House Floor Debates, Markups, and Beyond for SAFE Banking and MORE Act

Photo By CannabisCamera.com

By Michelle Rutter Friberg, NCIA’s Deputy Director of Government Relations

Usually, things are somewhat slow when it comes to cannabis policy reform in Washington, D.C., but the last week has been quite the whirlwind! In the span of one week, the SAFE Banking Act was included in (and passed via) the must-pass National Defense Authorization Act (NDAA) and the House Judiciary Committee marked up and subsequently passed the Marijuana Opportunity, Reinvestment, and Expungement (MORE) Act!

Last week, the House passed the language of the SAFE Banking Act for the fifth time via the must-pass NDAA. NCIA and our allies on Capitol Hill are always trying to be creative and come up with new, different avenues to advance our policy priorities, and the NDAA was a great opportunity that we were able to take advantage of! At first, there were some concerns that the language (proposed as an amendment to the larger package) would not be ruled germane, however, we were able to clear that hurdle in the House Rules Committee, allowing the provision to move forward for Floor debate and a vote.

The amendment was then debated for a short period of time on the House floor and for the first time ever, passed via voice vote! This is incredibly exciting and reinforces the strong, bipartisan support that this legislation has.

SAFE’s inclusion in the Senate’s version of the bill is a bit more uncertain. Currently, the Chair and Ranking Member of the Senate Armed Services Committee (which has jurisdiction over the NDAA) have circulated their draft of the package that differs in many ways from the House’s bill. Here at NCIA, we will be working with Senate allies to determine what’s next for the NDAA in that chamber and collaborating with other stakeholders to ensure that the SAFE Banking language is included and passed into law. I’ll be the first to admit that I am not (nor have I ever been) a defense lobbyist, however, I’m definitely getting a crash course now!

Then, less than 24 hours later, the House Judiciary Committee announced that they would be holding a markup on the Marijuana Opportunity, Reinvestment, and Expungement (MORE) Act. You’ll recall that the MORE Act was marked up in that committee in November 2019 (during the last Congress), and passed by a vote of 24-10. Then, after all of the other relevant committees waived their jurisdiction, the MORE Act was brought to the House Floor in December 2020 and passed 228-164.

While the MORE Act passed out of the Judiciary Committee this session by a vote of 26-15, the bill still has a long journey ahead of it. It’s unlikely that committees like Ways and Means and Energy and Commerce will waive their jurisdiction again, and it’s critical to remember that the chamber actually became slightly more conservative following the 2020 election. Additionally, there is no companion legislation in the Senate as of publication.

As always, NCIA will continue to work with our allies and stakeholders on and off Capitol Hill to get these policies enacted into law. Have questions? Find me on NCIA Connect. Want to become more involved with policy at NCIA? Learn more about our new Evergreen Roundtable here.

Member Blog: How to Avoid Compliance Issues with Your Cannabis Business

All businesses must adhere to tax rules and regulatory compliance, but for cannabis companies, the laws are significantly more challenging to navigate. The cannabis industry has specific tax rules that differ from other sectors, and failing to follow them can result in severe financial and legal implications.

At Green Space Accounting, we know that managing your finances as a cannabis company can be much more complicated than the average start-up. Keeping a compliant financial system in place is not always easy with constantly changing state laws and regulations.

Here are a few tips on how to avoid compliance issues with your budding cannabis business.

Have Your Business Documentation in Order

One of the first steps to staying compliant is to have all the appropriate financial information and licensing for your business on hand.

Always be prepared with copies of your cannabis license, information from your seed-to-sale tracking system, and your point of sale software records. Having this paperwork, along with legal documents like operating agreements, Articles of Incorporation or Organization, and EINs will ensure that you have a fully compliant relationship with your bank, as well as local and state government.

It’s also a good idea to have detailed records on all sales transactions within your business, especially ones dealing with cash. Cash is used more frequently in cannabis dispensaries than in other retail industries. Having proper cash-handling procedures in place can save you from theft and keep you ready for any unexpected auditing.

Stay up to Date with State and Local Regulations

It’s important to remember that regulations surrounding cannabis change over time, so monitoring your state legislature and all applicable state and local agencies is crucial to keeping your business compliant. By making yourself aware of the rules for the cultivation, manufacturing, and distribution of cannabis, you can avoid the risk of fines or legal action and build a better relationship with your local government, law enforcement, and, most importantly, customers.

One way to stay up to date with regulatory compliance laws is to consume state and industry news surrounding cannabis daily. Not only do these publications keep you informed on business and consumer trends, but they also avoid complicated legal jargon, speaking directly to business owners in a way that’s easy for them to understand.

Another great way to stay on top of state and local cannabis laws is to network and build relationships with your local regulators. While maintaining compliance internally is the biggest goal, creating an ongoing relationship with the regulators in your area can help you better understand the changes within the industry and the steps you can make to conduct business more transparently.

Develop SOPs, Training, and Reporting Systems

Think of these SOPs as a set of rules that all employees need to abide by to keep your company’s production, sales, and accounting processes consistent and safe. Having a set of standard operating procedures can help you recognize potential compliance issues and fix them before they occur. These procedures can include an employee handbook on proper handling and storage of cannabis consumables to installing a seed-to-sale tracking system for inventory management purposes.

The best way to stay on top of your SOPs is to create reports, checkbooks, and logs in all aspects of your operations to show regulators that you are a transparent business that has a complete understanding of your state’s compliance laws. Frequent compliance training sessions are also an effective way to educate your entire team on the legal and tax regulations associated with your business.

Cannabis Payroll

To avoid issues concerning payroll, installing time tracking software for employees is also a great way to keep your staff organized and stay on top of the 280E tax code. The 280E law denies cannabis businesses federal income tax deduction for operating business expenses, which means that the wages for some employees may be deductible, and some may not be. By introducing software where employees can specify the tasks they’re doing and track the salaries they’re receiving, you’ll stay compliant with the tax code and better understand the productivity your team is generating.

Frequently Audit your Business

Hiring an outsourced accounting team to audit your cannabis business is a great way to avoid any potential risks regarding compliance. Auditors serve as an additional, unbiased set of eyes that will examine all areas of your organization and identity aspects that might need improvement.

If you are looking to stay on top of the legal and tax regulations for your cannabis business on a tight budget, self-auditing your company is a great way to check whether or not your training, bookkeeping, and SOPs are being appropriately implemented.

Entrepreneurs who belong to the National Cannabis Industry Association can receive discounted access to an acclaimed compliance management platform created by Simplifiya, which gives licensed operators a self-audit checklist that helps them identify, track, and mitigate potential issues before it’s too late. The platform also provides templates for creating SOPs customized for each license type and tied directly to your state regulations.

The Bottom Line

Whether you are a start-up, a growing business, or a multi-state operator, complying with federal and state compliance laws is essential. By following the above tips and staying transparent with your employees, partners, and investors, you’ll be ready for any audit that comes your way.

Whether you’re looking for cash flow management, business planning, or internal controls, our team is dedicated to helping you achieve peace of mind when it comes to your company’s finances and compliance. We understand that the financial side of your business can be daunting, complicated, time-consuming, and most of all: stressful. You don’t need to go through it alone. Our team is prepared to help you achieve your financial goals. Whether you’re looking to earn more revenue, scale your business or achieve a little peace of mind, you can trust Green Space Accounting to guide you.

Video: NCIA Today – September 3, 2021

NCIA Deputy Director of Communications Bethany Moore checks in with what’s going on across the country with the National Cannabis Industry Association’s membership, board, allies, and staff. Join us every Friday here on Facebook for NCIA Today Live.

Member Blog: Commercial Property Assessed Clean Energy (C-PACE) – A Competitive Funding Source for the Cannabis Industry

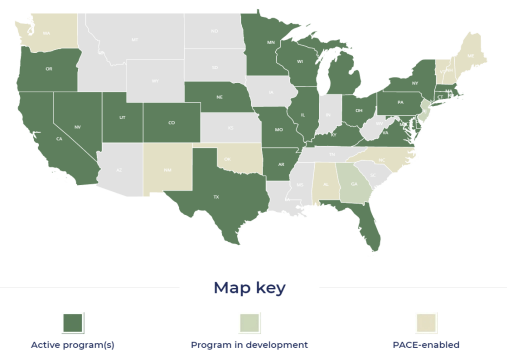

The state-by-state level of legalization and expansion of cannabis continues to pick up momentum across the United States, however, the adoption at Federal level is a much slower movement. The absence of federal legalization has created a situation where federally insured lending institutions like banks and traditional investment capital markets are prohibited from funding cannabis projects. The direct result of this restriction in capital has historically forced the cannabis industry to rely exclusively on private loans and individual investors as the primary sources of development and operating capital. These sources of capital are limited in capacity and can garner interest rates from 15-25%. While the legalized cannabis industry has made great strides in removing much of the negative stigma surrounding the products and their uses, resulting in the opening of some additional funding sources such as crowdfunding and angel investors, the cost of these capital sources is still significantly above the conventional market rates. At Ebee Management Group, we would argue that the most underutilized yet best financing tool presently available for the cannabis industry is the Commercial Property Assessed Clean Energy (C-PACE).

C-PACE is an innovative financing tool that gives owners of commercial, industrial, and multi-family properties access to long-term fixed-rate financing for energy efficiency, water conservation, and renewable energy projects. The C-PACE legislation authorizes municipalities or counties to partner with private capital providers to deliver financing options to commercial property owners for energy qualified improvements with the collection of the debt repayment through a special assessment on the property’s tax bill. The C-PACE funds provide upfront capital with 100% financing for qualified improvement often with terms up to 20 years. The resulting energy savings and reduced operating and maintenance costs typically exceed the amount of the assessment payment and often contribute to a positive cash flow to the operating budget.

The primary caveat to the use of C-PACE for cannabis is that the property must be in a state that has passed the legislation that empowers local municipalities to provide C-PACE as a funding tool. C-PACE can be funded directly by the municipality through a bond issuance; however, most projects are presently being funded by the private equity markets. Typical terms on a C-PACE-funded cannabis transaction are 100% financing, fixed for a term up to 20 years at interest rates ranging from 7%to 9%. The maps below illustrate the current enactment of state-level policy for both cannabis and PACE.

Map provided and maintained on the PACENation website

C-PACE can be utilized for any improvement that saves energy with maximum lending limits influenced by individual state legislation and program guidelines. Typically, the maximum loan amount is capped at 20-25% of the completed appraised value and restricted to funding only qualifying improvements. Typical qualified improvements include lighting, HVAC systems, and building controls, doors, windows, roofs, and alternative power generation like wind and solar. PACE can be used for retrofitting an existing building, new construction, and in some states, refinance of existing debt. For the established cannabis market, the refinance option is an extremely attractive tool because it can be utilized to pay off higher-cost investor debt and is non-recourse to the owner. The debt is tied to the physical facility as a special assessment, not a mortgage lien, and is thus fully transferable at sale. You heard me right. If you have a short-term hold strategy for a facility, any remaining obligation you have associated with your PACE assessment does not have to be paid off at closing. The balance of the debt follows the tax bill and transfers directly to the new owner like any other existing tax-based assessment.

The table below outlines the benefits and features of C-PACE

Owner Benefits

Financing Features

Qualified Equipment

• Lower cost capital

• Non-recourse to owner

• Preserves owner’s capital

• Debt transfers at sale

• 100% financing of qualified improvements

• Long-term fixed-rate up to 20 years

• Competitive interest rates ranging from 6.5%-9.5%

• Debt securitized by a special assessment on the property

• Lighting

• HVAC

• Controls

• Roofs

• Doors & Windows

• Insulation

• Power factor conversion

• Alternative energy generation

The future of a wider array of funding options for the cannabis industry will clearly be impacted by both the ongoing adoption on a state-level and the possible federal-level legalization. Presently the pressure from states like New York and Chicago that house the two largest capital markets in the United States is leading to the expanded conversations about tapping into some of these sources of capital. That being said, arguably the best real-time solution for structuring a cannabis capital stack is C-PACE. New construction, building retrofit, or refinance, C-PACE can fill a gap or serve as a lower-cost replacement of other investment capital or equity.

Dr. Teresa Smith leads the Strategic Growth & Development for Ebee Management Group where she is recognized as an industry expert in sustainable development, leveraging PACE financing solutions for qualified energy efficiency projects throughout Ohio and Michigan. Prior to joining Ebee in 2019, Teresa was the Business Development Manager for the Toledo-Lucas County Port Authority where she built a robust growth process that delivered a 280% annualized increase in Property Assessed Clean Energy (PACE) loan transactions, driving loan balances from $3 million in 2011 to $47 million in 2019. Teresa obtained a Bachelor Degree in Economics from Eastern Michigan University, a MBA in Executive Management from the University of Toledo and a Doctorate Degree in Business Management with a specialty in Leadership from Capella University.

Ebee Management Group is a full-cycle construction, finance, and energy management firm, offering our clients the most cost-effective and appropriate development strategies — never compromising integrity and quality. We oversee every aspect of the project with a proprietary process and unique energy financing programs, delivering a custom designed, state-of-the-art energy savings solution with a guarantee to save you time, energy, and money. Ebee offers a wide array of financing solutions for the Cannabis Industry that reduce equity requirements and replace much more expensive sources of capital. Our flagship financing tool for new construction, renovation and refinance of commercial facilities is Commercial Property Assessed Clean Energy (C-PACE). This financing tool makes it possible for owners and developers of commercial properties to obtain low-cost, non-recourse, long-term financing which is paid back through an annual assessment on the organization’s property tax bill. For more information, contact Teresa Smith at 419.340.0420, tsmith@ebeeco.com or visit our website athttps://www.ebeeco.com/

Committee Blog: Successful Retail Outcomes of SAFE Banking

By NCIA’s Retail Committee

Have you ever wondered where or how a cannabis retail business banks? You should know that it’s complicated because of federal prohibition. So what do you do? Some are finding workarounds and loopholes, others are able to obtain services with smaller financial institutions for exorbitant costs, while many others struggle to maintain an expensive, risky, and dangerous cash-only ecosystem.

The 2020 elections set the creation of four new regulated state cannabis markets in motion, and four more state legislatures followed suit in the first half of 2021, making the last year arguably one of the most consequential and momentous periods for the cannabis industry and policy reform.

However, cannabis is still illegal at the federal level, classified as a Schedule I substance under the Controlled Substances Act, despite state-level regulated cannabis markets in more than half the country. This prevents banks from doing business with cannabis companies because of fear of prosecution or reputational risk, as these businesses aren’t viewed as legal under outdated federal laws.

The cannabis industry is optimistic about the future, though, thanks to an increasing interest in cannabis, public safety, and economic development in Congress. Lawmakers in both chambers are actively debating comprehensive legislation to remove cannabis from the schedule of controlled substances and regulate it federally while repairing some of the harms caused by prohibition, but there are also incremental reforms in play that have a track record of success in the House as well as bipartisan support. Chief among them is the Secure and Fair Enforcement (SAFE) Banking Act, which would provide safe harbor for financial institutions that wish to work with state-legal cannabis businesses and allow them to provide services to the industry without fear of prosecution. This legislation originally passed the House in 2019 and was the first piece of standalone cannabis policy reform legislation ever to receive a vote or be approved by a full chamber vote.

Since then, cannabis banking has been approved in the House three more times in various forms, mostly recently when it passed the SAFE Banking Act again – and with record bipartisan support – earlier this year. The bill is now awaiting consideration in the Senate, but has yet to be taken up by the Senate Banking Committee.

So, what does the SAFE Banking Act mean for retail cannabis businesses?

Loans, capital markets, and credit card processing are common interests for cannabis companies. Access to traditional lending is particularly important for small businesses that usually lack connections to angel investors and venture capital. However, some of the benefits of this legislation are of special interest to cannabis retailers. Check out what some of the Retail Committee members are considering to be important aspects of broadened access to banking and financial services:

Safety

“As a retail cannabis business operator, safety is of our top priorities as it directly affects our staff, our patrons, and our bottom line,” said Larina Scofield, director of retail operations at Lucy Sky Cannabis Boutique dispensary chain in Colorado and vice-chair of NCIA’s Retail Committee. “We are required to operate as a predominantly cash business in a high-risk industry that can sometimes lead to criminal targeting; this can put not only our business at risk but also the potential individuals on-site if a targeted crime were to take place.

“There is also no doubt that operating a cannabis business is costly, due in part to the fact that we do not receive the same benefits and protections that other businesses have; cannabis companies are also subject to higher fees in order to get similar services, if those services are available at all. Lucy Sky is fortunate enough to have banking and armored services, as well as a cashless ATM service to allow for safer money handling, but this does not come without a price… a high price. Our company pays top dollar every year in order to have banking and secured payment delivery (something that is not seen in traditional businesses), in order to provide safety for our business and to the individuals who frequent our facilities.

“SAFE Banking would mitigate that and allow for retail cannabis companies to operate without having to “constantly look over their shoulders” so to speak. It would provide an enormous sense of security in an already high-risk business, it would allow for small business owners to receive proper funding to allow for safer operations, and it is truly crucial in the progression of the industry as a whole.”

Less Cash on Premise

“Less cash during COVID-19 is always a plus. The goal is to limit contact, and we all know cash is constantly being passed from person to person. There are plenty of studies highlighting how many germs really are on physical cash. Researchers found plenty of questionable microbes on $1 bills in a more recent study. In a world where we are all concerned about our physical health, the time is now to reduce physical cash in cannabis businesses. Or at least, give people the choice to go cashless if they want to. Let’s also not forget the security benefits of carrying less cash on the premises”, said Byron Bogaard, CEO of Highway 33, a cannabis dispensary in Crows Landing, California, and chairperson of NCIA’s Retail Committee.

Contactless Delivery for Retail

“Golden State Greens had a spike in deliveries during the COVID pandemic but were still forced to collect cash and signatures from customers. When online orders can process card transactions we can make a true contactless delivery where both payment and signature are managed from the customer’s device. This will increase the safety of our drivers by maintaining safe distancing practices and allow new types of deliveries to drop boxes or to customers’ homes similar to Amazon,” said Gary Strahle, chief growth officer for California dispensary Golden State Greens.

Beyond these major issues, there are a number of potential outcomes that could impact retailers as well.

Revamping the relationship between cannabis businesses and banks will likely trigger higher competition for banking services, resulting in lower fees. This would clearly benefit small businesses but could also have an impact on the frequency and nature of mergers and acquisitions in the cannabis space.

Regulatory frameworks will certainly change, and outstanding litigations will most definitely become more complex. Chargebacks from credit transactions will be a constant problem, due to the level of surveillance and data collection they will more easily be disputed.

Better access to banking also positions technology companies for success, as there will be a high demand for mobile wallets, online ordering, and automatic recurring memberships. We can’t predict everything, and there might be more hurdles to cross than we realize, but the technologically-agile retailer may benefit most. Studies show that most of the Top Fortune 500 Companies use software platforms such as Salesforceto manage their enterprise, however many of the canna-specific solutions are missing much of the integration and scalability needed to immediately handle broadly increased access to the banking system.

Speak your voice.

The SAFE Banking Act is critical to the cannabis industry’s success, and your voice will tip the scales. Reach out to your members of Congress, especially your Senators, and tell them what safe banking means to you as a cannabis retailer. Remember, policy needs to support logic over emotion. Emotions are important, but remind Senators of the logic behind implementing safe banking solutions for cannabis businesses:

Reducing the risk of robbery & theft with less cash on the premises

Supporting the demand cannabis businesses receive, which in turn supports the local and national economy and helps minimize the unregulated market

Reduce pathogen transmission by limiting physical cash transaction

If your senator already supports the SAFE Banking Act, please politely ask them to prioritize this legislation in the current session.

Member Blog: We’re Out of the Weeds – CRC Releases Initial Rules & Regs for New Jersey’s Adult-Use Marketplace

New Jersey recently passed the Cannabis Regulatory, Enforcement Assistance, and Marketplace Modernization Act (“CREAMMA”). Among other things, CREAMMA permits adults 21 years and older to consume cannabis and allows New Jersey residents to operate six types of cannabis businesses within the state. The new adult-use marketplace, as well as the already established medicinal marketplace, will be administered by the Cannabis Regulatory Commission (“the CRC”). The CRC is a panel of five appointed members who will oversee the development, regulation, and enforcement of the use and sale of all legal cannabis in New Jersey.

The CRC recently approved its first set of rules and regulations on August 19, 2021. This will enable the start of the licensing process for personal adult-use cannabis operations in New Jersey. Here are the 15 takeaways from the initial rules and regulations:

What type of license can I apply for?

There are six different license types:

Class 1 – Cannabis Cultivator License

Class 2 – Cannabis Manufacturer License

Class 3 – Cannabis Wholesaler License

Class 4 – Cannabis Distributor License

Class 5 – Cannabis Retailer License (also includes consumption lounges)

Class 6 – Cannabis Delivery License

Businesses may also apply for a license to operate a cannabis testing facility or medical cannabis testing laboratory. License-holders may hold multiple licenses concurrently; however, there are limitations on the number and type of licenses that may be held concurrently.

Are there any caps on the number of licenses that may be awarded?

The State only placed a cap on Class 1 licenses for cultivators. In particular, there will be a statewide cap of a total of 37 cultivators until February 22, 2023. Keep in mind that state limits aren’t the end of the inquiry; municipalities may set restrictions on the number of businesses in their jurisdiction.

What are the fees to apply for one of the adult-use licenses?

In an effort to make the application fee reasonable, the CRC will require applicants to only pay 20% of the application fee at the time of application, and the remaining 80% will only be collected at the time the license is approved. The initial application cost may be as low as $100 but successful applicants should be prepared to pay additional fees ranging from a total cost of $500 – $2,000.

Are there any fees other than the initial application fee?

Yes. There are annual licensing fees, which can range from $1,000 for a microbusiness to $50,000 for a cultivator, with up to 150,000 square feet of cultivation capacity. This fee range only applies to the adult use marketplace. There is a different licensing fee schedule for the medicinal use marketplace.

Will anyone be given priority in the application process for a cannabis license?

Yes. The CRC will prioritize applicants who live in specifically definedeconomically disadvantaged areas of New Jersey or who have past convictions for cannabis offenses (“Social Equity Applicants”). It will also prioritize applications from minority-owned, woman-owned, or disabled veteran-owned businesses that are certified by the New Jersey Department of the Treasury (“Diversely Owned Businesses”). Businesses in impact zones will also take priority (“Impact Zone Businesses”).

What do you mean by “priority review?”

Applicants meeting the criteria described above will have their applications reviewed before other applications, regardless of when they apply. Remember, however, that priority review doesn’t guarantee selection.

When will the CRC begin to review applications?

No date has been announced, but the CRC promises that it will be soon. The CRC will publish notice in the New Jersey Register announcing its intent to review applications and submissions will be reviewed, scored, and approved on a rolling basis (pun intended), subject to the required priority review for certain applicants.

What should I expect from the application?

Applicants will be expected to submit a detailed application that includes specific details for the proposed site for the business (which must be owned or leased), municipal approval, and zoning approval. Applicants must also submit an operating summary plan detailing the applicants’ experience, history, and knowledge of operating a cannabis business. The scoring of applicants and awarding of licenses will be based entirely on the application materials.

What if I don’t have all of the materials to submit a complete application?

Don’t worry, you can apply for a “Conditional License.” A Conditional License is a provisional award that gives the holder 120 days to become fully licensed by satisfying all the requirements for full licensure, includingfinding an appropriate site, securing municipal approval and applying for conversion to an annual license.

What are the requirements to be considered for a Conditional License?

Conditional License applicants mustsubmit a separate application for each cannabis business license requested, along with a background disclosure, a business plan and a regulatory compliance plan to the CRC. At the time of the application, all owners with decision-making authority of the conditional license applicant will need to prove that they made less than $200,000 in the preceding tax year, or $400,000 if filing jointly.

Are there any advantages in being awarded a Conditional License?

Conditional License holders that convert to an annual license will not have to submit the sections of the application that, under statute, require applicants to demonstrate experience in a regulated cannabis industry. This flexible option offers an opportunity for newcomers to get into the cannabis industry.

What is a Microbusiness License?

Microbusiness licenses are for applicants who want to run a relatively small operation. Applicants may apply for a microbusiness license for any of the six license types. A microbusiness license limits the business to 10 employees; a facility of no more than 2,500 square feet; possession of no more than 1,000 plants per month; and/or a limit of 1,000 pounds of usable cannabis per month.

Can I rely solely on my local municipality for a license?

No. The state must award the cannabis license. Municipalities play a critical role, however, in the licensing process. For example, applicants will only be licensed by the CRC if the applicant has demonstrated support from the municipality, zoning approval, and has been verified to operate in compliance with any other local licensing requirement.

Can municipalities ban cannabis businesses from operating within their jurisdiction?

Yes. Municipalities may ban certain businesses from operating within their borders if they enact an ordinance regulating or banning cannabis businesses by August 21, 2021. Municipalities may update their ordinances at any time to remove any restrictions that they previously placed.

What happens if I don’t follow the CRC’s rules and regulations?

The CRC is authorized to inspect cannabis businesses and testing laboratories, issue notices of violations for infractions and issue fines. Standard fines can be no higher than $50,000, while fines for infractions implicating issues of public safety or betrayal of public trust can be as high as $500,000. Licenses may also be suspended or revoked. Don’t take the risk!

These 15 key points present only a quick summary of the CRC’s initial set of rules and regulations. We anticipate there will be a second set of rules released later this year, which will likely resolve issues that weren’t addressed in the initial set of rules and regulations, or CREAMMA. We expect the second set of rules and regulations to focus mainly on the needs of distribution and delivery service, and preparing for the acceptance of applications, before the Garden State is in full bloom…

Charles J. Messina is a Partner at Genova Burns LLC and Co-Chairs the Franchise & Distribution, Agriculture and Cannabis Industry Groups. He teaches one of the region’s first cannabis law school courses and devotes much of his practice to advising canna-businesses as well as litigating various types of matters including complex contract and commercial disputes, insurance and employment defense matters, trademark and franchise issues and professional liability, TCPA and shareholder derivative actions.

Jennifer Roselle is a Partner at Genova Burns LLC and Co-Chair of Genova Burns’ Cannabis Practice Group. She has unique experience with labor compliance planning and labor peace agreements in the cannabis marketplace. In addition to her work in the cannabis industry, Jennifer devotes much of her practice to traditional labor matters, human resources compliance and employer counseling.

Daniel Pierre is an Associate at Genova Burns and a member of the Cannabis and Labor Law Practice Groups. In addition to labor work, he likewise assists clients in the cannabis industry, from analyzing federal and state laws to ensure regulatory compliance for existing businesses to counseling entrepreneurs on licensing issues.

For over 30 years, Genova Burns has partnered with companies, businesses, trade associations, and government entities, from around the globe, on matters in New Jersey and the greater northeast corridor between New York City and Washington, D.C. We distinguish ourselves with unparalleled responsiveness and provide an array of exceptional legal services across multiple practice areas with the quality expected of big law, but absent the big law economics by embracing technology and offering out of the box problem-solving advice and pragmatic solutions.

Given Genova Burns’ significant experience representing clients in the cannabis, hemp and CBD industries from the earliest stages of development in the region, the firm is uniquely qualified to advise investors, cultivators, processors, distributors, retailers and ancillary businesses.

Committee Blog: Safety – Terpene Limits in Cannabis Manufacturing

by NCIA’s Cannabis Manufacturing Committee

From the taste of your fruits and vegetables to the aroma that travels from trees and flowers in bloom, terpenes are the organic compounds that play a vital role in the flavors and smells we experience daily. Terpenes are common ingredients that are used in many industries such as food, cosmetics, tobacco, and pharmaceuticals. Therefore, the information on the safety of terpenes in these industries can be used for determining the safe use of terpenes in a wide range of product applications.

Terpenes are currently being introduced into a variety of adult-use and medical cannabis preparations across the U.S. and hemp-CBD markets around the world for both flavor and functional purposes. Much research has been and still is being conducted on the therapeutic effects of terpenes and their synergistic effects when used in conjunction with cannabinoids. The strong research background supports the benefits of infusing terpenes into cannabis extracts, both in reference to endogenous terpenes found naturally in the plant and those terpenes that have been added back into preparations from other botanical sources. Therefore, almost every manufactured cannabis product contains a percentage of terpenes. However, the clear lack of understanding of the full potential of the terpene profiles, and misuse of these volatile, fragile compounds bring up various misconceptions regarding terpene safety versus their efficacy in creating an elevated user experience.

As terpenes make a significant contribution to the quality of cannabis products, which varies from one consumption method to the other, it is highly important to utilize the most advanced knowledge regarding terpenes in order to maximize their potential while maintaining product safety.

Inhalation

Bioavailability

Terpenes are a naturally occurring constituent in resin cannabis extracts. Terpenes have been incorporated into vaporizable formulations in the form of pre-filled cartridges. These terpene formulations are designed to produce specific effects based on the creator’s intentions, or the terpenes are simply reintroduced to mimic the source material since the extracts are often refined to the point that they have little or no taste (i.e., lost their original essence).

Inhalation of these volatile molecules leads to quick absorption of the compounds via the lungs and directly into the bloodstream. The high solubility of monoterpenes in the blood and hydrophobic medium suggests a high respiratory uptake and accumulation in fat tissues (Falk 1990a). This was confirmed by recent studies of uptake and elimination of a-pinene and 3-carene in humans (Falk 1990b, Falk 1991b). The bioavailability range via inhalation of alpha pinene, camphor and menthol has been studied and reported to be 54-76% (Kohlert 2000) which is relatively high compared to oral bioavailability. Therefore, terpenes via inhalation are an efficient route of administration which allows low dosage of terpenes.

General Guidelines

When examining terpene infusion, the points below should be taken into consideration:

From accumulated knowledge within the cannabis industry and considering terpenes’ natural ratios in cannabis (1 – 5%) and data on safety, it is suggested not to exceed a concentration of 10% in the final product.

As terpenes are volatile molecules, the final terpene-infused product is recommended to be used only with adjustable temperature vaporizers such that the oil will not be heated to high temperatures to prevent unnecessary heat-derived toxin production.

Aerosol testing for the final product is recommended to test for heavy metals leaching into the vaporizable product.

Terpenes are recommended to be used within their defined expiration date labeled on the suppliers’ bottle. The final vaporizable product must be tested in a certified lab under the requirements of the authority having jurisdiction to make sure it meets all quality and regulatory requirements.

Terpene Limits

By using position papers such as the ANEC Position Paper on E-cigarettes and e-liquids, suggestions regarding terpene limits can be made for cannabis inhalable products. It is important to mention that the final decision on added terpene amounts and determination of product safety is the sole responsibility of the manufacturer based on their assessments, internal procedures, and local regulations.

The following numbers are the suggested infusion percentage of specific terpenes in E-liquid. This suggestion was calculated by using DNEL (Derived No Effect Level) levels in inhalation as well as frequency of puffs a day.

On average, E-liquid users take 500 puffs a day (ANEC position paper), whereas cannabis users take around 9 puffs a day. Therefore, the suggested terpene limit percentage in cannabis inhalables may be higher than E-liquid due to the lower daily usage.

Substance

Suggested Terpene Limit in E-liquid According to ANEC

Linalool

0.34%

Menthol

7.8%

Beta Pinene

0.7%

Alpha-Terpineol

1.1%

Geranyl Acetate

7.4%

Carvone

0.14%

Ingestion

Bioavailability

Terpene presence in foods of plant origin and in herbs with functional properties has led to further exploration of their bioavailability following oral consumption. The research on terpenes’ bioavailability is commonly done through medicinal plants since they are subjected to digestion within the mouth and stomach before accessing the small intestine. Bioavailability through oral ingestion is affected by mechanical actions, enzymatic actions, and different pH conditions, Transformations into usually more water-soluble and more readily excreted in the urine compounds affect this process as well. These transformations appear mainly in the liver, but also in the gastrointestinal tissue, lungs, kidneys, brain, and blood (Furtado 2017) Several studies have shown that terpenes consumed orally are absorbed through the gastrointestinal tract and are bioavailable as soon as 0.5 h after intake, reaching their peaks between 2 and 4 h (Furtado 2017, Papada 2018).

General guidelines

Terpenes are commonly used as flavor ingredients and their usage guidelines are clear when used in foods, such as the FEMA values table below. However, when terpenes are used for therapeutic purposes, the suggested dose in food is not fully researched, and the balance between flavor and functionality is still yet to be determined. Basing the dosing according to flavor guidelines is a good place to start. Upper limits should be defined by safety limits such as the DNEL values table found below. It is important to use natural, Food Grade terpenes that are backed up with certificates of analysis and are safe to ingest.

Terpene Limits

The Flavor and Extract Manufacturers Association of the United States (FEMA) has developed an innovative program utilizing the GRAS concept to evaluate the safety of flavoring substances. The FEMA GRAS program began in 1959 with a survey of the flavor industry to identify flavor ingredients then in use and to provide estimates of the amounts of these substances used to manufacture flavors. This database provides information on all ingredients that have been determined to be “generally recognized as safe” under conditions of intended use as flavor ingredients. According to The FEMA GRAS assessment – aromatic terpenes used as flavor ingredients are ubiquitous throughout the food chain; and therefore, not surprising that they serve as effective flavoring ingredients.

The below table presents the average maximum usage levels of terpenes used as flavors in several product types as provided by FEMA.

Product

Lime Terpenes

Average Max (ppm)

Orange Terpenes

Average Max (ppm)

Grapefruit Terpenes

Average Max (ppm)

Limonene Average Max (ppm)

Myrcene Average Max (ppm)

Linalool Average Max (ppm)

Beverages, Nonalcoholic

750

1,550

500

31

4.4

7

Beverages, Alcoholic

1,000

1,000

1,000

NA

NA

50

Chewing Gum

20,000

20,000

20,000

2300

NA

200

Hard Candy

5,000

5,000

5,000

49

13

400

Soft Candy

5,000

5,000

5,000

NA

NA

10

ppm is an abbreviation for “parts per million” and it also can be expressed as milligrams per liter (mg/L) or in a percentage where 10,000 ppm is 1%. For example, the maximum suggested infusion for orange terpenes in chewing gum is 2%, where the suggested infusion in hard candy is 0.5%.

*Point of thought*: Since terpenes in the cannabis industry are mostly infused in cannabis-based products, the frequency of usage of such products is lower than regular food products.

Additional safety data can be gathered from reviewing reports from governmental agencies such as European Chemicals Agency (ECHA). The following data about the DNEL (Derived No Effect Level) in the category of General Population was collected from ECHA website. These numbers may be used as a guideline for maximum daily intake via oral administration:

Substance

DNEL (Derived No Effect Level)

Calculated Daily DNEL for 70kg subject (mg/day)

Linalool

0.2 mg/kg bw/day

14

Menthol

4.7 mg/kg bw/day

329

Beta Pinene

0.3 mg/kg bw/day

21

Alpha-Terpineol

no hazard identified

no hazard identified

Geranyl Acetate

8.9 mg/kg bw/day

623

Carvone

69.4 µg/kg bw/day

4,858

For example, a 70 kg person consumes a 1g cookie that is infused with 1% Pineapple Express terpene formulation and Linalool constitutes 10% of the formulation, then there will be overall 10mg of terpene formulation in the cookie, out of the 10mg there is 0.1mg of Linalool which doesn’t exceed the DNEL level.

Topical

Bioavailability

Terpenes are lipophilic, small, and nonpolar molecules that are considered to be the largest group of natural fragrances. Terpenes can easily penetrate the skin and enhance transdermal delivery (Aqil 2007) and can potentially aid cannabinoid transdermal delivery. Terpenes are also known to have several dermal benefits including anti-inflammatory (Maurya 2014), wound healing (d’Alessio 2014) and anti-acne (Yuangang 2010). Terpene bioavailability via transdermal delivery ranges between 3-12% depending on the type of terpene, medium and application (Brain 2007, Gilpin 2010). Following topical application, maximum plasma levels of terpenes are reached within 10 minutes (Kohlert 2000).

General guidelines

While some terpenes are known as dermal irritants, the severity of the irritation may depend on their concentration. These should not be used on any inflammatory or allergic skin condition and should always be appropriately diluted. The oxidation of terpenes can increase risk of causing skin reactions because the oxides and peroxides formed are more reactive. This can be seen with (+)-limonene, δ-3-carene and α-pinene and arise due to the formation of oxidation products, some of which are more sensitizing than the parent compound. For this reason, proper storage of terpenes is required to preserve their effectiveness and decrease the risk of adverse reactions.

The table below lists commonly known allergenic terpenes, and for this reason, should be declared on the packaging or in the information leaflet if the concentration of these allergenic fragrances is higher than the permissible concentration of 0.01% in shower gels and baths (rinse-off products) and higher than 0.001% in body oils, massage oils and creams (leave-on products)

Allergenic Terpenes

Citral

Citronellol

Eugenol

Farnesol

Geraniol

Isoeugenol

D-Limonene

Linalool

Terpene Limits

The International Fragrance Association (IFRA) defines which compounds represent a potential allergy risk and determines their maximum concentration to produce safe cosmetic products. IFRA also issues recommendations for the safe use of fragrance ingredients, which are published in the IFRA Code of Practice and its guidelines. In the below table, there can be found specific infusion recommendations for specific terpenes.

Substance Name

Restriction Limits in the Finished Product (%) according to IFRA:

Lip Products

Body Lotion, Cream & Oils

Hand Sanitizer & Hand Cream

Body Wash

Citronellol

2.20%

12.00%

3.20%

24.00%

Citral

0.11%

0.60%

0.15%

1.20%

Farnesol

0.21%

1.20%

0.29%

2.30%

Eugenol

0.45%

2.50%

0.64%

4.90%

Geraniol

0.85%

4.70%

1.20%

9.20%

Alpha Bisabolol

0.42%

2.40%

0.60%

4.60%

Testing of terpenes in dermal products can be achieved safely by making a sample product with terpene formulation infused at 0.5% to 5% concentrations in petrolatum. Patch testing can be a useful technique to detect and avoid skin reactions.

While marijuana has been around in Mexico since the 1600s, the real story begins in the 20th century during the Prohibitionist Era. After Mexico news outlets widely reported stories of cannabis users committing violent crimes, a cannabis stigma was created, resulting in Mexico banning the production, sale, and use of cannabis in 1920, followed by a ban of exports in 1927. The movement of cannabis was first regulated by the three U.N. conventions on narcotic drugs, beginning with the Single Convention on Drugs in 1961. The prohibition gave rise to the cartel’s involvement in the illegal cannabis industry in the ’80s, and these cartels have consistently supplied the U.S. market since. After the war on drugs significantly increased violence in Mexico and gave the cartels more power than before, Mexico began to alter its stance. In 2015, the country decriminalized cannabis use, and in 2017, legalized medical cannabis containing less than 1% THC. In 2018, the Mexican Supreme Court deemed the prohibition unconstitutional, and in December 2020, the U.N. Commission on Narcotic Drugs transferred cannabis from a Schedule 4 to a Schedule 1 drug under the Single Convention. As of now, Mexico is on the edge of legalizing recreational cannabis use. This bill, “The New Federal Law on the Regulation of Cannabis,” is awaiting approval by the Senate and then only needs to be signed by the President to be passed into law.

With a population of 130 million and over 10 million regular cannabis users, Mexico will generate $1.2 billion in annual tax revenues while saving $200 million annually in law enforcement and creating thousands of new jobs. One estimate has cannabis legalization bringing up to $5 billion to the economy annually. One issue Mexico will face will be keeping the cartels from transitioning to the legal cannabis market. While those with criminal records can’t obtain any cannabis license, cartels have a deep network, and Mexican officials can’t always determine whether someone is connected to a cartel. Mexico’s legislators believe the cartel will be forced to operate legally over time as they won’t be able to compete in the illegal market and keep as much power as they currently have.

There are also many questions regarding how Mexico’s cannabis legalization will affect the U.S. market. The USMCA, formerly known as NAFTA, currently does not include cannabis, raising the question of whether Mexican producers will be able to import cannabis into the U.S. for a much lower price than the U.S. can produce domestically. However, the U.S. will likely implement trade barriers to protect domestic companies. Currently, the U.S. places trade barriers on tomatoes in Mexico, and many see similar actions being placed on cannabis.

The United States will likely place a trade barrier on cannabis from Mexico to protect domestic companies

There’s no doubt that cannabis legalization in Mexico will create investment opportunities in the U.S. It mostly comes down to whether the U.S. creates trade barriers with Mexico regarding cannabis. If they don’t, the U.S. cultivation and manufacturing sectors will be hurt badly as Mexico can produce much cheaper. The absence of trade barriers will also hurt testing labs as cultivation moves out of the country and uses testing labs in that same country. However, U.S. companies with distribution networks, retail operations, or strong brands will benefit from Mexican legalization through lower costs of goods sold. One solution that would benefit U.S. companies would be legalizing interstate commerce in the U.S. without federally legalizing cannabis. This means other countries wouldn’t export finished products or raw material with THC above 0.3% into the U.S., and the U.S. industry would develop and consolidate. Once the U.S. federally legalizes cannabis, they must create tariffs or some trade barriers against all the developing countries legalizing cannabis, or the U.S. companies will suffer.

Companies are also greatly affected by banking laws. Currently, companies touching the flower in countries where it is not federally legal cannot access regular banking and can’t list publicly on the NASDAQ or NYSE. However, Canadian companies touching the flower can list in the U.S. since it is federally legal in Canada. These laws mean companies operating in Mexico will also be able to list in the U.S publicly. However, the SAFE Banking Act recently passed the House of Representatives in April 2021 and is up for debate in the Senate. Passage of this act would grant banking access to cannabis companies touching the flower and open the door for these companies to list in the U.S publicly. This would create a large flow of money into U.S. cannabis companies and allow them to scale at a much quicker pace than previously available. One important thing to note is that the large U.S. stock exchanges are technically able to accept cannabis companies’ listings if they meet the exchange requirements. However, they don’t accept them to avoid punishment from the federal government. Therefore, as the government moves towards allowing these companies federal banking access, the main question regarding U.S. companies is raised. In absence of government pressure, will these exchanges allow U.S. companies to list and access their own public markets?

The SAFE Banking Act would reduce risk for cannabis companies transacting with only cash

Overall, companies and investors looking to take advantage of the booming cannabis market need to stay up to date on the fast-changing cannabis legalization process in many countries. Those that truly understand it will position themselves to benefit from what is projected to be one of the fastest-growing industries over the next decade.

Ms. Della Mora is the Co-founder of BLC, a financial advisory and investment firm based in Los Angeles with satellite offices in Houston, New York, London, Hong Kong, and Melbourne. During her tenure at BLC, she successfully invested, assisted in the capitalization, and helped business develop small cap oil companies in Kentucky, Texas, Louisiana, Illinois, Colorado, California, Wyoming, North Dakota, and Alaska. She has also structured oil & gas partnerships in several U.S. states, and in Ecuador, Central America. Ms. Della Mora has been involved in many LNG (Liquid to Natural Gas) projects in the U.S., as well as many commodity trades worldwide. She has personally advised also Chinese conglomerates in their U.S. oil & gas investments.

Black Legend Capital is a leading Merger & Acquisition boutique advisory firm based in California with offices worldwide. Black Legend Capital was founded in 2011 by former senior investment bankers from Merrill Lynch and Duff & Phelps. We provide M&A advisory services, structured financing, and valuation services primarily in the cannabis, technology, healthcare, and consumer products industries. Black Legend Capital’s partners have extensive advisory experience in structuring deals across Asia-Pacific, Europe, and North America.

Crazy for Cannabis Administration and Opportunity Act (CAOA)

Photo By CannabisCamera.com

By Michelle Rutter Friberg, NCIA’s Deputy Director of Government Relations

Last week was undoubtedly one of the most exciting weeks in federal cannabis policy ever! On July 14, Senate Majority Leader Chuck Schumer (D-NY), along with Sen. Cory Booker (D-NJ) and Senate Finance Committee Chair Ron Wyden (D-OR), unveiled long-awaited draft legislation that would remove cannabis from the schedule of controlled substances while allowing states to determine their own cannabis policies. Let’s take a look at what we know:

What is it?

You’ll recall that back in February, the trio of Senators announced that they were working on a comprehensive cannabis bill. Since then, NCIA and other advocates have (im)patiently been waiting to see what shape that would take – I was calling it the best-kept secret in Washington! However, at long last, the discussion draft of the Cannabis Administration and Opportunity Act (CAOA) was released.

A discussion draft is exactly what it sounds like – prior to introducing this language as formal legislation, the Senators have shared it in this form, allowing stakeholders, the public, and others the opportunity to weigh in and provide their expertise and feedback.

What’s in it?

As I mentioned above, the CAOA removes cannabis from the list of controlled substances, effectively legalizing it at the federal level while still allowing states to set their own policies. According to the bill’s detailed summary, it has a few goals:

“… [it will] Ensure that Americans – especially Black and Brown Americans – no longer have to fear arrest or be barred from public housing or federal financial aid for higher education for using cannabis in states where it’s legal. State-compliant cannabis businesses will finally be treated like other businesses and allowed access to essential financial services, like bank accounts and loans. Medical research will no longer be stifled.”

The bill also includes:

Restorative measures for people and communities who were unfairly targeted in the war on drugs.

Automatic expungements for federal non-violent marijuana crimes and allows an individual currently serving time in federal prison for nonviolent marijuana crimes to petition a court for resentencing.

An “Opportunity Trust Fund” funded by federal cannabis tax revenue to reinvest in the communities most impacted by the failed war on drugs, as well as helping to level the playing field for entrepreneurs of color who continue to face barriers of access to the industry.

An end to discrimination in federal public benefits for medical marijuana patients and adult-use consumers.

Respect for state cannabis laws and a path for responsible federal regulation of the cannabis industry. Like with federal regulations on alcohol, under CAOA, states can determine their own cannabis laws, but federal prohibition will no longer be an obstacle. Regulatory responsibility will be moved from the U.S. Drug Enforcement Agency (DEA) to the Alcohol and Tobacco Tax and Trade Bureau (TTB), the Bureau of Alcohol Tobacco Firearms and Explosives (ATF), as well as the Food and Drug Administration (FDA) to protect public health.

A federal tax structure – CAOA would impose an excise tax on cannabis products in a manner similar to the tax imposed on alcohol and tobacco. The general rate of tax would be 10 percent for the year of enactment and the first full calendar year after enactment. The tax rate would increase annually to 15 percent, 20 percent, and 25 percent in the following years.

What’s next?

The discussion draft comment and feedback process will be ongoing until September 1. Until then, NCIA will be working with our board, Policy Council, committees, and our members (particularly our Evergreen members!) to solicit their expert input on some of the areas the Senators have expressed interest in. After that deadline, the Senators will take their time to review submissions and subsequently formally introduce the revised language later this year. Stay tuned via our newsletter, blog, and upcoming events to learn the latest on this and how you can actually submit your thoughts to us!

Even With So Much Progress, We Must Remain Diligent

By Rachel Kurtz-McAlaine, NCIA’s Deputy Director of Public Policy

What a time to be in the cannabis industry! Federal legalization feels like it is finally on the horizon, especially with the big news that tomorrow will be a press conference to introduce a draft discussion bill that has been promised by Senate Majority Leader Chuck Schumer Senate Majority Leader Chuck Schumer (D-NY), Senate Finance Committee Chairman Ron Wyden (D-OR) and Sen. Cory Booker (D-NJ).

When I first started cannabis reform advocacy 25 years ago, cannabis legalization seemed unattainable in my lifetime, given the stigma we were, and still are, up against. But medical cannabis was just starting to pass and more of us were coming around to believing in the potential of the plant and being horrified at the war on drugs to the point that we devoted our lives to ending it. That includes the founders of this organization and many who went on to start businesses that are now members of NCIA.

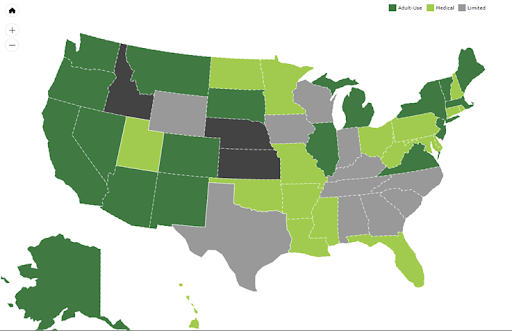

Running a business in the cannabis industry can be a daily challenge, from banking to text messaging to supply chain issues, so it may be hard to notice the sea change happening with cannabis bills around the country. Four state legislatures legalized cannabis just within the first six months of this year, for a total of 18 states and Washington, D.C., that have legalized cannabis for adult use over 21 years of age. (You can check out our state policy map to learn more about the status of different states.)

Believe it or not, that sea change is happening in Congress, too, and we want to make sure we’re doing everything we can to inform you about what is happening and to hear you.

As Michelle wrote about previously in the Government Relations blog, Give Us MORE, the MORE Act of 2021 was reintroduced at the end of this Spring in the House of Representatives. Read Michelle’s excellent summary, but more importantly, read the bill! An almost identical version of the MORE Act passed the House last Fall, only to be held up by a GOP-led Senate, but showed the real momentum happening in Congress.

Despite the hold up in the Senate, there is some bipartisan support. A Republican bill was even introduced in the House, the “Common Sense Cannabis Reform For Veterans, Small Businesses, and Medical Professionals Act,” that would have similar legalization efforts to the MORE Act, such as descheduling cannabis from the Controlled Substances Act and punting on regulations to federal agencies, but would not have any of the provisions that address industry equity and retribution from the years of harm caused by cannabis prohibition.

Support for legalization is now so mainstream that even Amazon is now backing cannabis legalization, expressing support for the MORE Act, although it remains to be seen if they will continue supporting MORE or get behind Sen. Schumer’s bill.

The SAFE Banking Act of 2021 is still in play and remains a crucial bill given that it could have the highest likelihood of passing the soonest. It can be overlooked given the trajectory of descheduling bills, but NCIA’s Government Relations team remains committed to SAFE and continues lobbying for it because, even though we’re planning what descheduling looks like now, it could take a few years to get there. In the meantime, banking is in emergency status.

As federal descheduling appears on the horizon, I encourage you to read the bills, including the Schumer bill, and consider how they will affect you and your business. I’m not saying legislation will necessarily pass this year, but right now is when ideas are being discussed, amendments are being drawn up, decisions are being made.

Consider how much we need to do federally versus getting the states to standardize their regulations versus having a set of voluntary self-regulatory measures that shows we are a self-aware industry and want to be safe for our customers. Keep in mind that much of the alcohol industry is self-regulated, and why would we purposely advocate to regulate ourselves more than the alcohol industry when cannabis is demonstrably safer? I appreciate the thriving alcohol market, the innovation and craft, but I know we can do even better while minimizing harm and acknowledging the past harm, but we have to be diligent.

NCIA is proud and honored to be representing the broad spectrum of the industry, from multi-state operators, to small legacy farmers, to those that have been hurt by past prohibition and want to be part of this thriving industry – all of the industry. That means hearing from you, your concerns, your ideas, your insights. Please feel free to contact me at Rachel@TheCannabisIndustry.org.

I encourage you to read the bills, including Sen. Schumer’s draft discussion bill being released tomorrow, keep reading blog posts, watching webinars, checking out NCIA’s industry buzz, and stay informed because a new day is dawning, but it’s going to be a long day, so we better be prepared for it.

Mid-Year Update on 280E and its Impact on the Cannabis Retail Sector

by Beau R Whitney, NCIA’s Chief Economist

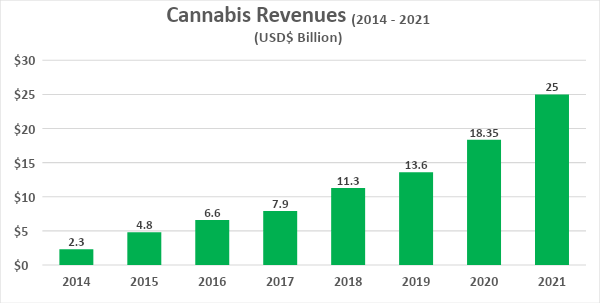

The first half of the year was a strong one for cannabis revenues. After a strong first quarter, with $5.9 billion in revenue, cannabis retailers are experiencing continued growth in Q2 with preliminary results coming in at $6.2 billion to $6.5 billion.

If this trend remains in the second half of the year, the cannabis retail sales are projected to be $24.5 to $25 billion for the year. This would reflect another cycle of 35% year-over-year growth.

Source: Whitney Economics, Leafly

Strong growth in the first half of the year, does not necessarily mean huge profits for the cannabis industry.

While the industry has seen strong growth over the past year, this does not necessarily mean that the industry as a whole is in good shape. Retailers are struggling to make profits due in a large part to federal taxation. IRC 280E does not allow entities conducting business in federally illicit trade, such as cannabis, to write off common and ordinary deductions from their federal taxes. As a result, cannabis operators pay significantly more taxes than other businesses. This has long been an issue with the cannabis industry and organizations such as NCIA has been working tirelessly to address this, but as long as it remains a federal policy it will be negatively impacting the industry.

Cannabis retailers are taking the brunt of federal tax policy.

With over $12 billion in first-half revenues, cannabis retailers will be on the hook for $1.2 billion in federal taxes for the first half of the year alone. This is $756 million more than what “normal” businesses would pay. Cannabis retailers are forecasted to pay over $1.5 billion more in taxes in 2021 and, when combined with the rest of the supply chain, will pay over $2.2 billion in additional taxes in 2021.

280e Example of Impact on Retail

Normal Business

280E Business

Comment

Retail mid-Year Revenue

$12,000,000,000

$12,000,000,000

Based on data from Whitney Economics

Cost of Goods Sold (COGS = 50%)

$6,000,000,000

$6,000,000,000

Ordinary and Necessary Expenses (30%)

$3,600,000,000

$3,600,000,000

Not allowed under 280e

Real Pre-Tax Profit w/o 280e

$2,400,000,000

$2,400,000,000

Taxable Profit

$2,400,000,000

$6,000,000,000

Big difference in taxable rates

Fed Tax @21% *

$504,000,000

$1,260,000,000

Retailers pay 150% more

Effective tax rate

21.0%

52.5%

Some effective tax rates approach 60%-70%

Net Annual Profit (Before State Tax and Debt Service)

$1,896,000,000

$1,140,000,000

A difference of $201,000 per year per retailer

Source: Whitney Economics *Assumes taxed at C-corporation rates

The effective tax rate is forecasted to increase with corporate tax increases.

The effective tax rate increases significantly for retailers and in many cases exceeds 60% to 70%. The level of additional taxes that cannabis operators pay, over the course of the next five years, will increase by an average of $630 million per year for the industry if the business tax rates increase from 21% to 28%. Depending on how corporate tax policy negotiations are settled, things may go from bad to worse for cannabis retailers.

Cannabis retailers are struggling to make ends meet.

Based on sales data from 2020, there were over 7,550 licensed cannabis retailers in the U.S. with each retailer generating an average of $2.4 million per year. This is right around the amount of revenue required to be a sustainable retail business. In 2021, there have been roughly 1,000 more retailers licensed and even with an increase in sales, retailers are only forecasted to average $2.7 million per year.in sales. In fact, in 13 states, retailers are not projected to average the $2.4 million per year to remain viable. While retailers in some states may be OK, other retailers are not able to make ends meet.

What do these numbers tell us?

IRC 280E will reduce cannabis retailers cash flow by $200,000 in 2021 and that $200,000 would go a long way in shoring up the finances and provide retailers with the breathing room they need to remain viable. 280E reform would allow retailers to pay for health care for more employees, hire more workers and expand their business. However, in the current environment, many cannabis operators will continue to struggle.

The key message here is that retailers are under duress due to 280E and policy reform in the area of federal taxes may make the difference between success and failure. The time for reform is now, before it is too late.

Learn more in a recent NCIA Fireside Chat webinar with an all-star panel of accounting experts and operators to dive deep into all things 280E.

Supreme Court of Cannabis?

Photo By CannabisCamera.com

By Michelle Rutter Friberg, NCIA’s Deputy Director of Government Relations

While it’s become commonplace to hear cannabis come up in the halls of Congress, and increasingly so in the White House, there’s one branch of government that has been quieter on the topic: the Supreme Court (SCOTUS). However, this week, conservative Justice Clarence Thomas changed that when the court actually declined to weigh in on a 280E case.

Towards the end of 2020, a Colorado medical cannabis dispensary decided to ask the U.S. Supreme Court to review a lower-court decision that allowed the IRS to obtain business records in order to apply the 280E provision of the tax code. (Fun fact: NCIA member Jim Thorburn, of the Thorburn Law Group, was actually the counsel on record for this appeal!) According to the filings, the IRS overstepped its authority and also violated the company’s Fourth Amendment privacy rights. Some of the questions the company took to the highest court in the land:

Does the Fourth Amendment protect taxpayers from having confidential information released to the IRS and federal law enforcement authorities?

Does the application of Section 280E to state-legal marijuana businesses violate the federal constitution?

Again, while SCOTUS declined to consider this appeal, Justice Thomas took issue with the underlying state/federal discrepancy in the country’s cannabis laws and issued a searing statement. He specifically discussed a 2005 ruling by SCOTUS in a case called Gonzales v. Raich. In this ruling, the court narrowly determined that the federal government could enforce prohibition against cannabis cultivation that took place wholly within California based on its authority to regulate interstate commerce. Check out a few excerpts from Justice Thomas’ statement below:

“Whatever the merits of Raich when it was decided, federal policies of the past 16 years have greatly undermined its reasoning. Once comprehensive, the Federal Government’s current approach is a half-in, half-out regime that simultaneously tolerates and forbids local use of marijuana. This contradictory and unstable state of affairs strains basic principles of federalism and conceals traps for the unwary.”

“Given all these developments, one can certainly understand why an ordinary person might think that the Federal Government has retreated from its once-absolute ban on marijuana. See, e.g., Halper, Congress Quietly Ends Federal Government’s Ban on Medical Marijuana, L. A. Times, Dec. 16, 2014. One can also perhaps understand why business owners in Colorado, like petitioners, may think that their intrastate marijuana operations will be treated like any other enterprise that is legal under state law.”

“As things currently stand, the Internal Revenue Service is investigating whether petitioners deducted business expenses in violation of §280E, and petitioners are trying to prevent disclosure of relevant records held by the State. In other words, petitioners have found that the Government’s willingness to often look the other way on marijuana is more episodic than coherent.”

“This disjuncture between the Government’s recent laissez-faire policies on marijuana and the actual operation of specific laws is not limited to the tax context. Many marijuana-related businesses operate entirely in cash because federal law prohibits certain financial institutions from knowingly accepting deposits from or providing other bank services to businesses that violate federal law. Black & Galeazzi, Cannabis Banking: Proceed With Caution, American Bar Assn., Feb. 6, 2020. Cash-based operations are understandably enticing to burglars and robbers. But, if marijuana-related businesses, in recognition of this, hire armed guards for protection, the owners and the guards might run afoul of a federal law that imposes harsh penalties for using a firearm in furtherance of a ‘drug trafficking crime.’”

“Suffice it to say, the Federal Government’s current approach to marijuana bears little resemblance to the watertight nationwide prohibition that a closely divided Court found necessary to justify the Government’s blanket prohibition in Raich. If the Government is now content to allow States to act “as laboratories” “‘and try novel social and economic experiments,’” Raich, 545 U.S., at 42 (O’Connor, J., dissenting), then it might no longer have authority to intrude on “[t]he States’ core police powers . . . to define criminal law and to protect the health, safety, and welfare of their citizens.””

Just to be clear, these statements don’t change the law of the land, nor do they indicate formal policy developments. They do, however, show that the constantly shifting public perception of cannabis is affecting the way we as a society think about marijuana, which will, at some point, translate into policy. It’s no small feat that one of the most conservative justices on the Supreme Court has weighed in so substantially on this topic. Continue the momentum and join the movement with NCIA!

States Still Leading The Way, With Some Stirrings In Congress

By Morgan Fox, NCIA’s Director of Media Relations

As has been so often true in the history of cannabis policy reform (but is starting to change with your help), the biggest news and progress made this week is at the state level. After a long and arduous legislative session, Connecticut lawmakers approved an adult-use bill, which Gov. Lamont signed on Tuesday!

The new law makes adult possession of up to 1.5 ounces legal and will establish a regulated licensing system. Half of all licenses are reserved for social equity applicants, who will also be able to access training, technical assistance, and startup funding. Limited home cultivation will be permitted in stages (medical first, then adults), and limited social consumption will not just be allowed – it will be mandated in municipalities with more than 50,000 residents.

Let’s put this in a national perspective. If you do not include all the years of foundation-building, activism, and lobbying that go into changing cannabis laws, it took two years for voters to approve adult use in the first four legal states starting in 2012. At that time, passing such laws through elected representatives was unheard of. Now in 2021, four state legislatures have approved adult-use bills in the first six months of the year! We’ve come a long way in terms of state policy reform and momentum is only increasing, but we still have a long way to go.

Now let’s move to Congress, where things tend to move a bit more slowly but are nevertheless picking up speed.

Earlier this month, NCIA endorsed the Drug-Impaired Driving Education Act. This bill, introduced by Reps. Kathleen Rice (D-NY) and Troy Balderson (R-OH), would provide grants and resources to states and organizations to engage in evidence-based impaired driving education. NCIA supports this bill because impaired driving is a serious issue that is most effectively combatted through early and consistent educational outreach, which this legislation promotes to the exclusion of unscientific per se limits and unproven chemical testing technology.

In somewhat related news, a massive transit bill is now awaiting a vote in the House of Representatives after recently passing a key committee. This legislation contains a number of provisions related to impaired driving education, the most important cannabis-related item is a provision that would allow researchers to access and study cannabis products that are available to consumers in state-legal markets rather than depend on federally-approved sources. While the DEA has announced that it will begin granting research production licenses to applicants – many of whom have been waiting for years for approval – there is currently only one legal federal cannabis source, and researchers have consistently complained that it is practically useless due to poor quality and contamination.

Moving on to the SAFE Banking Act, Senate sponsors Jeff Merkley (D-OR) and Steve Daines sent a letter to Banking Committee Chairman Sherrod Brown (D-OH) and Senate leadership urging them to take up the bill for consideration as soon as possible. After overwhelmingly passing in the House in April with a bipartisan vote, the bill has been awaiting review in the upper chamber, with some Democrats wanting to wait until a more comprehensive bill is introduced there.

Advocates and congressional supporters are eagerly awaiting the introduction of that legislation from Senate Majority Leader Chuck Schumer, who has been working closely with Sens. Ron Wyden (D-OR) and Cory Booker (D-NJ) since announcing that this effort would be a priority early this year.

The Senate has quite a bit on its plate at the moment, but we expect things to keep ramping up over the coming weeks and months. Stay tuned!

Video: NCIA Today – June 11, 2021