Member Blog: Reaching The Highest Common Denominator

by Raina Jackson, Founder & CEO of PURPLE RAINA Self Care Member of NCIA’s Diversity, Equity, & Inclusion Committee (DEIC)

This past September I had the pleasure of lobbying in D.C. for the first time as part of NCIA’s 10th Annual Lobby Days. The lobbying process was demystified for me, and I found that lobbying isn’t easy, but it isn’t that hard when you share your talking points from your heart, representing your own and others’ experiences. I learned that the NCIA delegation shares more common ground than we realized with Congressmembers, especially through their younger and more hip staffers and family members. One senator has a daughter who used to be a budtender and now podcasts about the industry, Senator Gary Peters (D-MI).

I was encouraged by how receptive legislative aides and advisors were to the factual talking points and statistics NCIA provided us to appeal to their sense of reason and fairness. They recognized the public health and economic benefits cannabis has delivered and its potential, without being distracted by useless moral arguments against it. Our team gave an overview of the cannabis landscape and advocated while offering solutions to our varied struggles as cannabis entrepreneurs.

We highlighted that 47 states have adopted some form of cannabis commerce and decriminalization, representing 97.7% of the U.S. population! The majority of the American public demands safe access to cannabis. Why not ride the wave?

Cannabis has been found to be a “gateway” medicine for a more safe withdrawal from opioid addiction, especially crucial to states experiencing high overdose death rates.

We discussed the DEA recently approved funds for even more substantial clinical research on the myriad of proven and potential health benefits delivered by the cannabis plant in a wide range of forms. Yet existing cannabis research is often more robust and held to higher standards than over the counter aspirin. Many pharmaceutical drugs are advertised on TV as the best thing since sliced bread one day (albeit with alarming potential side effects), then next named in TV ads for class action lawsuits for their harmful effects.

A case for an enhanced SAFE Banking Act

The legal U.S. cannabis market is valued at $17.7 billion, with a substantial amount unbanked, causing a public safety crisis. Our discussions illuminated our common ground regarding the public safety improvements and economic benefits that the bipartisan supported SAFE Banking Act will bring to each state choosing to introduce its own customized hemp CBD/low THC, medical, or adult recreational cannabis program.

When compliantly banked these funds will offer financial institutions of all sizes more capital for lending to spur economic recovery and a safer industry. While no financial institution will be required to participate, the risk mitigation and sizable financial benefits can’t be ignored.

SAFE will remove the risk of federal prosecution for compliant financial institutions already offering banking to cannabis businesses, while encouraging more banks and credit unions to join them. Too many existing entities providing cannabis banking services tend to mitigate risk by charging exorbitant monthly fees, financially hobbling startup cannabis businesses or excluding them altogether.

SAFE would also support hemp CBD businesses like mine, still navigated the grey area regarding access to banking, loans, leases/mortgages, and payment processing.

In my follow-up email to the Congressional aides and advisors we met with, I attached a white paper authored by the Cannabis Regulators of Color Coalition (CCRC) offering best practices for increasing financial access to cannabis businesses, prioritizing groups that have been historically underserved by traditional financial institutions and disproportionately harmed by prohibition.

What’s next?

This regulated cannabis industry is so new that we must allow each other some grace as stakeholders. As cannabis advocates, we have learned that “calling people in” for discussions on the benefits of the SAFE Banking Act and comprehensive cannabis reform is more effective than “calling them out.”

Elected officials and their staff don’t understand first-hand what we experience as cannabis entrepreneurs, and many care more than I expected. Lobbying and sending them emails on new and modified policy recommendations helps them to be well-informed enough to support us. My highlight was meeting with a CA legislative aide who is a fellow CA native and sincerely wanted to be updated on my progress and pain points. We all had a laugh about him agreeing to let me go into “the weeds” concerning the licensing process, pun intended.

Since Lobby Days, President Biden announced the upcoming FDA and DEA review of cannabis as a Schedule 1 drug. It could potentially be de-scheduling within the next 12 to18 months! However, to date, only seven states provide licensing priority, exclusivity, or set aside a percentage of licenses for qualified social equity applicants. The same way the SAFE Banking act should be passed with amendments fostering equity, state, and future federally legalized cannabis programs must include targeted equity programs to help level the playing field. I look forward to returning to D.C. in May for 2023 NCIA Lobby Days!

Raina Jackson is a multifaceted cannabis brand strategist, product developer, and advocate, and is the founder & CEO of PURPLE RAINA Self Care, the culmination of her love for beauty wellness products, the color purple, and the musical and cultural phenomenon Prince. For the past 7 years she has worked in the San Francisco Bay Area cannabis industry in sales management, field marketing, distribution, and product development, and a verified SF Cannabis Equity applicant in Oakland and San Francisco. For the past year she has served on the NCIA Diversity, Equity, & Inclusion Committee and the Regulatory Compliance subcommittee.

Raina has over 15 years of experience in beauty/wellness care product development, sales/ marketing management, and product education at Maybelline, L’Oréal Professional, and Design Essentials Salon System and has taught cosmetology at The Aveda Institute in SoHo NYC. A San Francisco native, Raina earned a B.A. degree in cultural anthropology and linguistics from Stanford University and an MBA in marketing and management from NYU.

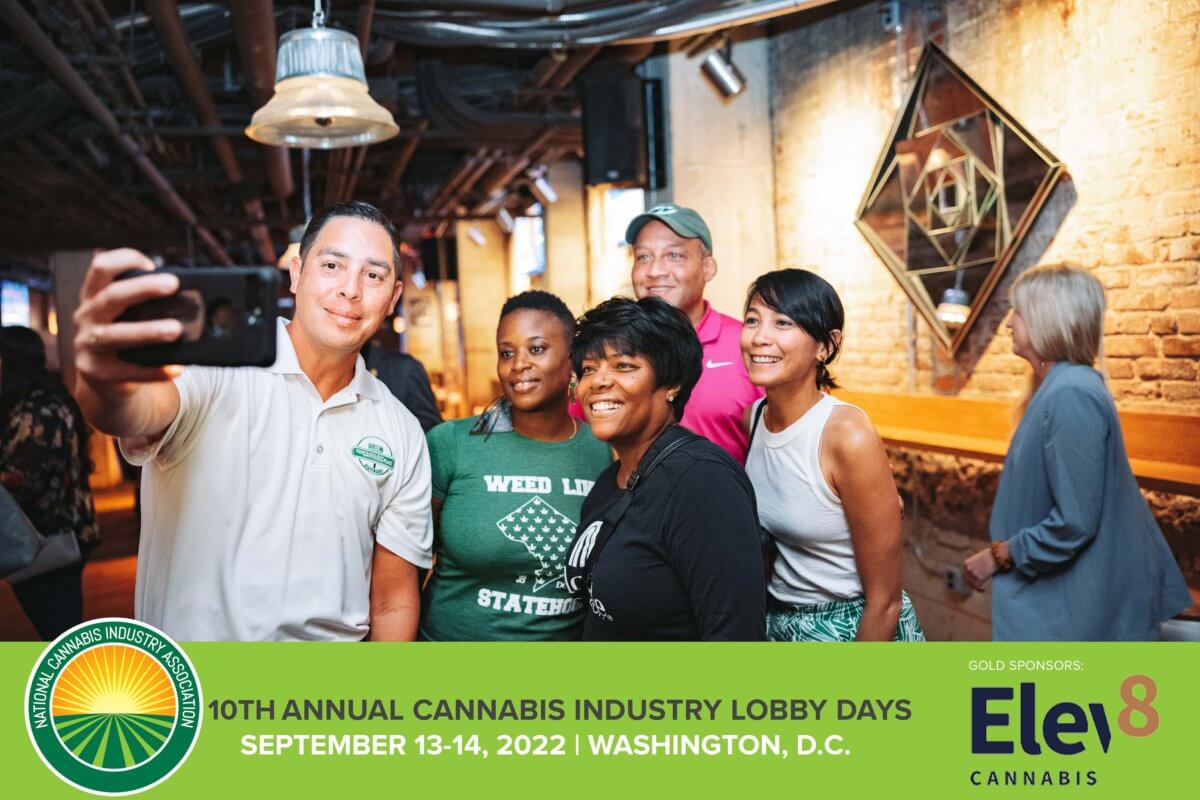

The NCIA DEI Delegation Reports Back from Lobby Days in D.C.!

by Mike Lomuto, NCIA’s DEI Manager

On September 13-14, Social Equity applicants and operators from around the country traveled to Washington D.C. as part of NCIA’s Lobby Days. Lobby Days provides the opportunity for NCIA members to speak directly with national lawmakers about the issues most important to small cannabis businesses – from SAFE banking to federal de-scheduling. This first-ever DEI delegation was supported by our members’ contributions to the Social Equity Scholarship Fund, and was the first of its kind – intentionally bringing diverse voices from our membership to Lobby Days.

Due to the pandemic, this was our first in-person Lobby Days since the launch of our DEI Program in 2019, and the launch of our Social Equity Scholarship Program in Spring of 2020. Since then, we have been coalescing our members’ diverse voices into clear perspectives and opinions on the direction of our industry. Something that our DEI Program is very proud of is that at this year’s Lobby Days we supplied talking points with the purpose of creating a proper impact.

Some of these talking points were sourced from the excellent white paper on SAFE Banking by the Cannabis Regulators of Color Coalition, which provides very thorough recommendations including: Requiring federal banking regulators to identify best practices to achieve racial equity in financial services; and Clarifying that cannabis criminal records are not an automatic red flag. Notably, this group which has some of its roots from NCIA’s very first Catalyst Conversation over two years ago, and its Treasurer, Rafi Crockett, now serves on NCIA’s DEI Committee.

The Social Equity applicants and operators comprising the delegation spoke directly to lawmakers on the kind of real changes we need for DEI and social equity to become a reality in our industry, in particular regarding SAFE banking. From their experience as professionals and advocates in the industry they were able to provide much-needed insight into how legislation impacts owners, operators, budtenders, and the social equity community in particular at the ground level. These conversations proved to be the missing link for a lot of these elected officials on Capitol Hill who stated their support for making a more equitable industry and righting the wrongs of the war on drugs, but lack real-life experience on the matter.

Here are some of the highlights from the delegation:

“My highlight was meeting with a CA legislative aide who is a fellow CA native and sincerely wanted to be updated on my progress and pain points. We all had a laugh about him agreeing to let me go into “the weeds” concerning the licensing process, pun intended.”

Raina Jackson, Founder & CEO PURPLE RAINA Self Care

“As I moved from meeting to meeting, one thing became crystal clear; there’s a knowledge gap that surrounds this plant, a gap fueled by learned behaviors, stigmas, pain, gain, and loss. This message rang clear to me from members and staff of both the senate and house…”

Toni MSN, RN, CYT, Toni

NCIA Education Committee and Health Equity Working Group

“From my experience, I learned that people make a difference. The people who make the laws don’t know everything and us providing information and answers can and may make that difference”

LaVonne Turner, Puff Couture, LLC

NCIA DEI Committee

“NCIA Lobby Days was an interesting peek behind the curtain of how the sausage is made in D.C. It became easier to see why some politicians seem so ill-informed about cannabis. Elected officials may themselves come from a state with draconian laws and politics about cannabis. Mix that with their staffers/advisors being recent college grads from other parts of the country with those same conditions, and you have a recipe for horrific policy. What was refreshing however was the amazing amount of knowledge that some of those staffers did possess both about cannabis policy and the plant itself. Not surprisingly they without fail worked for pro-cannabis congresspersons.”

Dr. Adrian Adams, CEO Ontogen Botanicals

NCIA DEI Committee – Subcommittee Regulation

“In each session, as I spoke about equity in underserved communities, the representative(s) appeared as it was the first time hearing the phrase Safe Equitable banking. Through their perplexed faces, I saw them registering that safe, equitable banking is needed.” – Toni

“I’ve never done something like this before sounds so cliche but it’s the best way to describe this eye-opening experience of speaking directly to Congressional staff about what it means to be a small business owner in the cannabis space. The challenges and hurdles that we have to deal with because of 280e and cannabis being a “controlled substance” are real and huge burdens to us as small businesses and owners of color. The lack of banking and financing is exponentially more damaging and difficult to black and brown communities because of our historic lack of fair and equitable access to this vital resource. This lobby days opportunity strengthened my resolve to be a loud voice for the Latino and black communities to ensure we have our seat at the table from this day forward!”

Osbert Orduña, The Cannabis Place

“Everyone we met with was compelled by the financial and public safety benefits that SAFE would offer under any form of cannabis decriminalization, from CBD with low-THC to adult consumption” – Raina Jackson

All in all, the consensus was that it was a valuable experience and folks would take the time to lobby again and encourage others to do the same. Lobbying in DC is one part of many strategies that have the potential to spark policy change at the federal level and without a doubt, getting a chance to speak personally to experienced industry professionals with a social equity lens was invaluable for the policymakers.

Next year we are pledging to double or even triple our DEI delegation. If you’d like to be a part of making this happen, we are already accepting sponsorships as we plan for 2023’s event, NCIA’s 11th Annual Cannabis Industry Lobby Days on May 16-18, 2022.

If you did not get a chance to read our blog post before the delegation left for Washington, D.C. to participate in NCIA Lobby Days as part of the first-ever Lobby Days Social Equity Scholarship delegation, you can read more here.

Member Blog: Payment Processing in the Cannabis Space – Part 2

America is a federation. As such, individual states have innumerable sovereign rights that supersede federal law. This may seem obvious, but in most countries, that’s not how it works. Whether they are democracies or not, often all rights emanate from the central government. When the central government says marijuana is illegal in such a place, specific regions or territories aren’t permitted to go their own way.

However, as a federation, the 50 states in the U.S. get to make up their own rules on a lot of material issues.

That’s why cannabis products containing more than .3% THC by volume can be legal in your state, but illegal, federally. And it is also why cannabis products containing .3% THC by volume or less can be legal, federally, but illegal in your state.

All this ambiguity gives the banks and card associations the vapors. And it goes a long way toward explaining why, nearly four years after the landmark Farm Bill, so few banks are willing to provide CBD businesses with merchant accounts.

Parenthetically, it’s also why, if you walk into your local Chase branch to open a simple checking account for your CBD or cannabis business, they will give you a lollipop and show you the door.

A Colorado Resident Walks into a Colorado Dispensary with a Credit Card…

Here’s a fair question: “If cannabis is legal in my state, and I operate a cannabis business in my state, why can’t I accept a credit card from a customer who is not only a resident of my state, but also somebody who got a credit card from a bank in my state?”

On those terms, it defies logic how any intrastate cannabis purchase would be a federal issue. Unfortunately, the movement of money from a Visa or Mastercard, or any U.S. credit card, occurs on a card association’s network, or rail. These rails are nationally interconnected, not siloed to a specific state or territory. So, even if a cannabis consumer lives in the apartment above a dispensary, heading downstairs to make a purchase with a credit card is a national transaction, and not a local one. And on those terms, it violates federal law.

Regional rails do exist outside of the card association networks. They connect banks to one another, and these are the rails that are leveraged for the non-cash transactions taking place at dispensaries around the country. Whether or not these rails are truly siloed, and not part of a national network, is, to say the least, the source of much legal, financial, and philosophical debate.

But Do I Even Need a Merchant Account?

It would be disingenuous to say that you need a merchant account to accept credit card payments. You don’t. There are several FinTech companies out there with names we all know and, generally speaking, trust to process payments on our behalf.

In the payments space, we refer to these third-party organizations as PSPs, or Payment Service Providers, or Payment Aggregators. With a PSP, a commercial enterprise doesn’t need its own merchant account. The PSP is allowing you, and thousands of other merchants, to share in the processing power of its merchant accounts and accept credit card payments on your behalf. In this case, you are what is called a ‘sub-merchant.’

However, the big PSPs, by and large, have been reticent about hopping aboard the CBD express. And there is little surprise there. These FinTech giants we associate with banking are, at their core, just software companies. To offer credit card processing, they need merchant accounts from Acquiring Banks, just like the rest of us. So the dearth of Acquiring Banks willing to work in the cannabis space affects them the same way it affects everyone else.

To date, only Square has thrown its hat in the ring, and an overwhelming number of CBD and hemp retailers have opted to go the Square route. Square is the most popular processing solution for CBD merchants for a couple of reasons. First, it’s easy to find. Searching “How do I begin accepting credit cards CBD” on Google nets mostly ads and review sites, but Square appears prominently. Parenthetically, I just entered that very search term, and Square appeared twice on page one.

Square, we always tell CBD merchants, is low-hanging fruit. Low-hanging fruit, by definition, should always be, and usually is, eaten first.

The near-universal recognition of Square also makes integration easier. The technologists that entrepreneurs hire to code their digital storefronts and websites have plenty of experience integrating the Square plugin for all manner of eCommerce businesses.

However, for the CBD retailer, there are important reasons to approach Square with caution, or, at a minimum, not to use Square without a backup processing option. Backup processing, or redundancy, is a must for everybody in a high-risk business, especially for CBD merchants using Square. It’s a bell we, at MobiusPay, sound often, as Square’s Set It and Forget It value proposition has proven a fiction for numerous CBD retailers.

The horror stories, reductively:

“Square shut me down.”

“Square is holding my money.”

“Square shut me down and is holding my money.”

When Square’s underwriters identify a compliance issue in a CBD retailer’s digital storefront, their processing is halted, and their funds are frozen — sometimes, indefinitely. Most problematic is that, owing to their size and dogged commitment to automation, Square does not excel at communicating with clients — even when it’s of vital importance.

Often, Square doesn’t disclose the cause of the account shutdown. This omission of details turns a precarious situation for the merchant into an existential crisis, and the larger the digital storefront, the bigger the problem it is. This is because, frequently, the compliance issue is a small one, like a broken link or an expired Certificate of Analysis. Depending upon the number of products in your shop, identifying the one problematic COA may be like finding a needle in a haystack. That’s doubly damning. Not only has processing stopped, but work has stopped, too — because now, it’s all-hands-on-deck. Everyone in the office is on a frantic scavenger hunt, trying to track down the one compliance issue (and for all you know, maybe there are two) that has caused all sales to halt.

That doesn’t happen when you have a merchant account.

Even without the threat of a halt in processing, though, merchant accounts will always be the smarter choice for CBD retailers. They simply offer greater flexibility, better rates, more stability, better throughput, and, perhaps most important of all, the marketing and strategy flexibility that a business needs to grow successfully.

This is not an indictment of Square. They deserve points for throwing their hat in the ring. They are good at what they do, and what they do good is provide a turnkey processing solution for low-risk brick & mortar and eCommerce merchants. The pet store, down the street from me, here in Philly, uses Square. When I’m picking up cat litter at the shop, I never think to suggest that she consider a merchant account. She doesn’t need it. Square was made for businesses like hers. It is ideal for low volume businesses operating in a routine business environment.

However, if you’re reading this, your business is facing challenges somewhat different from those faced by the pet store down the street — unless you specialize in CBD for pets, of course.

CBD businesses, as with all individuals and organizations in the cannabis space, stand at the vanguard. They are the tip of the spear in an inevitable plant medicine revolution.

Like square pegs — pun intended — in round holes, they don’t fit easily into Square’s steady-as-she-goes ecosystem.

On the other hand, establishing a merchant account is no picnic. Merchant accounts do not open like elevator doors. At their most reductive, merchant accounts are lines of credit, and lines of credit are established with a paper trail. There is an application to fill out. There are KYC protocols to follow. There are document requests and compliance checks. There is waiting for activation.

However, as someone who has spent many more years acquiring merchant accounts as a high-risk merchant than offering them to high-risk merchants, I can promise you that they are worth the wait and the effort, and that depending upon a PSP like Square for something as important as processing makes growth and success more difficult than it needs to be.

MobiusPay, Inc. is a U.S.-based global financial services organization that is committed to empowering individuals and businesses. For more than a dozen years, MobiusPay has leveraged state-of-the-art secure billing technology, long-standing relationships with financial institutions and award-winning customer support to provide merchant processing and payment solutions to brick and mortar and digital businesses around the world.

Todd Glider has been an e-Commerce leader since the start of the Internet age. He has an MFA in Creative Writing from the University of Miami, and has served as CEO for small and medium-sized technology companies in Spain, Austria and the United States. As our Chief Business Development Officer, Todd introduces MobiusPay’s suite of award-winning financial services to new industries, and implements the development strategies and key partnerships needed to bring value to new customers.

Service Solutions | 10.26.22 | Show Me the Money – The Current State of Cannabis Lending

NCIA’s Service Solutions series is our sponsored content webinar program which allows business owners the opportunity to learn more about premier products, services and industry solutions directly from our network of established suppliers, providers and thought leaders.

In this edition originally aired on Wednesday, October 26, 2022 we were joined by the experts from cannabis-focused financial institutions FundCanna, Safe Harbor Financial, and AVANA Companies to dive deep into the current state of cannabis lending with leading industry journalist John Schroyer of Green Market Report.

A decade after California and Colorado became the first adult use states, the regulated U.S. cannabis market encompasses over 70,000 cannabis-related businesses. Shockingly, most of those businesses still lack easy access to debt and other forms of growth and operating capital. From federal prohibitions and the impact of IRS regulation 280e, to state and local taxation issues, the costs of operating a regulated cannabis company continue to remain nearly unendurable.

Learn what may change in the coming six to 12 months so you’ll know how to access debt capital most cost-effectively in this ever evolving environment. No matter your place in the industry or the supply chain from cultivators, manufacturers, vendors, suppliers, distributors and retailers this conversation will provide the insights to meet your financial needs.

At the conclusion of the discussion our panel hosted a moderated Q&A session to provide NCIA members an opportunity to interact with leading minds from the financial services space, join today to contribute to future conversations!

Panelists:

Adam Stettner

Founder & CEO

FundCanna

Sundie Seefried

Founder and CEO

Safe Harbor Financial

02:13 – Equity vs. Debt: With equity dried up, should cannabis companies be looking at debt financing to grow now?

07:28 – Equity vs. Debt: What do borrowers need to do before approaching a debt provider (vs. an equity provider)?

13:25 – Equity vs. Debt: What can cannabis companies or entrepreneurs do to improve their overall credit worthiness prior to seeking capital?

17:16 – How has the interest rate increases by the Federal Reserve impacted capital markets (and the industry at large) in 2022?

26:07 – Audience Q&A: “If there’s “no reason not to have banking” for your cannabis business how can I easily (and inexpensively) establish and maintain a compliant bank account?”

28:56 – Lending: What significant lending challenges are your clients currently facing within the industry?

33:56 – Lending: What advice can you provide business owners for evaluating lenders that you should (or shouldn’t) work with and tips for avoiding predatory lending practices?

39:05 – Cannabis Reform: What impact do you expect President Biden’s recent announcement will have on the industry?

49:32 – Audience Q&A: “Are your financial institutions planning to offer lending and banking services in New York, New Jersey and other new markets?”

51:42 – Audience Q&A: “With the mindset of “Investors are betting on the Jockey not the Horse.” What type of CEO or founding team would be a red flag or not a viable investment?”

55:19 – Audience Q&A: “How can I start to shift my retail company from being primarily a cash-only business?”

1:05:03 – NCIA Member Appreciation Credit Sequence

Sponsored By:

Video: NCIA Today – Thursday, October 22, 2022

NCIA Director of Communications Bethany Moore checks in with what’s going on across the country with the National Cannabis Industry Association’s membership, board, allies, and staff. Join us every other Thursday on Facebook for NCIA Today Live.

Member Blog: Payment Processing In The Cannabis Space

There is a lot of confusion about payment processing in the cannabis space because payment processing is somewhat confusing to begin with, and because, in the cannabis space, ambiguity is a way of life.

The title of this very blog post could, realistically, seem misleading to some.

So, to be clear, when I say, “Cannabis Space,” I mean the entire industry — from plant-touchers (CBD included) to the ancillary businesses built up around it.

The passage of the 2018 Farm Bill marked an exciting new chapter for the industry. Suddenly, CBD, or, more specifically, any ingestible cannabis product containing .3% THC or less by volume, was classified as hemp. And since it is marijuana, and not hemp, that is defined as a Schedule I substance under the United States Controlled Substance Act, the Farm Bill, technically, made products like CBD as legal as cow milk — federally, anyway.

The upshot of this new classification is that now, at least some players in the cannabis space can market their products to a national base of consumers and clients, and they can do so by accepting credit cards as payment.

However, the myriad Acquiring Banks across the United States have not exactly jumped for joy at the prospect of providing credit card processing in the form of merchant accounts to CBD retailers. Reticence rules. CBD is considered high risk, and four years on, only a handful of them have thrown their hat in the ring.

Jargon Alert I: Acquiring Banks and Issuing Banks

In merchant processing parlance, banks fall into two categories: Acquiring Banks and Issuing Banks. Acquiring Banks, or, Acquirers, provide merchant processing accounts to businesses wishing to accept credit card transactions. Issuing Banks, short for Card Issuing Banks, are banks that offer branded payment cards directly to consumers. For example, if your bank has ever offered you a Visa card, it is an Issuing Bank (not that it couldn’t also be an Acquiring Bank, too).

Jargon Alert II: CBD is ‘High Risk’

CBD is deemed high risk by the card associations (i.e., Visa, MasterCard, American Express), and when the card associations deem a product or industry high risk, most Acquiring Banks tap out. This is because financial institutions are, by nature, risk averse (subprime mortgage crisis notwithstanding).

So let’s talk for a minute about risk. High risk, that compound term, is a truncation of a longer phrase: ‘Higher risk of fraud or chargebacks.’

Why are CBD products at higher risk of fraud? It’s impossible to say for sure since the Visas and MasterCards of the world are publicly traded companies with their own trade secrets and IP, but there are several characteristics unique to CBD, or any cannabis product now federally legal, that likely figured into that decision.

Those FDA disclaimers that CBD retailers must print or paste on all product packaging and webpages are as good a place as any to start. They are mandatory because none of the benefits assigned to CBD have been clinically proven. There just isn’t enough data or testing at this point, and no big story there. That’s what happens when you demonize a plant for 100 years.

Consequently, from the perspective of the FDA, and the card associations, by extension, consumers are making CBD purchases with baked-in expectations based, exclusively, on word-of-mouth advice and anecdotal data. That’s a recipe for dissatisfied customers. And dissatisfied customers tend to charge back transactions.

The card associations, and the banks who provide merchant accounts, worry incessantly about fraud and chargebacks.

Too Close for Comfort

Dissatisfied customers aside, there are onerous legal nuances that make the prospect of boarding cannabis merchants, even those selling products that are federally legal, daunting for banks.

Selling a product with .31% THC across state lines is felonious. It is a federal offense. Violating a law like that could get a bank’s charter revoked, or, at a minimum, result in massive fines.

On the other hand, selling a product with .30% THC across state lines is 100% federally legal. As stated above, safe as milk, federally.

That is a heck of a distinction. If any product contains more than .3% THC by volume, it is ‘marijuana’ in the eyes of the federal government. From the perspective of the banks, that’s a little close for comfort. Furthermore, banks don’t operate laboratories. They must rely on testing data presented to them in the form of third-party lab reports — Certificates of Analysis or COAs for short — to verify that the products being sold are federally legal.

The last thing an Acquiring Bank wants to do is violate a federal law EVER. It could result in a loss of their charter, lawsuits, and massive fines. And it’s important to keep in mind that the Acquiring Banks out there offering merchant accounts to CBD retailers are not giant, publicly traded institutions like Bank of America or Wells Fargo. They tend to be much smaller, and therefore, have infinitely smaller war chests for court cases.

Still, separating the federally legal Tier I cannabis product from the federally illegal Tier I cannabis product should be pretty cut-and-dry. If the product you’re selling is .3% THC by volume or less, it is exempt from the Controlled Substance Act (CSA). If that threshold is documented in the product’s Certificates of Analysis (COA), you ought to be able to sell it.

Unfortunately, it’s not that simple. When bank underwriters look at percentages of Delta 8, Delta 9, and Delta 10 on the COAs that cross their desks, they’re frequently at sixes and sevens trying to figure the whole thing out.

From the perspective of the 2018 Farm Bill, a cannabis product is hemp if it contains .3% Delta-9 THC or less by volume, but what everybody says is “.3% THC or less by volume.” Consequently, when the compliance officer at the bank is performing her due diligence by inspecting the COAs corresponding to each product, she may encounter a lot of crooked numbers, and she may blanch at the results.

Those results, often, look something like the following:

00.195% D9-THC

52.475% d8-THC.

Federally, the Delta-9 threshold is the only threshold that matters. The 2018 Farm Bill says as much, and the 9th Circuit Court of Appeals in California affirmed it in a ruling this past May. Therefore, in the example above, the Delta-9 threshold has not been crossed. It’s not even close. It is textbook HEMP, even if the Delta-8 threshold is off the charts.

However, if the compliance officer was provided the remit, “.3% or lower,” he’s likely to look at this and say, “Fail,” without realizing that the Delta-8 THC information is irrelevant as far as federal law goes.

Complicating the underwriting further is the fact that there is, to date, no standard template for COA reports. Every lab presents them differently. Bank compliance officers rarely moonlight as scientists. Like most of us, these CBD COAs are probably the first lab reports they’ve looked at since high school chemistry.

Furthermore, the banks can set their own rules. They don’t have to board CBD merchants. Few do, and those few that do have their own standards and practices.

Todd Glider has been an e-Commerce leader since the start of the Internet age. He has an MFA in Creative Writing from the University of Miami, and has served as CEO for small and medium-sized technology companies in Spain, Austria and the United States. As our Chief Business Development Officer, Todd introduces MobiusPay’s suite of award-winning financial services to new industries, and implements the development strategies and key partnerships needed to bring value to new customers.

MobiusPay, Inc. is a U.S.-based global financial services organization that is committed to empowering individuals and businesses. For more than a dozen years, MobiusPay has leveraged state-of-the-art secure billing technology, long-standing relationships with financial institutions and award-winning customer support to provide merchant processing and payment solutions to brick and mortar and digital businesses around the world.

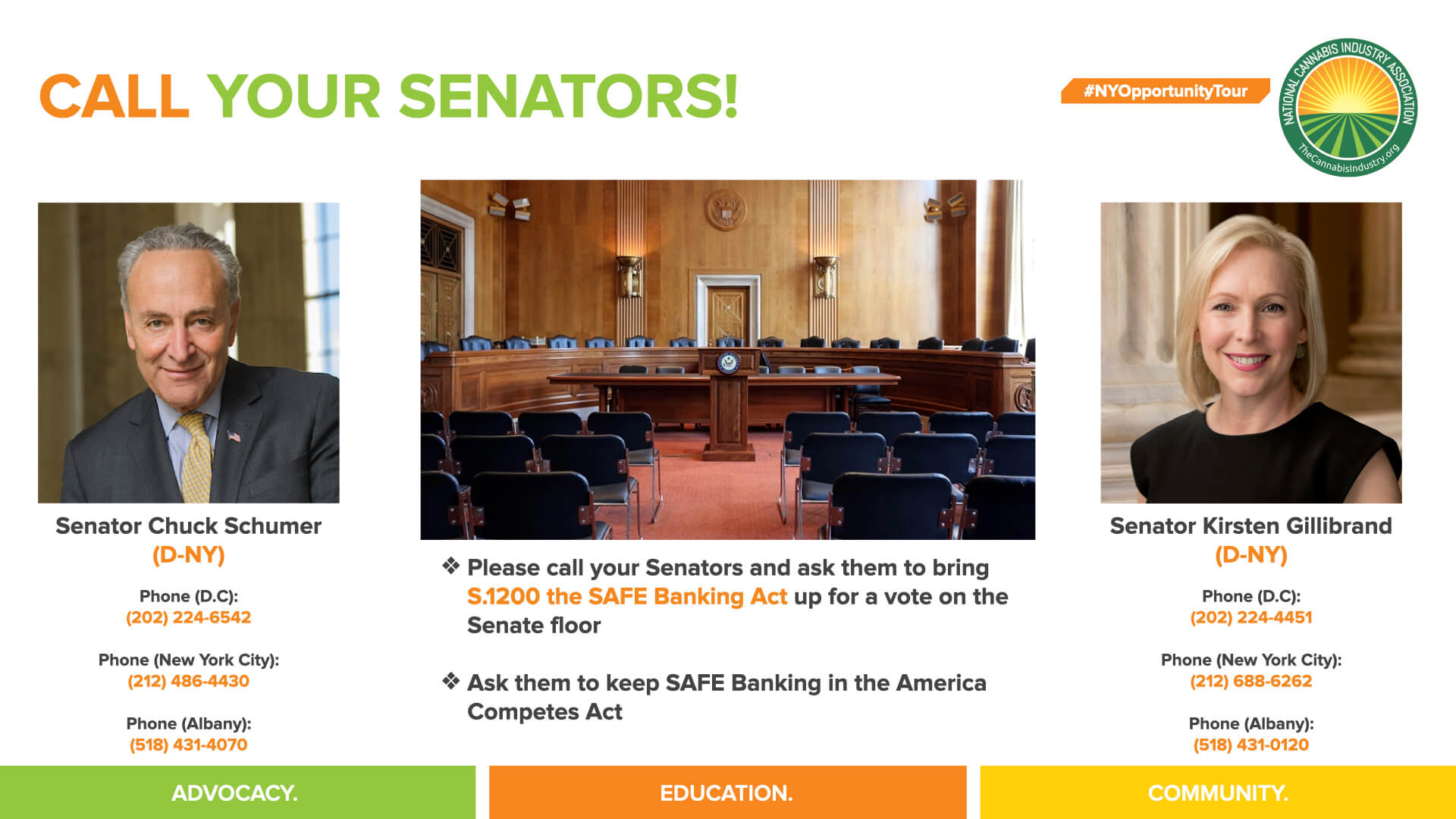

Biden’s Announcement, SAFE Banking, and the CAOA

Photo By CannabisCamera.com

By Michelle Rutter Friberg, NCIA’s Deputy Director of Government Relations

October has been a mixed bag in Washington, D.C. in terms of cannabis policy: there hasn’t been much news from Capitol Hill, but the Biden Administration shocked everyone when they made a big announcement earlier this month. As we draw nearer to the midterm elections in November (don’t forget to register!), let’s take a look at where things stand currently:

On Capitol Hill:

SAFE Banking Act

The SAFE Banking Act (S. 910) has been held up in the Senate for more than a year now. Many Senate Democrats (including Leader Schumer) have been pushing for changes to the bill to create a “SAFE +” bill that includes justice-focused provisions. As with all things in politics, a delicate balance must be kept in order to reach 60 votes in the hyper-partisan Senate.

The good news: Leader Schumer and other Democrats have been in negotiations with lead-Republican co-sponsor Sen. Steve Daines (R-MT) and others to determine what “SAFE +” could look like. Those discussions have been occurring for a few weeks now and will continue.

The bad news: those negotiations are taking time. As a result, you shouldn’t expect any legislative movement to occur until after the midterm elections.

There’s also the National Defense Authorization Act (NDAA) to consider. The House passed and sent the FY2023 NDAA to the Senate months ago and the large package did include the language of the SAFE Banking Act (as currently written). It’s unclear how the SAFE+ negotiations may impact cannabis banking’s chances in the NDAA: Leader Schumer could make sure the language is not in the NDAA if he feels confident about SAFE+’s chances.

CAOA

Unfortunately, there’s no substantive news regarding the Cannabis Administration and Opportunity Act (CAOA), or comprehensive reform broadly on Capitol Hill right now. While NCIA and others continue to push for descheduling and responsible regulations from Congress, the upcoming election and Senate timeline have taken precedent. It’s unlikely that CAOA will move this legislative session given the number of legislative days left in the year.

From the Administration:

Earlier this month, President Biden made an unprecedented announcement that his administration would begin the process for the pardoning of thousands of people with nonviolent marijuana use or possession convictions, and would begin the process of working with the Department of Health and Human Services to reclassify marijuana from a Schedule I drug in the Controlled Substances Act.

This announcement comes on the heels of NCIA’s successful 10th Annual Cannabis Industry Lobby Days held in mid-September, where 100 cannabis industry professionals, representing small and medium-sized businesses including social equity operators, met with more than 100 Congressional offices to discuss barriers faced by the industry stemming from marijuana prohibition.

It’s no coincidence that when NCIA members show up to D.C., big things happen! Make sure to stay informed as we head towards the lame duck session via our newsletter and social media platforms and don’t forget to register for NCIA’s upcoming 11th Annual Cannabis Industry Lobby Days in May 2023!

Member Blog: Understanding D&O Coverage for the Cannabis Industry

Cannabis industry companies face more and sometimes greater threats than non-cannabis companies because of the emerging nature of the market, a complex regulatory landscape, and investor relations.

Because of the challenging landscape, cannabis organizations have some unique risks they may face while running their businesses including:

High investor expectations and limited access to capital

The federal status of cannabis

Varying trade practices from state to state

Lack of bankruptcy protections

Increased merger & acquisition activity

State-by-state licensing requirements

Cannabis-specific local, state, and federal tax laws

Private companies in the cannabis market face threats from many directions, business leaders need to protect their assets and be able to attract top potential directors and officers to their company. The increased exposure to litigation includes disputes such as shareholder disagreement, allegations of mismanagement, and actions by regulatory agencies. Lawsuits can be levied against a cannabis company’s directors and officers and create risk for these individuals and the cannabis company. One way to help mitigate the risk of future losses is by getting Directors & Officers (D&O) insurance.

Directors & Officers Liability Insurance, or D&O, is a coverage designed to protect an organization and its directors and officers from being held financially responsible for legal action taken by an organization’s employees, vendors, customers, or shareholders. D&O insurance primarily covers the costs associated with an allegation and wrongful lawsuits including defense costs, legal fees, and settlements. D&O insurance does not cover illegal acts.

What is generally covered with D&O Insurance?

Coverage varies, but typically D&O policies encompass three main insuring agreements: Side A, Side B, and Side C. The structure of a policy depends on which of these three insuring agreements are included. Each insurance agreement can specify a distinct insured party.

Side A

When indemnification is either barred by law or an organization is insolvent and unable to indemnify, the individual director and/or officer can be at risk and responsible for losses. Side A offers protection for an individual’s personal assets in case of a non-indemnifiable loss.

This offers an extra layer of protection if a company is unable to pay for losses in cases like bankruptcy or regulatory investigations.

Side B

Side B provides reimbursement for the defense of a corporation for expenses incurred while defending its organization’s directors and officers. This protects a company’s corporate assets.

Side C

Side C, also known as entity coverage, protects a corporation’s interests if a corporation is named in a suit alongside directors and officers. This coverage provides entity asset protection for legal fees, settlements, or other related costs for covered claims, subject to a policy’s terms and conditions. Side C has a broader implication for private and non-profit companies, as Side C typically only protects public companies from securities claims.

When should you have conversations with your broker?

Buying the correct insurance coverage can be a confusing undertaking for Cannabis business owners. Insurance Agents/Brokers are critical in helping their clients navigate this process and serve as trusted advisors to find the best fit for their client’s businesses. This article aims to demonstrate the differences between admitted and non-admitted policies and their implication for your Cannabis clients.

Running a cannabis company can be challenging and often requires leveraging an insurance broker that understands the cannabis industry. Some questions to help decide when to have conversations about Directors’ & Officer’s coverage include:

Are you planning on taking on new investors during the next 12 months? As you take on investors, it increases your risk profile as shareholders can sue on their own behalf or in the name of the corporation. These suits may allege a breach of a director’s or officer’s fiduciary duties of care and loyalty to the company. This type of litigation can result in issues of conflict between the shareholders, the company, and the individual director and officer defendants.

Are you hoping to hire an executive or team of executives within the next 6-12 months? As the cannabis market begins to expand, cannabis companies are looking to attract top talent and at the executive level, D&O coverage is an advantage to many candidates.

What is an example of a recent lawsuit within the cannabis industry?

Private companies in the cannabis market face threats from many directions. Business leaders need to help protect their assets and be able to attract top potential directors and officers to their company. Below is a recent example of a lawsuit from the Cannabis industry:

PH Invesco LLC v. Pure Harvest Corporate Group Inc et al., case number 1:22-cv-00094, in the U.S. District Court for the District of Wyoming. Colorado-based cannabis farm Pure Harvest Corporate Group Inc. was hit with a suit by a lender that claims the farm and its CEO breached the terms of a $4,000,000 line of credit it took out. (2022)

This information is provided for general informational purposes only and is not intended to provide individualized business, insurance, or legal advice. All descriptions, summaries, or highlights of coverage are for general informational purposes only and do not amend, alter or modify the actual terms or conditions of any insurance policy. Coverage is governed only by the terms and conditions of the relevant policy.

Jon Spratt leads Greensite Insurance, a specialty MGU providing boutique insurance coverage to the rapidly expanding Cannabis industry. Greensite launched in 2021 and is partnering with agents/brokers to help better protect their clients. Jon also runs a business accelerator that develops and launches new programs on behalf of Aon programs.

Greensite Insurance Services is the brand name for the brokerage and program administration operations of Affinity Insurance Services, Inc. a licensed producer in all states (TX 13695); (AR 100106022); in CA & MN, AIS Affinity Insurance Agency, Inc. (CA 0795465); in OK, AIS Affinity Insurance Services Inc.; in CA, Aon Affinity Insurance Services, Inc., (CA 0G94493), Aon Direct Insurance Administrators and Berkely Insurance Agency and in NY, AIS Affinity Insurance Agency

Video: Insights From NCIA’s 10th Annual Lobby Days

“I think it was really successful on all fronts.

Whether it be the networking aspect, VIP access to key decision makers, or just the ability to get to know people both fellow cannabis business owners and congressional leaders.

Lobby Days was a perfect example of really putting the membership into work and seeing what it is that you pay for.” – Chris Jackson, NCIA Board Member

Committee Blog: Four Tips for Cannabis Businesses to Maintain Cannabis Friendly Financial Services

by Kameron Richards and Steven Schain Members of NCIA’s Banking & Financial Services Committee

Obtaining legitimate, cannabis-friendly financial services is among the cannabis industry’s biggest hurdles. Obtaining financial services is challenging for dispensaries, marijuana grows, and testing labs but it could also be an obstacle for non-plant touching businesses or individuals engaged in the cannabis industry. Without cannabis-friendly financial services, individuals and businesses related to the cannabis industry are deprived of simple financial solutions, like checking accounts, resulting in large amounts of cash being held at company facilities or the operator’s residence, posing significant risks.

Because only a small amount of insured banks and credit unions offer cannabis businesses financial services, finding cannabis-friendly financial services offered by FDIC or NCUA/CUNA institutions is challenging, and following a certain approach may fortify the longevity of a relationship with a financial institution.

Know Your Company Information and Banking Needs

Thorough onboarding initiates the account opening process for cannabis companies seeking financial services. Cannabis-friendly financial institutions exercise enhanced due diligence at account opening for compliance purposes, which will be further discussed in this article.

Financial institutions may require information on state licensing, corporate structure, and governance documents. Institutions generally collect information regarding the company’s underlying products and whether those products or services violate The Controlled Substances Act (“CSA”). Information collected during the onboarding process often determines the institution’s fee, risk-based categorization, and willingness to provide financial services to a particular cannabis company.

During the onboarding process, cannabis companies should determine if the financial institution provides all services necessary for its specific operation. The services offered by cannabis-friendly financial institutions may vary based on its risk tolerance.

Know Compliance Requirements and Cannabis-Specific Programs

Financial institutions serving the cannabis industry must comply with The Bank Secrecy Act’s (“BSA”) requirements set forth in the Treasury Department’s Financial Crimes Enforcement Network’s (“FinCEN”) BSA Expectations Regarding Marijuana Banking (FIN-2014-G001) (“FinCEN Guidance”). To mitigate the possibility of money laundering, institutions assemble extensive risk-based BSA programs centered around assessing the risk of each cannabis account and detecting and reporting “Red Flags” set forth by FinCEN Guidance.

To understand the constraints under which financial institutions are forced to operate, cannabis companies should familiarize themselves with relevant cannabis industry regulatory guidance and, if possible, structure its operations to ease its financial institution’s compliance efforts. Further, cannabis companies should understand any contractual terms and operation of any specific cannabis programs required by its financial institution (e.g., participation in cannabis-specific programs to support loan approvals, liquidity management or the coordination of cash courier services).

Know the Risk-Based Approach

FinCEN Guidance requires institutions to perform enhanced due diligence on cannabis companies, because the risk category of each cannabis account is determined during the onboarding process, institutions are required to obtain corporate and state licensing documentation and detect any negative news on the potential account signers and the business.

Because there is no mandated risk-based structure for institutions to follow, it is critical that cannabis companies know its institution’s specific risk-based structure. Further, if a cannabis company is utilizing more than one institution, it should understand that each institution’s risk-based categorization may have specific factors or considerations. Some institutions use a tiering structure (which can vary by institution) or make this determination based on the direct or indirect relationship that the account’s source of funds has with cannabis prohibited by the CSA. An institution’s risk-based categorization could determine an account holder’s compliance obligations or eligibility for financial services such as lending, treasury services, payment processing, and 401(k)/retirement solutions.

Know What Could Cause Account Termination

After completing the onboarding process and placing cannabis accounts in the requisite risk profile (which may vary among institutions), institutions are obligated to conduct ongoing enhanced due diligence on cannabis accounts in accordance with the risk each account poses.

This enhanced due diligence encompasses staying abreast of corporate changes, confirming that all licenses are up to date and conducting periodic negative news checks that indicate FinCEN Guidance “Red Flags.” It can also include a litany of happenings that cannabis account holders may not be aware of. While cannabis account signers may be compliant, without any negative news on them or their business, their institution could also close an account due to adverse information from tax and state licensing authorities or wrongdoing by employees or vendors. Cannabis account holders should also be aware of transactions prohibited by its institution’s policies and procedures like commingling funds between non-plant touching and plant touching accounts or transferring funds to and from vague accounts at unaware institutions unwilling to serve the cannabis industry.

Cannabis account holders with multiple relationships should be aware that each institution’s closure protocol may vary in response to adverse information or conducting transactions prohibited by internal policies and procedures (account termination terms are often contained in the depository agreement between the institution and cannabis account holder).

Conclusion

Beyond assisting a business’ core functioning, maintaining relationships with legitimate financial institutions leads to strategic advantages for a cannabis company and its owners and operators, like financing or payment processing.

Further, because FinCEN requires institutions to monitor and report cannabis account transactions and file a Suspicious Activity Report (SAR) when a cannabis account is opened or closed or if “Red Flags” are detected; cannabis companies can protect their accounts and businesses by knowing applicable laws and regulations and their institution’s cannabis-specific programs’ policies and procedures.

Social Equity Members Head to D.C. to Lobby for A More Inclusive Industry

by Mike Lomuto, NCIA’s DEI Manager

NCIA is proud to announce that for the first time, thanks to the support of our members, we have awarded nine Lobby Days Equity Scholarships to support our Social Equity members with travel expenses to attend NCIA’s Lobby Days in Washington, D.C., on September 13-14. These Social Equity applicants and operators from around the country are leaders and active contributors to NCIA’s Sector Committees, our DEI Initiatives (particularly policy-related ones), and to advocacy efforts in their local and/or state municipalities.

Lobby Days provides the opportunity for NCIA members to come together to advocate for the issues most important to small cannabis businesses — from SAFE Banking to federal de-scheduling — and to share their personal stories with national lawmakers.

Our delegation includes:

Dr. Adrian Adams, Ontogen Botanicals CBD Ambrose Gardner, Elev8 LaVonne Turner, Puff Couture Michael Diaz-Rivera, Better Days Delivery Osbert Orduña, The Cannabis Place Raina Jackson, Purple Raina Toni MSN, RN, CYT, Toni

We asked our DEI delegation why attending Lobby Days was important to them. Here are some of their responses:

“I want our elected officials to hear my story which gives a voice to so many others, who like me, grew up in areas that have disproportionately borne the brunt and weight of cannabis enforcement. Children and young adults, whose only crime was being poor and of color, faced the indignity of being stopped and frisked hundreds of times. Now after paying the ultimate entry price, we can not get in the door of the cannabis industry because of a lack of banking and lending opportunities that continue to shut us out of the cannabis market.

The de-scheduling of cannabis, the passing of SAFE Banking, or the repeal of IRC 280E all would immediately increase the opportunities for small cannabis businesses like mine to have a true opportunity for success, growth, and economic empowerment of our communities.”

– Osbert Orduña, The Cannabis Place

“As the industry grows and moves towards federal legalization, our elected officials must hear constituents’ voices. It’s important that my energy, face, and voice are present, representing the need for safe banking, health equity, and policies that support federal legalization. As states continue to legalize adult recreational cannabis usage, there will be an increased need for cannabis health equity to address the social, political, and economic conditions in underserved communities.

I’m committed to increasing awareness of the importance of education, employee retention, and community wellness in these communities.”

– Toni MSN, RN, CYT, Founder of Toni NCIA’s Education Committee & Health Equity Working Group

“I have begun to work on lobbying at a local level. Federal legalization, descheduling, decarceration, social equity, health equity, and safe banking are some of the areas that I would like to learn how to lobby for at the national level.”

– Michael Diaz-Rivera, Owner/Operator, Better Days Delivery

“We should not stop at using the SAFE Banking Act merely to provide legal and regulatory protection for financial institutions. That will enable, but not ensure, increased banking services for minority-owned cannabis and hemp companies.

As the regulatory gaps between state and federal governments are addressed, there must be mechanisms to prevent predatory practices while opening access to capital.”

– Dr. Adrian Adams, Ontogen Botanicals CBD

It is important to the NCIA, and its membership for Main Street Cannabis to continue to develop in as diverse, equitable, and inclusive a manner as we can achieve. As the industry has thus far failed at creating tangible Social Equity, it’s important to ensure our efforts this September to include these voices and the communities they represent.

This is where the DEI delegation comes in.

As the official DEI delegation, the Lobby Days Equity Scholarship recipients will provide a foundational understanding of matters related to DEI in the industry for all NCIA members present at Lobby Days. The DEI delegation will ensure that there are members present speaking up on matters of DEI from within an important national trade association and within the context of Main Street Cannabis.

NCIA’s Government Relations team has organized a full day of meetings with Lawmakers and their Offices. New citizen lobbyists will receive online training before the event and are grouped together with experienced industry leaders who can help them find their voice. There will be an opening networking reception for all attendees, and a closing event featuring some of NCIA’s most important allies in Congress.

We are still accepting sponsorships to fully fund Lobby Days Equity Scholarships to ensure our recipients have their travel and lodging expenses covered while in Washington, D.C. Contact MikeLomuto@TheCannabisIndustry.org for more information.

Let’s keep building a better industry together, as we bring our voices to Washington, D.C.

Video: Defending Main Street Cannabis Businesses

As the only national advocate for small and mid-sized cannabis businesses, NCIA works every day to advance policy reforms favorable to the whole industry — not just the wealthiest few. Hear from NCIA Board Members why our mission and advocacy work is crucial to defending the interests of everyday businesses in the cannabis industry.

We are Main Street Cannabis, not Wall Street Cannabis.

Become a member of NCIA today so that everyone can benefit from cannabis legalization — not just the wealthiest few.JOIN NCIA TODAY

Joining NCIA ensures that your interests are heard in our nation’s halls of power as the rules for national legalization are written. We’re also the only full service trade association in the industry, which means that our members enjoy unparalleled ROI and benefits to help them thrive in an increasingly challenging environment.

Video: NCIA Today – Thursday, August 25, 2022

NCIA Director of Communications Bethany Moore checks in with what’s going on across the country with the National Cannabis Industry Association’s membership, board, allies, and staff. This week Bethany is joined by NCIA CEO Aaron Smith to talk about the importance of having your voice heard on Capitol Hill at our upcoming 10th Annual Cannabis Industry Lobby Days on September 13-14. Join us every other Thursday on Facebook for NCIA Today Live.

This is your chance to unite with other NCIA members to advocate for the issues most important to small cannabis businesses – from SAFE Banking to federal de-scheduling – and to share your personal stories with national lawmakers who need to hear from Main Street Cannabis businesses.

Watch this video to hear from NCIA’s CEO and Co-founder, Aaron Smith, about why you should attend this most impactful and crucial event next month. Not yet a member? Join today and then make your plans to join us in D.C.

Behind Closed Doors: NCIA at CANNRA’s June Conference

The discussion about the future of cannabis legalization is ongoing, to say the least. Recently, Cannabis Regulators Association (CANNRA) held a two-day conference in early June to gather Marijuana government regulators, trade associations, and businesses. The Cannabis Regulators Association (CANNRA) is a national nonpartisan organization of government cannabis regulators that provides policymakers and regulatory agencies with the resources to make informed decisions when considering whether and how to legalize and regulate cannabis.

Representatives from NCIA participated in the conference – NCIA Board Members Khurshid Khoja (Chair Emeritus) and Michael Cooper (Board Secretary), and we caught up with them in this blog interview to better understand the goals and outcomes of the event.

From a bird’s eye view, what was the overall goal of this conference?

MC: The conference was an opportunity for regulators from around the nation to hear directly from stakeholders on the current and future challenges that face these markets and different models of regulation to tackle them.

KK: I’ll add that our own goals, as the current Policy Co-chairs for NCIA, were to better understand the priorities of state and local cannabis regulators across the country, and anticipate future developments in cannabis policy early on, so we could take that back to the NCIA membership and the staff – especially Michelle Rutter Friberg, Mike Correia, and Maddy Grant from our amazing government relations team.

Let’s talk about who was invited to participate in these panel discussions. From cannabis industry associations to those who regulate cannabis, who else was there?

KK: Michael and I each spoke on a panel. The other speakers included reps from federal trade associations, lobbyists, vendors, and ancillary companies who were helping to underwrite the event (along with NCIA). Given that CANNRA is a non-profit that doesn’t receive any funding from their member jurisdictions, and has a single paid full-time staff member, I thought they were still able to obtain a fairly diverse and interesting set of speakers at the end of the day – including NCIA Board and Committee alums Ean Seeb, Steve DeAngelo, Amber Senter and David Vaillencourt (representing the Colorado Governor’s Office, LPP, Supernova Women and ASTM, respectively), as well as folks from Code for America, Americans for Safe Access, and the Minority Cannabis Business Association, U.S. Pharmacopeia, NIDA, the CDC, and the Alcohol and Tobacco Tax and Trade Bureau, representatives of the pharmaceutical, hemp, tobacco and logistics industries, and public health officials.

Were there any organizations or sectors of the industry that were not in attendance, whether they weren’t invited or just didn’t participate, and why is it important to note the gaps of who was not represented?

MC: No licensed businesses were invited. Instead, organizations that represent industry members were invited. As a result, we felt it was crucial to inform these discussions with the perspective of the multitude of small and medium-sized businesses otherwise known as Main Street Cannabis that have built this industry and continue to serve as its engine.

KK: Sadly, we did not have an opportunity to hear from members of the Coalition of Cannabis Regulators of Color. I can’t speak to why that was, but it was unfortunate for us nonetheless. And while we had some public health officials there, I know that CANNRA Executive Director Dr. Schauer would have preferred to see more of them in attendance.

Across the spectrum of policy and regulations and legislative goals, what topics were covered in the panel discussions across the two-day conference?

KK: We covered a ton, given the time we had, including the federal political and policy landscape; interstate commerce; the impact of taxes on the success of the regulated market; social equity and social justice; preventing youth access; regulation of novel, intoxicating and hemp-based cannabinoids; the prospects for uniform state regulations; technological solutions to improve compliance and regulatory oversight; and delivery models.

What information or perspectives did NCIA bring to the panel discussions that were unique from other participants? What does NCIA represent that is different from the other voices at the event?

MC: There really are a wide variety of perspectives on how best to regulate this industry. We felt it was essential that NCIA give a voice to Main Street Cannabis, the small businesses that so many adult-use consumers and medical patients rely upon. We emphasized, for example, that these are often businesses that cannot simply operate in the red indefinitely, but provide essential diversity (in the background and life experience of operators as well as in product selection and choice). NCIA wants to make sure that the future of cannabis isn’t simply the McDonalds and Burger Kings of cannabis. There are times when consumers want that, but there are also times when they want something unique and different. And it’s crucial that policy not destroy the small and medium-sized, frequently social equity-owned, businesses that provide those choices.

What else was interesting to you about this gathering of minds? Were you surprised by anything, or was there anything you heard that you disagreed with?

MC: There are a ton of different perspectives and approaches to cannabis, and that’s no surprise to anyone who has followed these issues closely because the tensions are very clear in the policy debates that are ongoing.

As the voice for the industry, we sought to urge an approach grounded in reality. Americans want these products. That’s clear from the ballot box and public polling. The question should be about how to encourage Americans to purchase regulated, tested versions of these products.

KK: There was definitely stuff we didn’t agree with – some of it from folks that we otherwise largely agree with. For example, our good friend Steve Hawkins of the USCC shocked a few of us in the audience when he seemed to indicate some receptivity to re-scheduling cannabis on an interim basis, rather than moving to de-scheduling immediately. I think that while rescheduling may benefit scientific research and pharmaceutical development, it could ring the death knell for Main Street Cannabis businesses. NCIA has consistently advocated for de-scheduling rather than re-scheduling.

After two days of panels, did anything new come through these discussions, or were any accomplishments achieved?

KK: I think there’s a growing recognition that addressing social equity solely through preferential licensing and business ownership for the few isn’t enough and that the licensing agencies and regulators that execute social equity policies have a very limited (and often underfunded) arsenal to comprehensively redress the harm caused by federal, state and local governments prosecuting the war on drugs. In my remarks, I said it was time for us to start discussing additional forms of targeted reparation and had a number of regulators approach me afterward to continue the discussion. Candidly, I expected my remarks to fall on deaf ears. They didn’t. That was very encouraging.

MC: There was definite progress. At the end of the day, these cannabis regulators are working hard to try to get this right. But in such a new area, and with so many competing perspectives and voices, their job isn’t easy. We were heartened to see the level of engagement from regulators on these points, including follow-ups to get more information on some of the pain points we identified for small and equity businesses in the industry.

It was definitely rewarding to provide NCIA and our members’ perspectives in a forum like this, and we’re looking forward to continuing to further strengthen NCIA’s relationship with CANNRA and regulators around the country.

Member Blog: Trials and Tribulations – Compliance for Banking

There are not a lot of financial institutions out there that support cannabis, so finding the right one is important. What is also important is to understand the ‘why’ behind what they are asking. Opening a cannabis bank account is not as easy as opening a traditional business bank account. With cannabis being federally illegal, banks, and credit unions must adhere to the rules and regulations set forth by our regulators, also tying in the respective state that the cannabis business is operating in.

An initial phone call is often set up for the financial institution to learn more about the cannabis business, its owners, and signers. Knowing when the business will be operational and what their big picture looks like is fundamentally important. Questions could be asked about ownership, location, growth, licenses, and compliance. Some products and services are not fully available to the cannabis industry, because other players have not fully opted in (i.e., merchant processing and debit/credit cards). This makes the financial institution banking cannabis able to create a product suite that they feel comfortable with from a risk and compliance standpoint. Pricing out cannabis bank accounts is also something that differs from the traditional businesses being banked.

Again, not every financial institution will support cannabis, and that is because it is expensive. It is expensive because those that support the industry have had to seek guidance from consultants, their respective regulator, their state, their local cannabis groups and associations and their board of directors. The initial onboarding of a cannabis customer, after pricing is accepted, takes longer as well. Background and credit checks, as well as risk reviews need to be completed at most financial institutions, along with an initial onsite audit visit.

It is widely understood that cannabis businesses must go through an inspection with their operating state before they are licensed, however, financial institutions are still required to make sure they know what they are working with. Most financial institutions work closely with their compliance/BSA teams to develop risk profiles so that if questions are asked of them during an audit, they can answer to the best of their knowledge the transactions that are occurring and then prove that we understand what the cannabis businesses are using their accounts for. Many financial institutions have implemented the use of compliance software that allows their cannabis departments to review transactions, seed-to-sale monitoring, monitor licensing, insurance, onsite visits, and financial changes. METRC and Bio Track are the two main seed-to-sale tracking systems used throughout the United States. Most states have adopted using one or the other and few have implemented their own manual tracking.

The seed-to-sale system your financial institution chooses to work with can integrate with your respective state’s seed-to-sale tracking system for financial institutions to monitor account transactions and seed-to-sale flow. It is common to have your financial institution reach out to you once you have been onboarded to integrate your API key (QR code that houses your cannabis licenses) into their respective compliance software to initialize the tracking component. Directly after this, the designated person at the cannabis business or CPA (to be determined by the cannabis business) will be asked to upload your financials into the compliance software monthly for tracking purposes. These systems correlate with most POS systems as well as QuickBooks for a seamless flow. Financial Institutions are often asked by cannabis businesses if this is something they can do in-house or if they can utilize an outside CPA firm to help. The answer is yes to both. It takes minimal time each month to upload your financials so doing it yourself is certainly feasible, however, there are many CPA firms out there who will do it for you, along with making sure your numbers make sense and your taxes are accounted for. Not to mention, the annual CPA attestation as well.

Financial institutions are not asking you to do this to make your life difficult. It is simply because this is a new industry, one that is federally illegal at that, and verifying information to better understand how the industry works only helps to normalize it. It is also common for your financial institution to ask for invoices to accompany transactions such as wires, ACH, bill pay, checks, cash deposits, etc. We do this because auditors also ask us if we can, in fact, verify we know what this transaction was for and to whom the funds went. It also helps with fraud surveillance. Most financial institutions have experts in fraud or compliance who can help deter this from happening to you and your business.

We have come a long way since inception and have learned a lot over the years. What is important to know is we are all a team. The cannabis business and the financial institution are working together to understand how they both complement each other. Together we are building the cannabis industry, so that one day, when it is stabilized and normalized, we can take that with us for the next big thing. Every industry out there was new at one point and had to go through the same trials and tribulations, and while most of us cannot remember or have never been a part of the ‘build out,’ it did happen at some point. When your financial institution asks you for something related to transactions or business, please understand that it is for the better of the industry.

We can work together to normalize and strengthen this industry. All the steps we are taking are learning opportunities. I believe everyone can say at one point they did not know how to do something, but through training, education, and a road map, we were able to develop a routine so that as we grew at understanding something we had not understood before, it became normal.

Nicole Perry has been with Dart Bank since 2016 as the Office Manager and most recently VP/Senior Treasury Management Officer. She brings with her 20 years of financial services experience. Prior to joining Dart Bank, she worked for various financial institutions holding many different roles, specializing in business banking.

Nicole is an alumna of the Lansing Chamber of Commerce’s Lansing Leadership 2018 class and is part of the Perry School of Banking class of 2020. She received her Bachelor of Arts in Business Management with an emphasis in Human Resources from Davenport University and attended Central Michigan University for her Master of Science degree. In her spare time, Nicole enjoys attending Michigan State University football and basketball games and spending time with her family and friends at the lake.

Video: NCIA Today – Thursday, July 28, 2022

NCIA Director of Communications Bethany Moore checks in with what’s going on across the country with the National Cannabis Industry Association’s membership, board, allies, and staff. This week Bethany is joined by NCIA CEO Aaron Smith and Deputy Director of Government Relations Michelle Rutter Friberg. Join us every other Thursday on Facebook for NCIA Today Live.

Equity Member Spotlights: Where Are They Now?

Where are they now? This month, NCIA’s editorial department continues the monthly Member Spotlight series by following up with three of our Social Equity Scholarship Recipients as part of our Diversity, Equity, and Inclusion Program. Participants are gaining first-hand access to regulators in key markets to get insight on the industry, tips for raising capital, and advice on how to access and utilize data to ensure success in their businesses, along with all the other benefits available to NCIA members.

First off, we have rebranded. We are now Cannvas Events. The name change was part of our evolution and maturation as a startup. As we scaled, more resources became available for things like branding. We brought in Greg Hill of Brand Birth to deploy the science of branding and the end result was a new name, new logo, and new understanding of where we were situated in the regulated cannabis ecosystem. The transformation led to the planning and production of our signature Cannabis Event 2.0 offering, the inaugural Saturnalia Canna Carnival, taking place at the Trinity Health Arena in Muskegon, MI on August 2oth. We are powering a traditional indoor/outdoor carnival – rides and attractions included – with a hassle-free, normalizing consumption solution. If you’re in the Midwest, come join us as we celebrate the first year of an iconic, perennial cannabis festival. Tickets and info at cannvasevents.com and follow us @saturnaliacannacarnival

Would you like to share anything that came out of being in the Spotlight previously?

The Spotlight feature presented tremendous value. The first year of the cannabis startup journey is devoid of financial revenue. Unless you’re needle-in-the-haystack lucky, it’s not even a consideration. The money is flowing in the opposite direction. So, the only available revenue, or currency, are the relationships. If you’re fortunate, these become renewable resources upon which you can draw repeatedly, and managed properly, they have no expiration date. You can bank them like any currency and you have much more influence on their stability, than on fiat currency. For me, that one relationship was with Michael Schwamm, who leads the Duane Morris cannabis practice out of New York. Michael opened doors for me and got me into rooms that I was previously unaware existed. That access has made all of the difference for me, personally, and for Cannvas Events. And had it not been for the Spotlight, I would have never been in position to enjoy that access.

Endo Industries

Since the last spotlight, you’ve joined the DEI Committee and its Regulatory Subcommittee. Anything you’d like to share about that experience thus far?

I’m impressed by the brilliant folks on the committee, and their dedication to making cannabis equitable. It takes time out of our grueling work days to contribute time on these committees but the contribution to making the industry better is crucial during these developmental years of cannabis. Perhaps our current misguided, harmful CA cannabis policies could have been prevented with more early participation from stakeholders who are stewards of the plant. However, there were many factors involved with the way CA policies were created, including special interest money from those who don’t care or want to see the industry fail.

It’s been a painful journey living through the consequences of these challenging policies as a cannabis operator. It takes a long time to change once it’s been passed. However, companies who are willing to work together in these important processes will survive and write a new path to move forward. Most of us can’t wait anymore for things to change so we need everyone’s active participation now, whether it’s writing an email to your constituents or being a part of NCIA!

California cannabis seems to be going through terrible challenges. Is there anything you’d like to share about what you’re seeing, or about some of the solutions our members can support with?

Overburdensome taxes and high barriers to entry for licensing throughout the state are most obvious right now. The lack of diversity and equity, consumer education, state and federal funding for further research and development also play a huge role in CA’s struggles. I’m frustrated that the State doesn’t understand that those who have been dedicated to the industry, collaboration and this plant are the only ones who can truly guide this industry forward.

NCIA members can lend support by truly including legacy, equity, and other diverse teams into your conversations and partnerships, and opening our eyes to value brought to the table by different communities. I would also encourage members to think about ways we can create awareness to our consumers to make better buying decisions. We have left all the medical properties of cannabis while legalizing, and that’s also why the industry is failing. Lastly, we need to keep pushing for more consumption lounges and events!