Banyan Tree staff will be primed for success.

My goal for Banyan Tree is to be the #1 dispensary to work for. I truly believe that the success of your business relies heavily on its employees. I want our employees to have purpose and feel proud of the work they do. Banyan Tree was built upon the idea of helping our surrounding community achieve wellness and enjoyment through cannabis. When you come to Banyan Tree, you will not be rushed, you will feel safe, your questions will be answered, and the price you pay will not shock you.

What is your goal for the greater good of cannabis?

I am hopeful that I will see full legalization in my lifetime. As a cannabis business operator, I would like cannabis to be recognized as a normal commodity and not this taboo substance that has so much negativity around it and red tape. As a business owner, I would like cannabis commerce to transact and be accepted without any special rules in regards to banking and filing federal income tax. As outdated stereotypes are finally fading away, more and more consumers view cannabis as an integral part of their health and wellness routine. I’m confident that in 20 years we will look back at the history of cannabis and just laugh at all the nonsensical rules surrounding cannabis in the early 2000s.

What kind of challenges do you face in the industry and what solutions would you like to see?

Most cannabis operations are running all-cash businesses because mainstream, national banking institutions are not willing to support a federally illegal industry. A small number of state-chartered banks and credit unions have offered financial services to compliant operations, but establishing these relationships continues to be a significant challenge for operators.

An equally frustrating financial challenge is IRS Tax Code 280E, which states that “no deduction or credit shall be allowed in running a business that consists of trafficking a controlled substance.” This archaic code impacts cannabis businesses across the nation, causing unnecessary fiscal and operational stress.

Why did you join NCIA? What’s the best or most important part about being a member through the Social Equity Scholarship Program?

I joined NCIA through the Social Equity Scholarship program to extend my network of cannapreneurs and to help develop best practices and guidelines that will shape the future of our industry. I would say for me, the best part of being a member of NCIA is the synergy. One of my favorite parts of the program is the “Power Hour.” Each week, Mike Lomuto hosts a zoom meeting dedicated to Social Equity members. It is where we have an opportunity to share ideas and find solutions to the issues we all face in our industry. I am very capable, but I recognize that by fostering relationships and collaborating with others in my industry, I can achieve far more than I could ever achieve on my own.